FOREX: Risk Off Stabilizes USD Index, Yen Outperforms A$ & NZD

The USD BBDXY index sits up from post FOMC lows (1208.32), last near 1210.75, with risk off trends in the equity and crypto space driving outperformance versus higher beta plays. AUD/USD is off 0.60%, with the softer local jobs data for Nov also weighing. JPY and to a lesser extent CHF, have edged up versus the USD, in line with the risk off tones from the cross asset space.

- US equity futures have been weighed by the tech side, with Nasdaq futures down 1.5% at one stage (last -1.15%). Eminis were down 1%, last off -0.80%. Late US Wednesday time Oracle results weighed on the market and spilled over to Nvidia in after hours trading. The market remains sensitive to chip/AI related developments. Crypto is also weaker, down 2.5% for Bitcoin, although dips under 90k have been supported so far.

- AUD/USD is down 0.60%, last near 0.6635, close to session lows. The November labour market data were consistently softer, apart from the stable unemployment rate. However, the data are volatile and more data is needed to determine if there is a slowing. AUD/JPY is down 0.75%, last near 103.35/40, just up from session lows.

- The AUD/NZD cross is around 1.1450, off 0.25%. NZD/USD is back under the 0.5800 pivot.

- USD/JPY got to lows of 150.49, but now sits back at 155.75/80. We couldn't sustain the earlier break under the 20-day EMA.

- EUR/USD got to highs of 1.1707, but now sits back under 1.1690. For GBP.USD it has been a similar backdrop, last near 1.3365, after getting to 1.3392 earlier (fresh highs since mid Oct).

- Later US 6 December jobless claims and delayed September trade & inventories are released. The SNB decision is announced, the Eurogroup meeting takes place and BoE Governor Bailey speaks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Lower As Risk Sentiment Stabilises & Waits For November Reports

Oil prices are slightly lower in Tuesday’s APAC session following moderate gains yesterday as risk sentiment stabilised. WTI is down 0.3% to $59.96/bbl but it has spent much of the session below $60. It made a high of $60.12 before moderating again. Brent is 0.2% lower at $63.95/bbl after reaching $64.06. The USD index is up 0.1%, likely pressuring dollar-denominated crude.

- With the support of a number of Democrats, the bill to provide US government funding until 30 January passed the Senate. The House of Reps will vote on Wednesday EST.

- After Saudi Arabia reduced its price premium for shipments to Asia, Kuwait has set December deliveries to Europe at a $2/bbl discount while the US faces a $2.90/bbl premium.

- Attention remains firmly on the expected record 2026 market surplus with the IEA’s monthly report published on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November. The IEA increased its 2026 surplus forecast in its October monthly report.

- US President Trump said that a US-India trade deal is close which would reduce the average tariff rate. However, Russia’s Interfax reported that India continues to buy Russian crude despite Trump commending them for reducing purchases.

- The US bond market is shut for Veterans Day, which could impact oil trading volumes, but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

AUSSIE BONDS: Grinding Cheaper After Mixed Confidence Data

ACGBs (YM -3.0 & XM -1.0) are modestly weaker.

- Cash ACGBs are 1-3bps cheaper, with a flattening bias, in today’s Asia-Pac session after today’s confidence data.

- The details of the November Westpac consumer confidence survey are mixed, signalling that there could be payback in December. It rose despite lower sentiment amongst mortgage holders as a group and less optimism regarding the labour market outlook.

- NAB business confidence and conditions were little changed in October, with the former down 1 point to +6 and the latter up 1 point to +9.

- The bills strip has bear-steepened, with pricing -2 to -4.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 8% probability, with a cumulative 14bps of easing priced by mid-2026.

- Tomorrow, the local calendar will see Home Loan data alongside RBA's Jones-Fireside Chat.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond tomorrow and A$800mn of the 1.75% 21 November 2032 bond on Friday.

FOREX: Asia-Pac FX: USD Drifts Higher In Asia

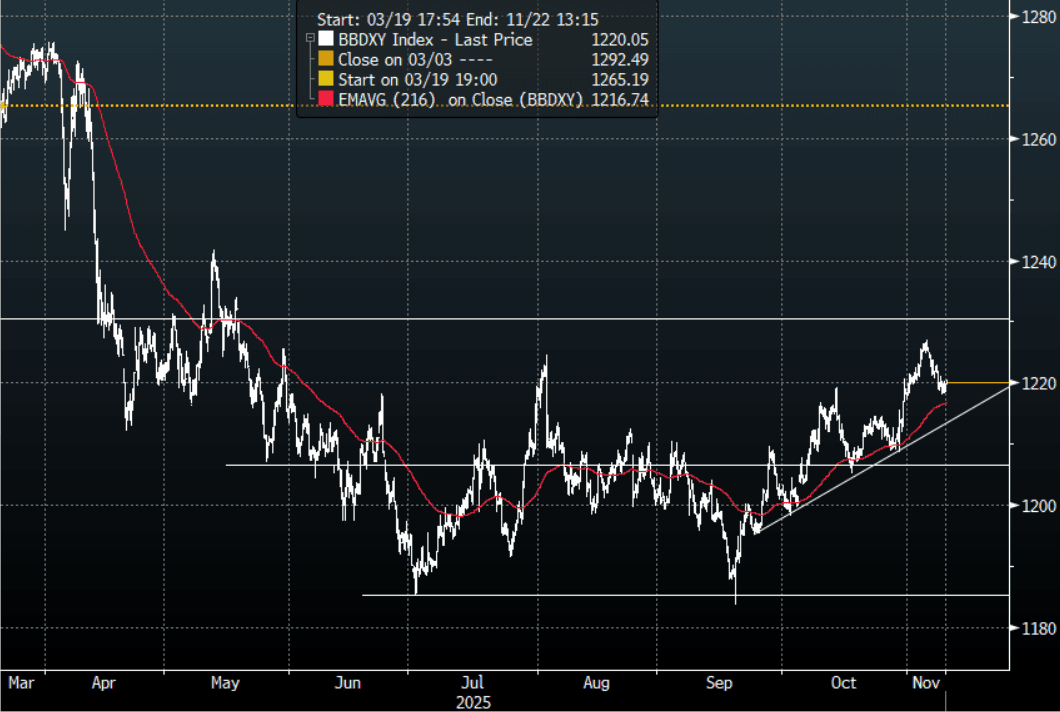

The BBDXY has had a range today of 1218.71 - 1220.57 in the Asia-Pac session; it is currently trading around 1220, +0.10%. The USD has found some support between 1218-1220 and has consolidated here the last couple of sessions. USD/JPY should continue to be well supported but I suspect the USD will be sold against risk currencies like the AUD & NZD and the EUR if this surge in risk sentiment turns into an end of year rally for risk. I am caught undecided on the USD at the moment, I liked the fade into 1230 initially but short term I expect dips back toward 1210-1215 to now be supported first up. We could chop around sideways for a while while the market decides which way to go. Above 1230 and we could start to break higher, below 1205 and the downtrends momentum could be re-engaged.

- EUR/USD - Asian range 1.1547 - 1.1564, Asia is currently trading 1.1555. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This has been the pivot with the larger 1.1400-1.1900 range over the past few months.

- GBP/USD - Asian range 1.3158 - 1.3181, Asia is currently dealing around 1.3170. The pair continues to build on its bounce off the 1.3000 area. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.05%, Gold $4145, BBDXY 1220, Crude Oil $60.01

- Data/Events : EZ ZEW Survey Expectations, Germany ZEW Survey Expectations

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P