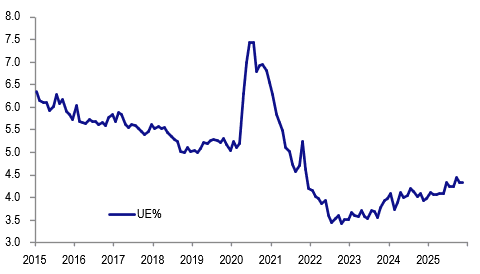

AUSTRALIA DATA: Nov Jobs Market Softer But Volatile, More Data Needed

The November labour market data were consistently softer, apart from the stable unemployment rate. However, the data are volatile and averages need to be considered and they were mixed. The RBA continues to see the jobs market as “a little tight”. Governor Bullock said that the Board is likely to discuss a prolonged pause or hiking in 2026 dependent on the data as inflation and capacity pressures are rising. Given the volatility, this release is likely to be consistent with the Board wanting more information.

- There don’t seem to be special factors although the ABS notes some “operational challenges” for NSW data collection but it made adjustments and “there are no residual data quality concerns”.

- The fall in the labour force exceeded employment at -23k versus -21.4k driving a 0.2pp decline in the participation rate to 66.7%.

- The 3-month average in jobs fell slightly to +10.3k from +14k in October with Q4 growth at 1.4% y/y after Q3’s 1.5%, slightly above the RBA’s November Q4 projection of 1.3%.

- The unemployment rate remained at 4.3% keeping the Q4 average at 4.3%, 0.1pp below the RBA’s Q4 forecast.

Australia unemployment rate %

Source: MNI - Market News/ABS

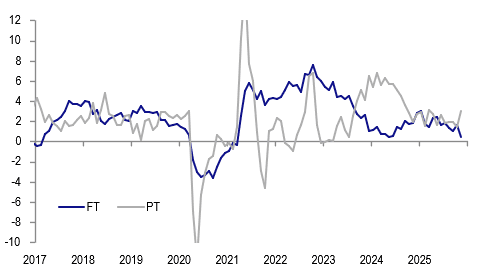

- Full-time (FT) jobs fell 56.5k unwinding October’s +53.6k while part-time (PT) rose 35.2k after -12.5k. The 3-month averages were steady.

- Hours worked were flat in November but 3-month momentum rose driven by both PT and FT. FT fell 0.2% m/m but the 3-month average annual rate was little changed at 1.3% y/y. PT hours were strong rising 0.7% m/m with momentum at 4.8% and growth up to 4.5% y/y from 3.1% driving the average to 3.1% y/y from 2.4% y/y.

- This growth in PT hours and employment may reflect employer caution if they are uncertain about the outlook. More data is needed to confirm this.

- The underemployment and youth unemployment rates also rose showing 0.2pp increases in the 3-month averages from October.

Australia employment y/y%

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

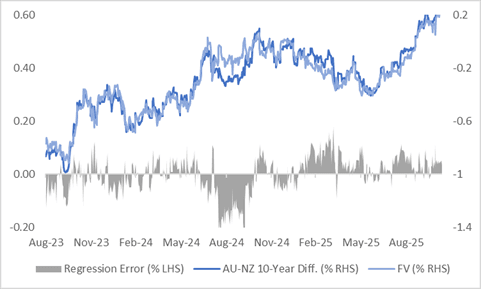

AUSSIE BONDS: AU-NZ 10Y Yield Differential At Highest Since 2020

The AU–NZ 10-year yield differential stands at +30bps, its widest since October 2020.

- The move mirrors a similar widening in the AU–NZ 1-year forward 3-month swap (1Y3M) spread, which is now at its highest level since 2012.

- A simple regression analysis of the AU-NZ 10-year yield differential against the AU-NZ 1Y3M spread over the past two years shows that the 10-year differential is around 3bps above fair value based on the regression model.

- The 1Y3M differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-NZ: 10-Year Yield Differential Vs. FV

Source: Bloomberg Finance LP / MNI

CNH: USD/CNY Fix Edges Up, Fixing Error Steady, CNH/JPY Probing Higher

The USD/CNY fix printed at 7.0866, versus a BBG market consensus of 7.1197. The fixing is a touch above yesterday's outcome, while the fixing error is little changed at -331pips. USD/CNH is a little higher post the fixing, but at 7.1250 remains within recent ranges. Broader USD sentiment is mostly positive so far today, with USD/JPY probing recent highs near 154.50. The CNH/JPY cross is above 21.67, with upside focus to be on recent highs around 21.70.

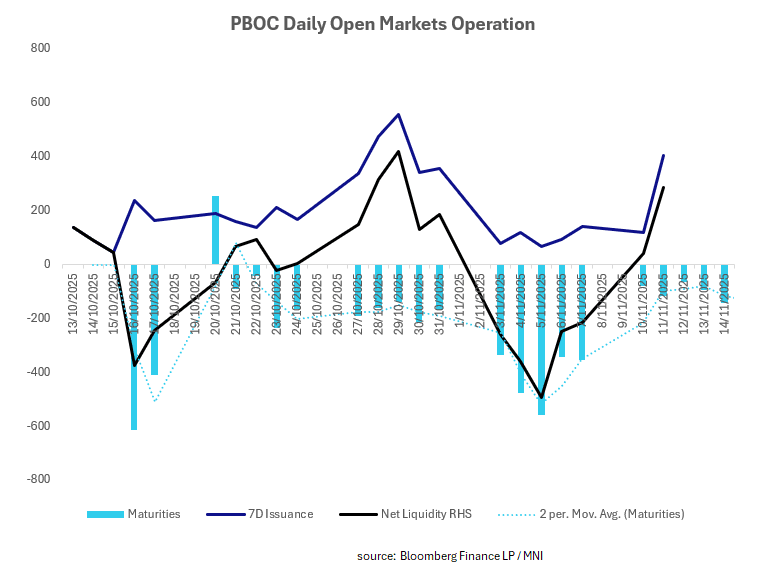

CHINA: Central Bank Injects CNY286.3bn via OMO

Money market rates still remain elevated as the PBOC has another day of significant liquidity injection. The overnight money market rate spiked this morning to its highest level since July.

- The PBOC issued CNY403.8n of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY117.5bn.

- Net liquidity injects CNY286.3bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.43%, from prior close of 1.49%.

- The China overnight interbank repo rate is at 1.53%, from the prior close of 1.45%.

- The China 7-day interbank repo rate is at 1.54%, from the prior close of 1.50%.