ASIA STOCKS: Oracle Warning Shakes Tech Heavy Bourses

A warning from U.S. cloud computing giant Oracle about lower-than-expected profit and revenue outlooks (due to higher infrastructure spending) has seen profit taking in the tech sector today with falls in AI-related stocks and major tech firms like Japan's Softbank (down -7%), Korea's SK Hynix (down -2.9%) and Taiwan's TSMC (down -2%). The warning overshadowed the U.S. Federal Reserve's decision to cut interest rates by 25 basis points to a target range of 3.75%–4.00% in what was generally considered a dovish tone emanating from the FED.

- After a moderately positive start to the week, the NIKKEI is down heavily today with fall of -0.85% and taking the index negative for the week. The NIKKEI now sits over 4% below the October high of 52,411.

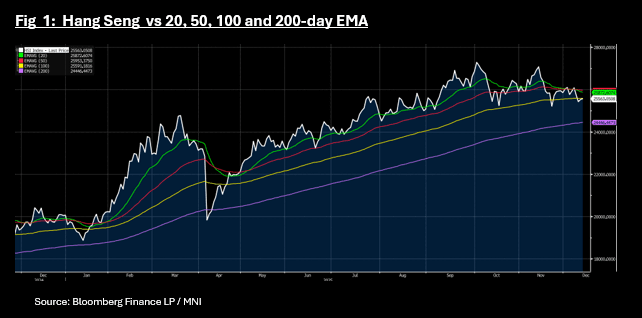

- China's onshore bourses are all down with the Hang Seng marginally positive. With onshore bourses all down -0.20% to -0.50% it took the HSI to lead with gains of +0.10% to reach 25,569 as it nears upside resistance via the 100-day EMA of 25,591

- Tech heavy bourses like the KOSPI and the TAIEX both fell with Taiwan down -1.1%, whilst the KOSPI was down a mere -0.12%

- India's NIFTY 50 has fallen the first four trading days of the week for its worst start to a week since September and is down -0.25% today.

- SE Asia bourses again a mixed with the FTSE Malay KLCI up +0.33% whilst the Jakarta Composite is down -0.25% and the SE Thai -1.1%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Release Of US Delayed Data Could Drive Fed Easing, Political Risks Persist

Gold prices have not only held onto Monday’s 2.9% gain but have risen further despite a stronger US dollar (BBDXY +0.1%) as risk appetite has been more stable. Bullion is up 0.7% to $4144.5/oz after a high of $4149.0, approaching resistance at $4161.4, 22 October high. It has found significant support from progress to end the US government shutdown, which will allow data to be released again. Clarity on the economy and the outlook is key to the 10 December Fed decision.

- With the support of a number of Democrats, the bill to provide government funding until 30 January passed the Senate. The House of Reps will vote on Wednesday EST and if it passes it will go to President Trump to be signed. He has voiced his support. It could then take a few days for operations to resume.

- With funding only assured to the end of January, another impasse next year is clearly possible. A vote by December on extending healthcare benefits was promised to Democrats, which could again be a hurdle to further financing.

- Silver is up 0.9% to $50.97 after reaching $51.142, breaching initial resistance at $51.071, a Fibonacci retracement point.

- Equities are mixed with the KOSPI up 1.0%, Hang Seng down 0.2% but S&P e-mini flat. Oil prices are lower with WTI -0.2% to $59.99/bbl. Copper is down 0.4%.

- The US bond market is shut for Veterans Day but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

BONDS: Subdued Session With Market Little Changed

NZGBs closed little changed, with benchmark yields flat to 1bp cheaper.

- The RBNZ’s Q4 survey of expectations posted unchanged inflation expectations. The central bank is likely to be relieved that not only are they within its 1-3% target band but they didn’t increase in the latest reading following the rise in Q3 CPI to 3.0% y/y from 2.7%, although the RBNZ’s measure of core held steady at 2.7%.

- The RBNZ has maintained for some time that the Q3 increase would be temporary and its August projections showed inflation moderating from Q4 and approaching the band midpoint in 2026 given the degree of spare capacity in the economy.

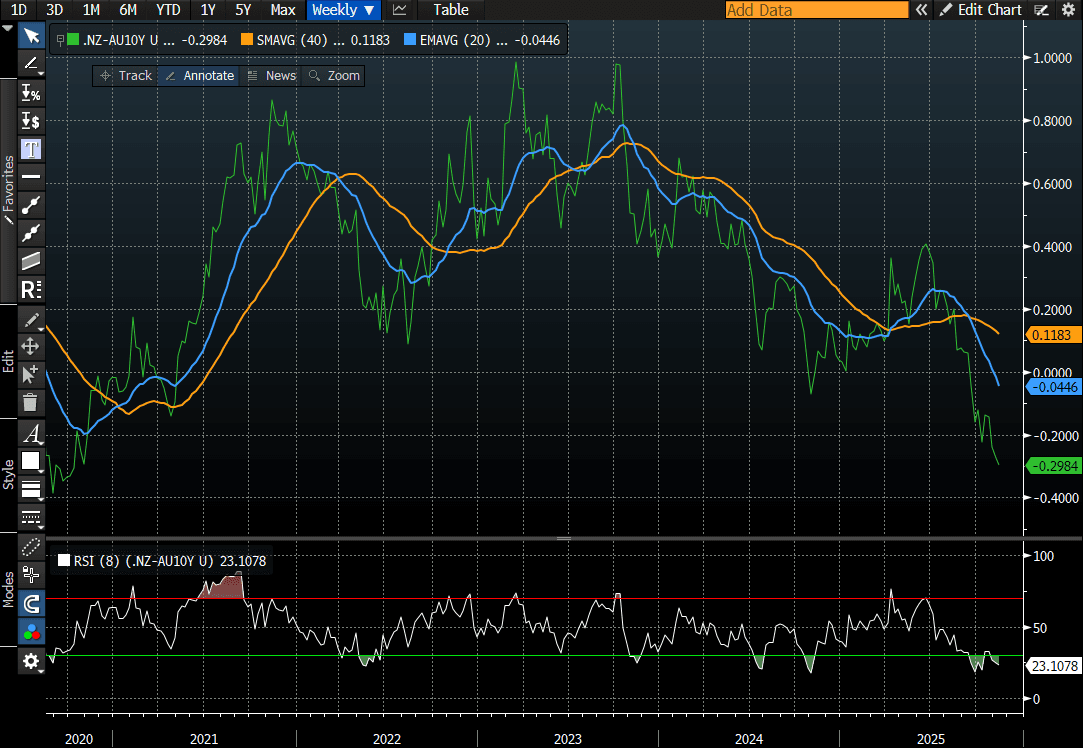

- NZ-AU 10-year differential is unchanged at -30bps, its lowest since 2020. (see chart)

- Swap rates closed are unchanged.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

Tomorrow, the local calendar will be empty ahead of Card Spending data on Thursday.

Bloomberg Finance LP

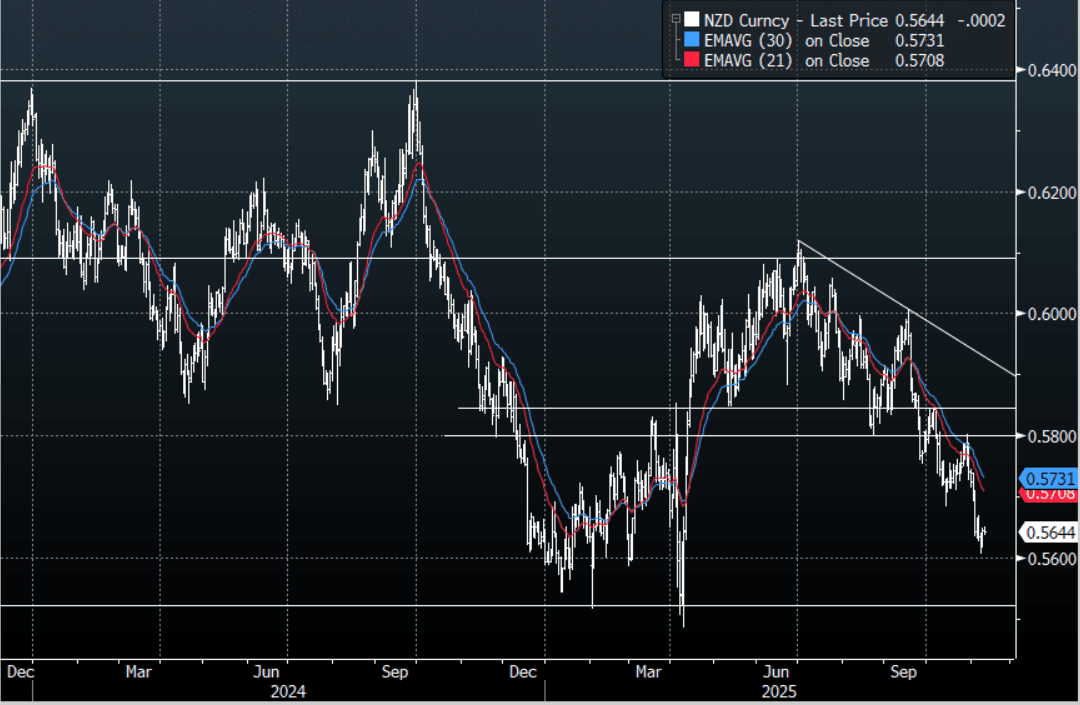

NZD: Asia-Pac: NZD/USD Consolidates Around 0.5650

The NZD/USD had a range today of 0.5636 - 0.5651 in the Asia-Pac session, going into the London open trading around 0.5645, -0.05%. The NZD continues to trade heavy but I continue to be a little wary of positioning in the NZD though as the market is small and traders tend to very quickly become all positioned the same way. The NZD does stand out as a vehicle to express a short in but should this bout of improved risk sentiment grow it will be tough for the NZD to ignore it and it could play catch up to the move at some point, if you feel this bounce in risk will fail and move back lower then the NZD remains a great way to express that. I still suspect any decent bounce will again attract sellers though. The first sell area on a pullback would be around 0.5750 and then the more pivotal 0.5850 area.

- The AU-NZ 10-year yield differential stands at +30bps, its widest since October 2020.

- MNI AU - Inflation Expectations Stable, RBNZ On Track For November Cut. The RBNZ’s Q4 survey of expectations posted unchanged inflation expectations. The central bank is likely to be relieved that not only are they within its 1-3% target band but they didn’t increase in the latest reading following the rise in Q3 CPI to 3.0% y/y from 2.7%, although the RBNZ’s measure of core held steady at 2.7%. The RBNZ has maintained for some time that the Q3 increase would be temporary and its August projections showed inflation moderating from Q4 and approaching the band midpoint in 2026 given the degree of spare capacity in the economy.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5380(NZD460m Nov 13), 0.5600(NZD538m Nov12), 0.5800(NZD461m Nov 12) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P