LNG: US Gas Prices Stabilise As Large Inventory Drawdown Forecast

Natural gas is down this week but US prices stabilised on Wednesday driven by an expected large inventory drawdown while Europe fell because of expectations that recent mild weather will continue into the new year.

- US Henry Hub rose 1.1% to $4.625 but is still down 12.6% this week due to forecasts for higher temperatures going into the latter half of December. The benchmark reached $4.696 off the intraday low of $4.455.

- EIA data for gas inventories for last week are released today and expected to fall 167 bcf compared to the 5-year average to 5 December of -89 bcf, according to Bloomberg. At the end of November they were still 5.1% above average.

- European gas fell 2.4% to EUR 26.820 after rising 1.9% on Tuesday and is down almost 7% in December. Prices trended lower through yesterday to EUR 26.535 before recovering slightly.

- Storage levels continued to trend down falling 0.2pp to 71.6% on Tuesday as low prices are impacting LNG imports. Pipeline flows from Norway were impacted by unplanned maintenance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

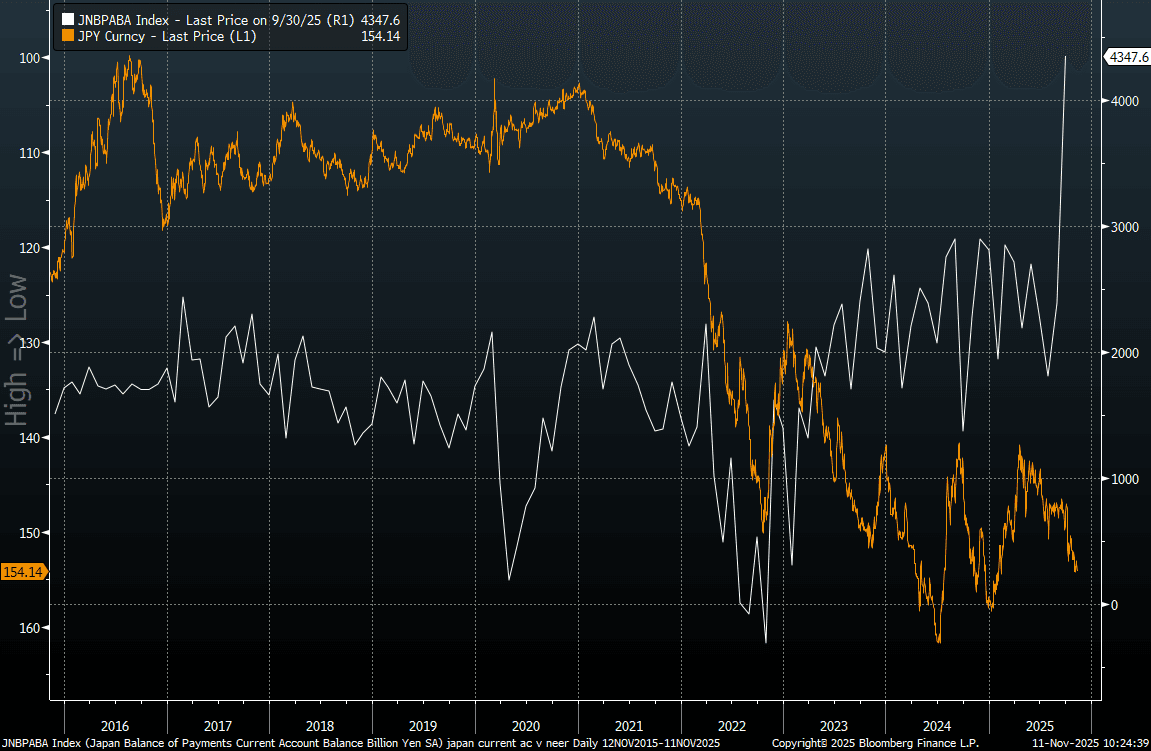

JAPAN DATA: Current A/C Surplus Surges On Income Inflows, But May Not Aid Yen

Japan Sep trade and current account balance data were stronger than forecast, particularly on the current account side. In unadjusted terms we printed ¥4483.3bn, versus ¥2456.6bn projected and ¥3701.4bn prior. In seasonally adjust terms we were at ¥4347.6bn for the current account, close to double the consensus projection and prior outcome. This is the best outcome for at least a few decades. This isn't necessarily a yen positive though, at least based off recent correlations. Current account shifts haven't coincided with yen shifts in recent years.

- The trade balance on a BoP basis aided the current account improvement. We were up to a surplus of ¥236bn, versus a projected deficit of -¥100.1bn. The trade balance remains within recent ranges. The Citi terms of trade proxy for Japan is pointing to positive trade balance outcomes continuing in the near term.

- The bigger driver for the current account improvement though was the surge in the primary income balance, ¥4728.1bn, versus ¥2968.4bn in Aug. These outcomes are usually fairly steady, but point to a pick in net income earned from Japan's offshore investments.

- The chart below plots USD/JPY, which is inverted on the chart (the orange line) against the current account position (the white line). It shows the lack of relationship between the two series, with much of the surplus in Japan potentially re-exported offshore via capital outflows.

- This may benefit the yen at some point, particularly if we see the US authorities (especially Tsy Secretary Bessent) making noises about yen being undervalued relative to Japan's external balances.

- However, this is likely to play out over the medium term rather than in the near term. Short term dynamics around the BoJ/Fed outlooks, which will drive US-JP yield differentials, along with broader risk trends, are likely to remain more important USD/JPY drivers.

Fig 1: Japan Current Account & USD/JPY (Inverted) Trends

Source: Bloomberg Finance L.P./MNI

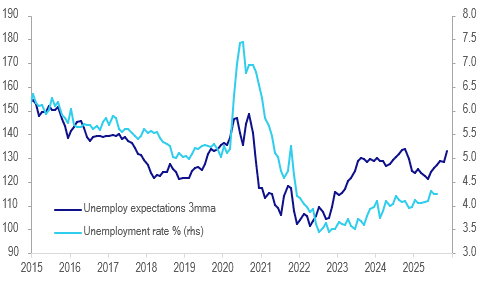

AUSTRALIA DATA: Westpac Consumer Details Mixed, Spending Rise Not A Given

The details of the November Westpac consumer confidence survey are mixed signalling that there could be payback in December. It rose despite lower sentiment amongst mortgage holders as a group and less optimism regarding the labour market outlook but stronger domestic growth and less risk from US tariffs seemed to have driven the rebound into net optimism territory.

- Westpac asked about Christmas spending intentions and 15% said they would spend more than last year up from 11.6% in November 2024 with around 35% planning to spend less, similar to 2024. Westpac describes the responses as “less restrained” than 2024. It shows that the jump in confidence translating into strong spending is not assured.

- Family finances improved with expectations for a year ahead +12.3% to 109.1, significantly stronger than compared to a year ago, which Westpac believes was helped by the RBA not discussing a hike on 4 November despite the surprisingly high Q3 CPI. But 76% of respondents after the RBA decision to keep rates on hold expect rates to be on hold or higher in a year up from 60% in October.

- The economic outlook for the next year and 5 years rose 16.6% and 15.3% respectively and are above their historical averages. But unemployment expectations jumped 9.3% to 139.5 driven by 18-24 year olds and the unemployed. The RBA sees the youth unemployment rate as a lead indicator of the labour market (October prints 13 November).

- The “time to buy a major item” rose 14.9% m/m to 111.6, highest in four years.

Australia Westpac unemployment expectations

Source: MNI - Market News/LSEG/ABS

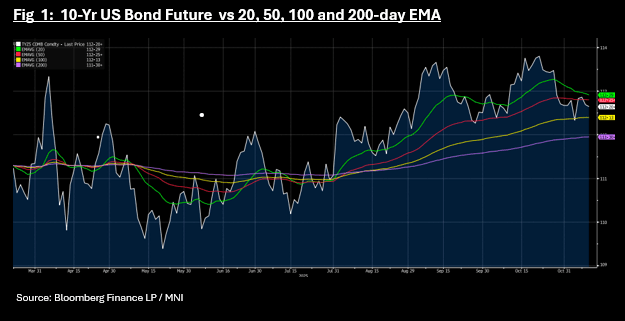

US TSYS: TYZ5 Caught Between Two Key Tech Levels; Waiting for a Catalyst

Following the weak lead in overnight, US treasury futures are hardly moving in this morning's trade with the 10-Yr future down -01+. At 112-20+ TYZ5 remains at the mid-point between the 50-day and 100-day EMA, looking for the next catalyst. With data releases delayed, the focus remains on the news flow on talks to end the US shutdown.

Cash is barely changed from the weak lead in, with yields relatively unchanged to 0.5bps lower from where the US closed.

- The US 2-Yr is at 3.59%

- The US 5-Yr is at 3.715%

- The US 10-Yr is at 4.118%

- The US 30-Yr is at 4.706%

Equity markets across the region are strong with the KOSPI and Hang Seng leading the rally.

The next focus for bond markets will be the US$42bn 10-Yr auction on the 13th, followed by the US$25bn 30-Yr auction on the 14th.