JGBS: Yields Lower As Risk-Off Grips Markets, 20Y Auction Sees Strong Demand

JGB futures are stronger but off session highs, +25 compared to settlement levels, as risk-off sentiment grips markets.

- US equity futures have been weighed by the tech side, with Nasdaq futures down 1.5% at one stage (last -1.15%). Late US Wednesday time Oracle results weighed on the market and spilled over to Nvidia in after-hours trading.

- A Reuters poll shows that 90% of economists expect the BOJ to raise its key interest rate to 0.75% in December, with 69% forecasting it will reach at least 1.0% by September 2026, 77% disapprove of the government financing its supplementary budget largely with new debt, and next year’s labour talks are expected to yield a 5.0% pay increase, slightly below this year’s 5.25%.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session.

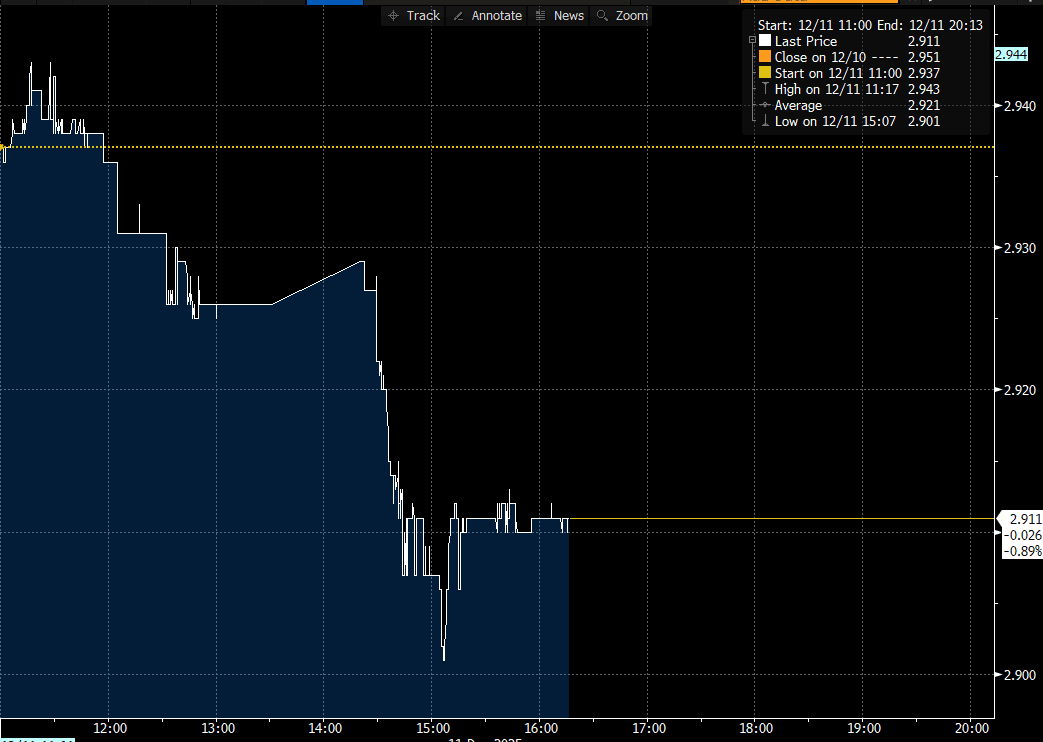

- Cash JGBs are 1-4bps richer across benchmarks, with the 20-year leading after today’s supply (see chart).

- The 20-year JGB auction drew its strongest demand since 2020. The low-price outperformed dealer forecasts, which were set at 97.10 according to a Bloomberg poll. Moreover, the cover ratio increased to 4.0958x from 3.2825x in the previous outing.

- Swap rates are ~1bp lower.

- Tomorrow, the local calendar will see October IP and Capu data.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: China Skips Party, as Regional Bourses Strong on Tech/Shutdown End

The NIKKEI was buoyed by improving global sentiment as Sony Group has delivered decent quarterly earnings, with a share buyback as well. The KOSPI's relentless rally continues as key tech stocks rise between 4-6% on the potential for an end to the US shutdown. In Taiwan, TSMC reported with sales up over 16% in October, in line with forecasts, but the slowest month in six months. Markets are looking ahead to Nvidia's earnings outlook next week and with Asia's key tech stocks correlations growing with Nvidia, it is likely to drive sentiment into next week.

- The NIKKEI's gains were modest, a mere +0.24% and over 2.6% below last week's record high.

- The KOSPI is up +0.86% today and almost 14% over the last month. The sell off last week sees the KOSPI no longer overbought on the relative strength index, providing potential upside should Nvidia's results be in line or better than expected.

- China's bourses have missed the rally today with all major bourses down. All major bourses remain above all moving averages, with upward sloping trend lines suggesting that the positive trend remains in place. Despite this the Hang Seng is down -0.20%, the CSI 300 -0.67%, Shanghai down -0.38% and Shenzhen down -0.32%.

- South East Asia's major bourses are mixed with SE Thai and Jakarta Comp down, whilst the FTSE Malay KLCI is up +0.58% and the FTSE Straits Times in Singapore +1.1%. For the KLCI, it is the best start to a trading week since the end of September.

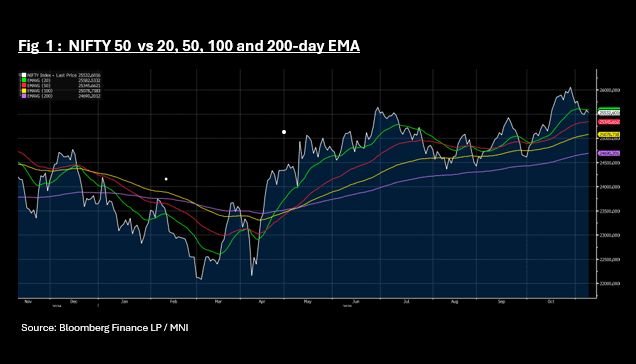

- Whilst India's NIFTY 50's finished higher yesterday, it finished on a weakening trend; giving back earlier gains. That sentiment flowed over into today with falls of -0.21% to 25,535 as the index fails to break above the 20-day EMA of 25,582.

OIL: Crude Lower As Risk Sentiment Stabilises & Waits For November Reports

Oil prices are slightly lower in Tuesday’s APAC session following moderate gains yesterday as risk sentiment stabilised. WTI is down 0.3% to $59.96/bbl but it has spent much of the session below $60. It made a high of $60.12 before moderating again. Brent is 0.2% lower at $63.95/bbl after reaching $64.06. The USD index is up 0.1%, likely pressuring dollar-denominated crude.

- With the support of a number of Democrats, the bill to provide US government funding until 30 January passed the Senate. The House of Reps will vote on Wednesday EST.

- After Saudi Arabia reduced its price premium for shipments to Asia, Kuwait has set December deliveries to Europe at a $2/bbl discount while the US faces a $2.90/bbl premium.

- Attention remains firmly on the expected record 2026 market surplus with the IEA’s monthly report published on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November. The IEA increased its 2026 surplus forecast in its October monthly report.

- US President Trump said that a US-India trade deal is close which would reduce the average tariff rate. However, Russia’s Interfax reported that India continues to buy Russian crude despite Trump commending them for reducing purchases.

- The US bond market is shut for Veterans Day, which could impact oil trading volumes, but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

AUSSIE BONDS: Grinding Cheaper After Mixed Confidence Data

ACGBs (YM -3.0 & XM -1.0) are modestly weaker.

- Cash ACGBs are 1-3bps cheaper, with a flattening bias, in today’s Asia-Pac session after today’s confidence data.

- The details of the November Westpac consumer confidence survey are mixed, signalling that there could be payback in December. It rose despite lower sentiment amongst mortgage holders as a group and less optimism regarding the labour market outlook.

- NAB business confidence and conditions were little changed in October, with the former down 1 point to +6 and the latter up 1 point to +9.

- The bills strip has bear-steepened, with pricing -2 to -4.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 8% probability, with a cumulative 14bps of easing priced by mid-2026.

- Tomorrow, the local calendar will see Home Loan data alongside RBA's Jones-Fireside Chat.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond tomorrow and A$800mn of the 1.75% 21 November 2032 bond on Friday.