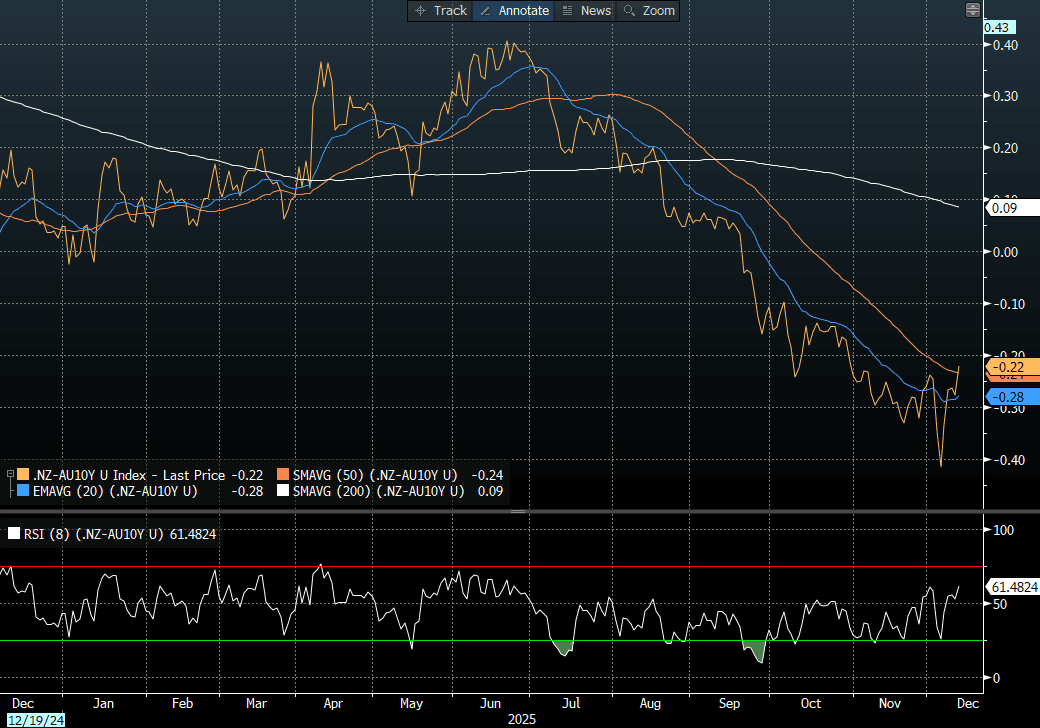

BONDS: NZGBS: Bull-Flattener But NZ-AU 10Y Diff Sharply Higher

NZGBs closed showing a bull-flattener, with benchmark yields 2-5bps lower. Nevertheless, yields remain 27-48bps higher than pre-RBNZ levels on 26 November.

- Today’s weekly supply shows solid to great demand, with cover ratios ranging from 3.33x (Apr-33) to 5.09x (May-30).

- On a relative basis, however, NZGBs underperformed their $-bloc counterparts, with the NZ-US 10-year yield differential 1bp higher, while the NZ-AU differential rose by 6bps. As the chart shows, the NZ-AU spread has rebounded sharply from its lowest level since 2020.

- A simple regression analysis of the NZ-AU 10-year yield differential against the NZ-AU 1Y3M spread over the past two years shows that the 10-year differential is around 6bps below fair value based on the regression model.

- Swap rates closed 4-5bps lower.

- RBNZ-dated OIS pricing closed little changed across meetings. 1bp of tightening is priced for February, while November 2026 assigns 61bps.

- Tomorrow, the local calendar will see BusinessNZ Manufacturing PMI.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

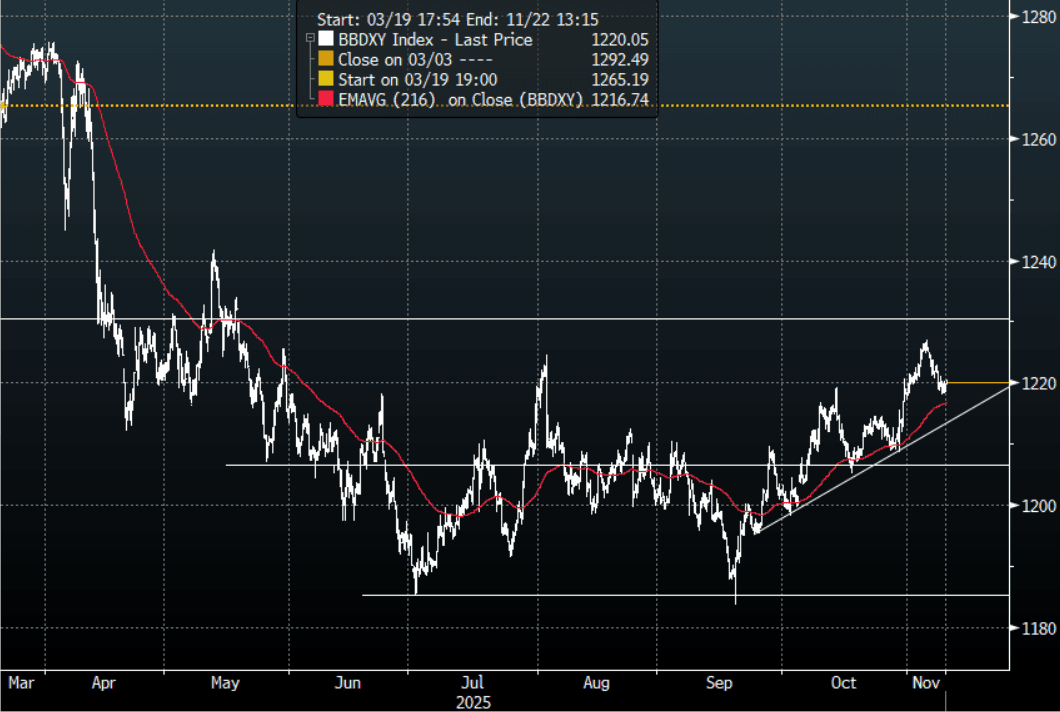

FOREX: Asia-Pac FX: USD Drifts Higher In Asia

The BBDXY has had a range today of 1218.71 - 1220.57 in the Asia-Pac session; it is currently trading around 1220, +0.10%. The USD has found some support between 1218-1220 and has consolidated here the last couple of sessions. USD/JPY should continue to be well supported but I suspect the USD will be sold against risk currencies like the AUD & NZD and the EUR if this surge in risk sentiment turns into an end of year rally for risk. I am caught undecided on the USD at the moment, I liked the fade into 1230 initially but short term I expect dips back toward 1210-1215 to now be supported first up. We could chop around sideways for a while while the market decides which way to go. Above 1230 and we could start to break higher, below 1205 and the downtrends momentum could be re-engaged.

- EUR/USD - Asian range 1.1547 - 1.1564, Asia is currently trading 1.1555. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This has been the pivot with the larger 1.1400-1.1900 range over the past few months.

- GBP/USD - Asian range 1.3158 - 1.3181, Asia is currently dealing around 1.3170. The pair continues to build on its bounce off the 1.3000 area. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.05%, Gold $4145, BBDXY 1220, Crude Oil $60.01

- Data/Events : EZ ZEW Survey Expectations, Germany ZEW Survey Expectations

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Release Of US Delayed Data Could Drive Fed Easing, Political Risks Persist

Gold prices have not only held onto Monday’s 2.9% gain but have risen further despite a stronger US dollar (BBDXY +0.1%) as risk appetite has been more stable. Bullion is up 0.7% to $4144.5/oz after a high of $4149.0, approaching resistance at $4161.4, 22 October high. It has found significant support from progress to end the US government shutdown, which will allow data to be released again. Clarity on the economy and the outlook is key to the 10 December Fed decision.

- With the support of a number of Democrats, the bill to provide government funding until 30 January passed the Senate. The House of Reps will vote on Wednesday EST and if it passes it will go to President Trump to be signed. He has voiced his support. It could then take a few days for operations to resume.

- With funding only assured to the end of January, another impasse next year is clearly possible. A vote by December on extending healthcare benefits was promised to Democrats, which could again be a hurdle to further financing.

- Silver is up 0.9% to $50.97 after reaching $51.142, breaching initial resistance at $51.071, a Fibonacci retracement point.

- Equities are mixed with the KOSPI up 1.0%, Hang Seng down 0.2% but S&P e-mini flat. Oil prices are lower with WTI -0.2% to $59.99/bbl. Copper is down 0.4%.

- The US bond market is shut for Veterans Day but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

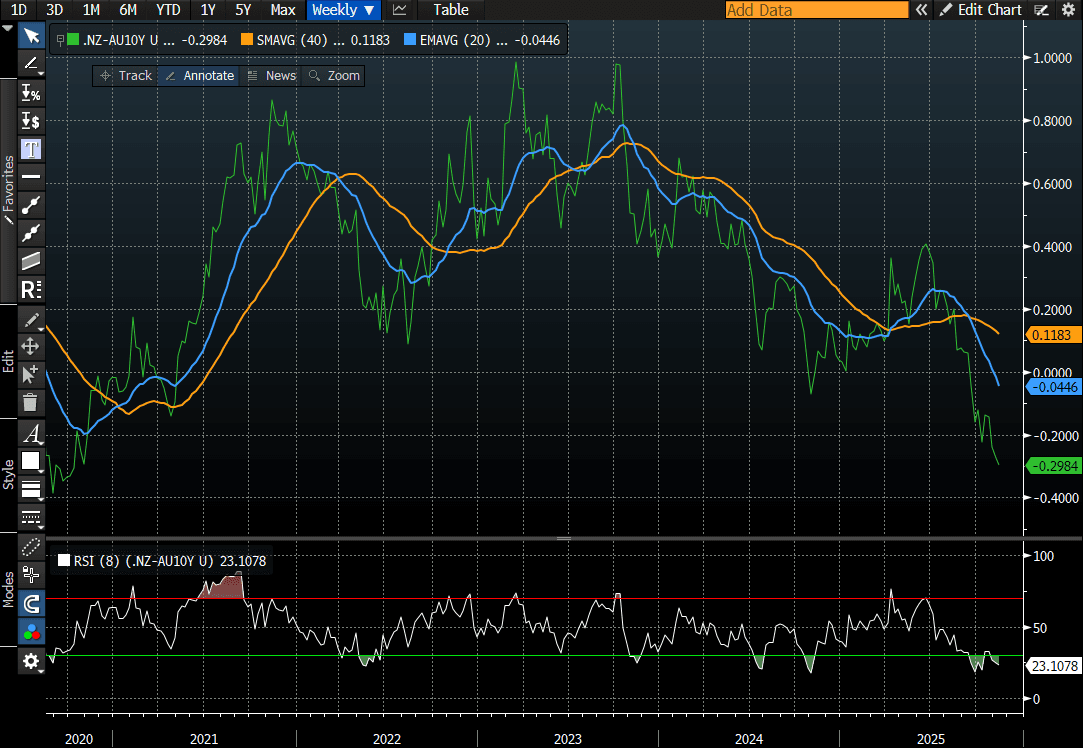

BONDS: Subdued Session With Market Little Changed

NZGBs closed little changed, with benchmark yields flat to 1bp cheaper.

- The RBNZ’s Q4 survey of expectations posted unchanged inflation expectations. The central bank is likely to be relieved that not only are they within its 1-3% target band but they didn’t increase in the latest reading following the rise in Q3 CPI to 3.0% y/y from 2.7%, although the RBNZ’s measure of core held steady at 2.7%.

- The RBNZ has maintained for some time that the Q3 increase would be temporary and its August projections showed inflation moderating from Q4 and approaching the band midpoint in 2026 given the degree of spare capacity in the economy.

- NZ-AU 10-year differential is unchanged at -30bps, its lowest since 2020. (see chart)

- Swap rates closed are unchanged.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

Tomorrow, the local calendar will be empty ahead of Card Spending data on Thursday.

Bloomberg Finance LP