MNI EUROPEAN MARKETS ANALYSIS: Equities Worried by Bonds

- Bond markets sell off gave major Asian equity bourses a scare today.

- At China's military parade, President Xi vows to defy intimidation.

- Japan's PM is under pressure as the top power broker resigns and other LDP members to follow suit.

- Australia's growth topped forecasts boosting chances of rates on hold at the next RBA.

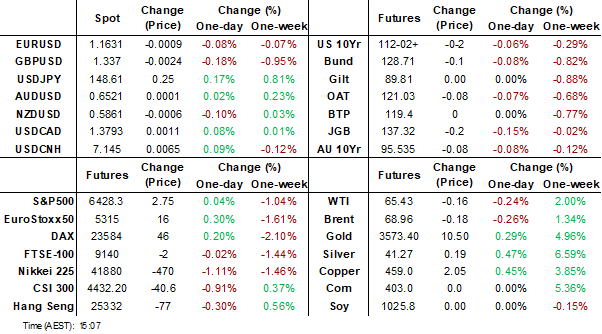

MARKETS

The TYZ5 range has been 112-03 to 112-08+ during the Asia-Pacific session. It last changed hands at 112-04, down 0-00+ from the previous close.

- The US 2-year yield has edged higher trading around 3.65%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.281%, up 0.02 from its close.

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. The price action in the long-end looks pretty dire, the 4.35/4.40% area needs to hold for the longs to remain in control.

- Bessent to Start Fed Chair Interviews on Friday -- WSJ. "There are 11 contenders for the job, according to Bessent and his advisers. Among them are Fed governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett and former Fed governor Kevin Warsh. Following the interviews, Bessent plans to recommend a final list of candidates to President Trump.”

- Bob Elliott on X: “If you shift to easing when inflation is nearly 4% and rising, there are consequences(the UK). JP & the FOMC should take note.”

- Robin Brook on X: “The 30-year yield is rising everywhere, even though the world's central banks are in an easing cycle. That's the best indication that rising long yields are due to a global debt glut, the answer to which is to get lax fiscal policy under control. Not lean on your central bank...”

- Data/Events: MBA Mortgage Applications, Wards total Vehicle Sales, JOLTS, Factory Orders, Durable Goods Orders, Fed Beige Book

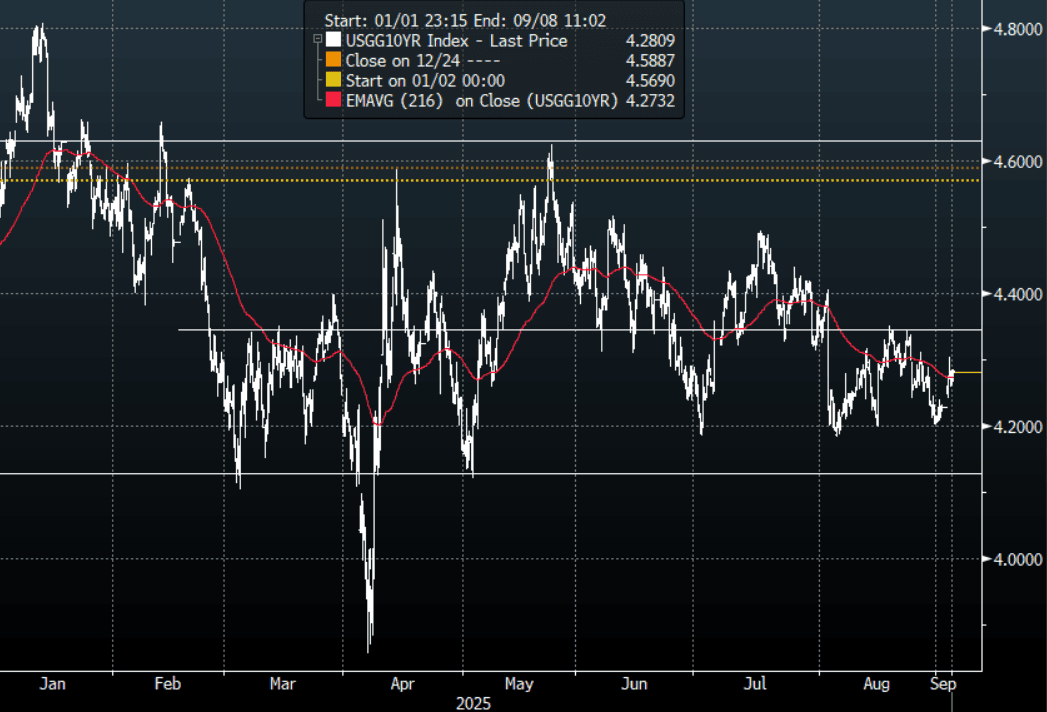

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

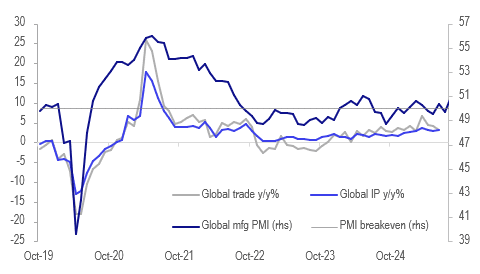

GLOBAL MACRO: Indicators Suggest Global IP Growth Continued In Q3

The August JP Morgan global manufacturing PMI printed at 50.9 up from 49.7 signalling growth in activity in the sector again and at its fastest since May 2024. The pickup was driven particularly by higher output but also domestic orders and a return to hiring but confidence remained below average. The PMI, LME metal prices and the Baltic Freight Index (BFI) are all consistent with global IP and trade growth remaining at current rates or possibly improving.

Global growth

Source: MNI - Market News/LSEG/Bloomberg Finance L.P.

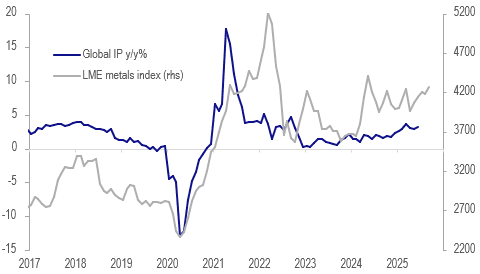

- CPB global IP growth rose 0.4% m/m in June driving a 0.4pp improvement in annual growth to 3.2% y/y, the strongest since March which was boosted by the frontloading of deliveries to the US ahead of tariff deadlines. June global trade rose 3% y/y down from 4.1% y/y.

Global IP y/y% vs LME metals

- August output in the JP Morgan PMI rose to 51.7 from 49.7 helped by orders up 1.1 points to 50.9. All sectors saw growth. However the increase was driven by domestic demand and export orders continued to contract but at a slower rate but tariff worries remained a problem, according to JP Morgan.

- The increase in demand likely drove an improvement in employment with it marginally returning to growth territory at 50.2.

- The resumption of output growth in manufacturing was also across most countries with only 5 continuing to see contraction. India, Thailand, Spain and the US saw strong growth.

- Cost inflation rose to its highest rate since February driving a marginal pickup in selling price inflation with the US reporting the fastest rate.

JGBS: Back End Yields Higher, But Away From Best Levels, 30yr Auction Tomorrow

JGB futures have maintained a negative bias, with the Sep future last near 137.34, -.18 versus settlement levels. We haven't tested sub 137.20 so far (session lows rest at 137.23). Broader trends have been skewed towards weaker futures with US 10yr futures back to flat after initially opening firmer. Aussie bond futures are down sharply, aided by a better Q2 GDP outcome.

- The initial impetus in the cash JGB space was for steeper curves, led by the 20-40yr tenors. We sit away from session extremes though. The 10yr outright yield was last near 1.63%, little changed for the session.

- The 30yr was close to 3.26%, earlier highs were around 3.29%. The 2/30s JGB curve was last around +240bps (sessions highs were at +242bps). The 40yr was last up 3bps, near 3.50%, the 20yr around 2.67%, up 3bps.

- BOJ Governor Ueda met with PMI Ishiba to discuss the economy/markets. Ueda reiterated they will raise rates if the economy, prices move in line with forecasts.

- Domestic politics will remain in focus as well: "JAPAN LDP'S ASO SET TO CALL FOR EARLY PARTY ELECTION: MAINICHI" - BBG.

- The strong focus for tomorrow will be on the 30yr debt auction.

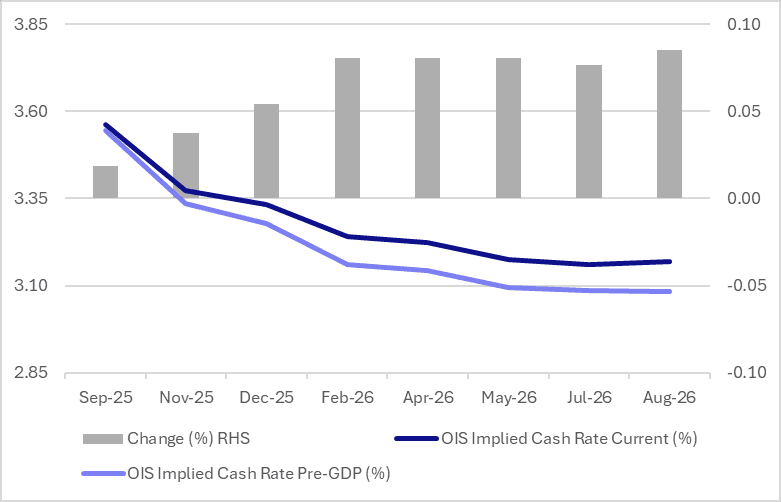

AUSSIE BONDS: Yields Surge, Led By Front End, Q2 GDP Beats, RBA Gov Speaks Later

ACGB yields are higher across the benchmarks. The move started with the back end when onshore markets opened, which was consistent with global developments. However, as the session progressed, front end yields have outperformed, aided by the Q2 GDP beat. A better China services PMI read has also likely aided these moves.

- The 2 and 3yr bond yields are both up around 9bps. This puts the 3yr benchmark close to 3.54%, which is close to mid July highs. Beyond this region note that mid May highs were around 3.69%.

- The 10yr yield is up 7bps to 4.425%, which is also tracking towards mid July highs. The ACGBS 3/10s curve is slightly flatter at +89bps though, bucking the generally steeper trends seen globally.

- Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook.

- RBA dated OIS contracts have shunted higher, led by 2026 dates. We are 2-9 bps firmer versus pre GDP levels, see the chart below. A Sep cut has little chance priced in while a Nov cut is around 75% priced in.

- For futures we have sunk to fresh lows, 3yr (YM) to 96.44, off 9.5bps, while 10yr futures (XM) are down 7.5bps to 95.54.

- Coming up in a few hours at 6pm AEST we have RBA Governor Bullock speaking.

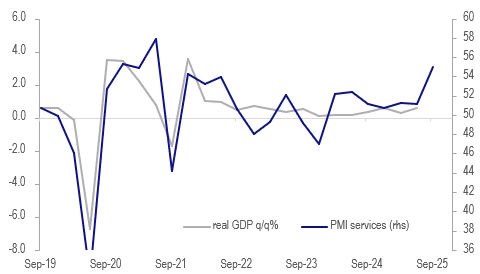

AUSTRALIA DATA: Q2 Boosted By Special Factors, H1 Averaged 0.4% q/q

Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook.

- The S&P Global PMI improvement over Q3 suggests growth may have improved further at the start of H2. The August composite rose to its highest since February 2022.

Australia GDP q/q% vs S&P Global PMI services

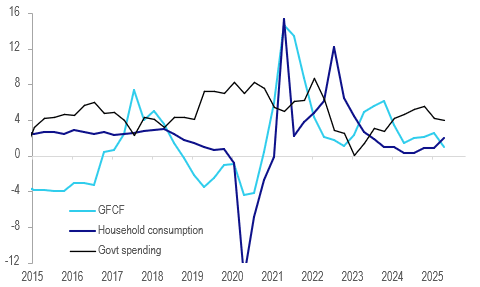

- Household consumption contributed 0.45pp to GDP as it rose 0.9% q/q to be up 2% y/y, the highest in 2 years, which was supported by a 1pp fall in the savings rate to 4.2%. Nominal disposable income rose 0.6% q/q.

- The ABS notes that the close proximity of Anzac Day to Easter boosted holiday-related spending. Also end of financial year discounting encouraged discretionary spending which rose 1.4% q/q.

- Government spending contributed 0.2pp to growth as it increased 1.0% q/q to be up 4% y/y driven by a strong increase in benefits paid and health expenditure as well as election and defence spending.

- Investment was lacklustre across the board with it detracting 0.2pp driven by the public sector with private capex neutral.

- Net exports made its strongest contribution to GDP in two years. Exports rose 1.7% q/q to be up 1.5% y/y, while imports increased 1.4% q/q & 1.9% y/y, a sign of improving domestic demand.

- GDP/person rose 0.2% q/q to be up 0.2% y/y, the first annual rise since Q1 2023.

Australia domestic demand y/y%

Source: MNI - Market News/ABS

Fig 1: RBA Dated OIS Higher Post Q2 GDP

Source: Bloomberg Finance L.P./MNI

BONDS: NZGBS: Back End Yields Notably Higher, 2/10s Curve At +148bps

NZGB yields are flat to 6bps higher, led by the back end of the curve. The steepening theme evident globally has been seen strongly today in NZGB markets. The 2yr yield is barely changed and anchored sub 3.0% at this stage. The 10yr yield is up close to 6bps, last at 4.46% and closing the gap with pre RBNZ highs from August close to 4.50%. These moves leave the NZGB 2/10s curve at +148bps, closing in on April highs near +154bps.

- US Tsy futures initially moved higher in Wednesday Asia Pac trade, but this move has been faded. Cash Tsy yields sit 1-2bps higher in yield terms, with the back end leading. The US 2/10s curve sits at +63bps.

- Outside of US moves, NZ markets have also likely been impacted by ACGB yield gains. These were supported post the better than expected Q2 GDP print (although ACGB front end yields are notably higher, up 9bps for the 2-3yr tenors, compared to NZ's flat 2yr trend today).

- NZ's 2yr swap rate has edged a little higher, last near 2.775%.

- On the news front: " S&P Global Ratings is “comfortable” with New Zealand’s sovereign rating outlook, though it’s closely watching the nation’s current account and budget deficits." (via BBG).

- Data wise, the ANZ August commodity price index rose 0.7%m/m, after a -1.8% fall in July. Overnight we did have a softer whole milk powder auction result though.

FOREX: Asia FX Wrap - USD Shorts Being Pared Back Into NFP ?

The BBDXY has had a range of 1206.85 - 1208.92 in the Asia-Pac session, it is currently trading around 1208, +0.10%. The USD has again found some solid demand around the 1200 area and is again attempting to bounce higher off this base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD is looking comfortable for the moment above this support, not sure we get any clear direction though until the market sees what the NFP print is.

- EUR/USD - Asian range 1.1625 - 1.1645, Asia is currently trading 1.1630. The pair is drifting back towards its first support around 1.1550, firmly within its wider 1.1350-1.1850 range.

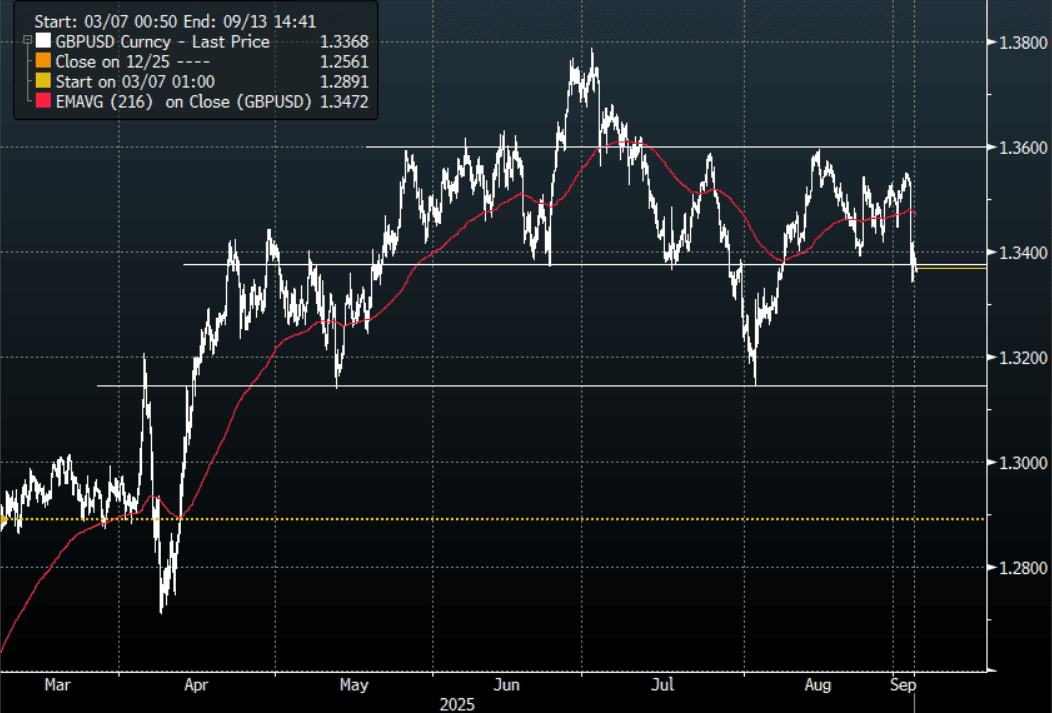

- GBP/USD - Asian range 1.3361 - 1.3394, Asia is currently dealing around 1.3370. The pair collapsed in response to moves in UK bonds. Price is now testing its support around 1.3350, a sustained break below here opens up a move back to 1.3100, the USD’s bounce will add to the sterling's headwinds.

- USD/CNH - Asian range 7.1354-7.1453, the USD/CNY fix printed 7.1108, Asia is currently dealing around 7.1450. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3535, US 10-Year 4.283%, BBDXY 1208, Crude Oil $65.41

- Data/Events : Italy HCOB PMI’s, EZ HCOB PMI’s & PPI, France HCOB PMI’s, Spain HCOB PMI’s, Germany HCOB PMI’s

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

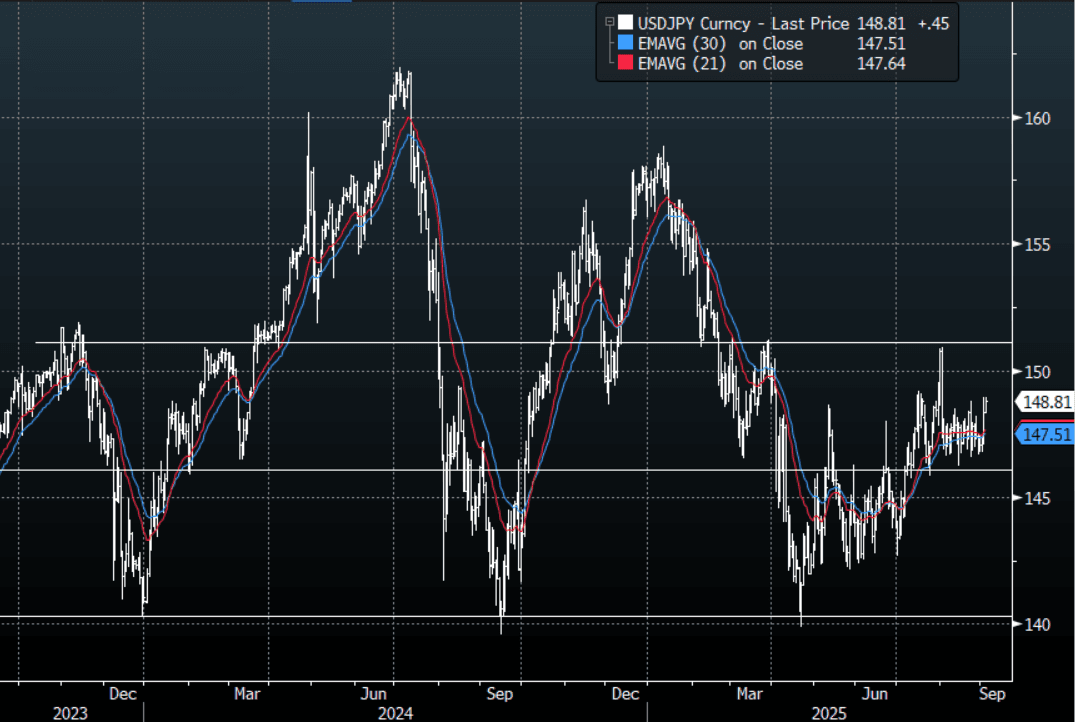

JPY: Asia Wrap - USD/JPY Back To Overnight Highs On A Potential Early Election

The Asia-Pac USD/JPY range has been 148.36-148.92, Asia is currently trading around 148.85, +0.32%. USD/JPY was bid all session moving back toward the overnight highs on a potential early election and 30-Year JGB’s blowing out to 3.28%. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. The price action looks pretty constructive but I would not be expecting any major extensions until the market has had a look at the NFP on Friday unless we get some other catalyst, could an early election be that ?

- Bloomberg - “Japan’s Long Bonds Join Global Slide as Politics Adds to Jitters. Yields on 20-year government bonds rose to 2.69%, the highest level since 1999, while those on the 30-year maturity jumped to 3.28%, the highest since debut.”

- "USD/JPY’s Upward Tilt Encouraged With LDP Early Election Report. USD/JPY is ticking higher after a report the LDP’s Aso is set to call for an early election. This comes as PM Ishiba’s tenure is looking vulnerable following news of a key ally’s intention to step down." - BBG

- “JAPAN LDP'S ASO SET TO CALL FOR EARLY PARTY ELECTION: MAINICHI" - BBG

- “S&P Global Japan Aug. Services PMI 53.1 vs 53.6 in July, S&P Global Japan Aug. Composite PMI 52 vs 51.6 in July" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.15($870m), 146.50($1.39b).Upcoming Close Strikes : 147.10($970m Sept 4), 146.00($2.16b Sept 5) - BBG.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

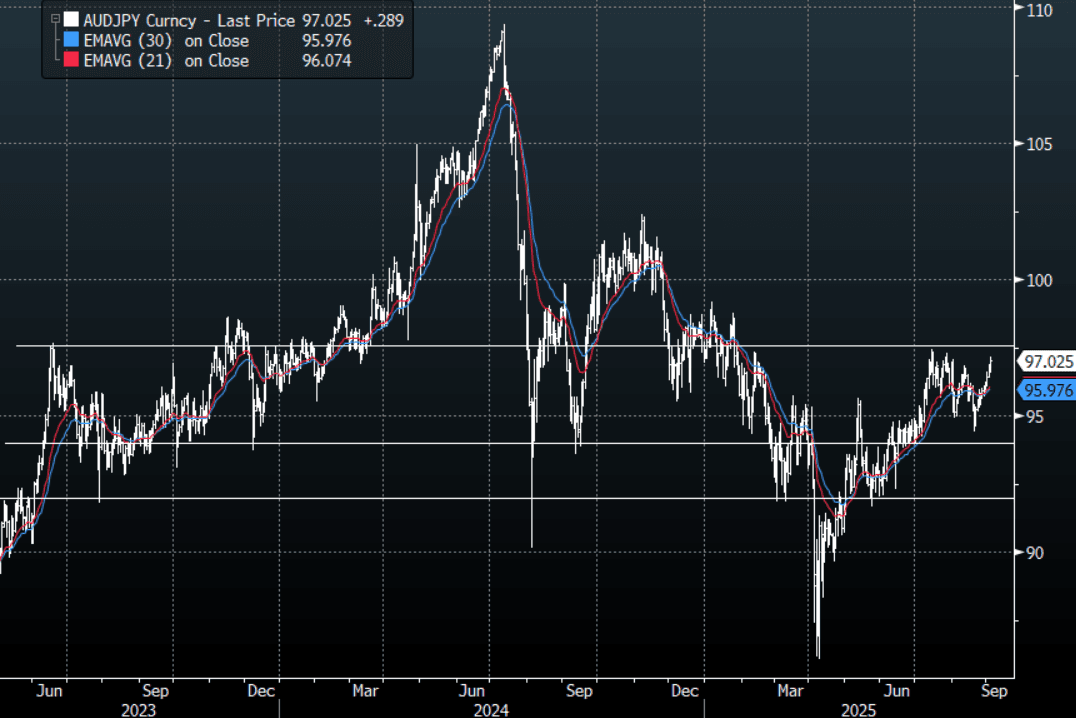

AUD: Asia Wrap - AUD/USD Fails To Push Higher On GDP

The AUD/USD has had a range of 0.6513 - 0.6525 in the Asia- Pac session, it is currently trading around 0.6520, +0.02%. The AUD tried to bounce on the better GDP data but could not follow through and has drifted back to its open. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- Q2 Boosted By Special Factors, H1 Averaged 0.4% q/q. Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook

- "S&P Global Australia Aug. Composite PMI 55.5 vs 53.8 Prior (pre 54.9), S&P Global Australia Aug. Services PMI 55.8 vs 54.1 in July(pre 55.1).” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD569m). Upcoming Close Strikes : 0.6400(AUD1.12b Sept 5), 0.6500(AUD974m Sept 5), 0.6600(AUD1b Sept 5) - BBG

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

- AUD/JPY - Asia-Pac range 96.59 - 97.15, Asia is trading around 97.00. The pair has broken back above 96.50 which starts to negate the downward direction, a sustained break above 97.50 is needed to reignite the upward trend. Until then looks to be 94.50 - 97.50.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

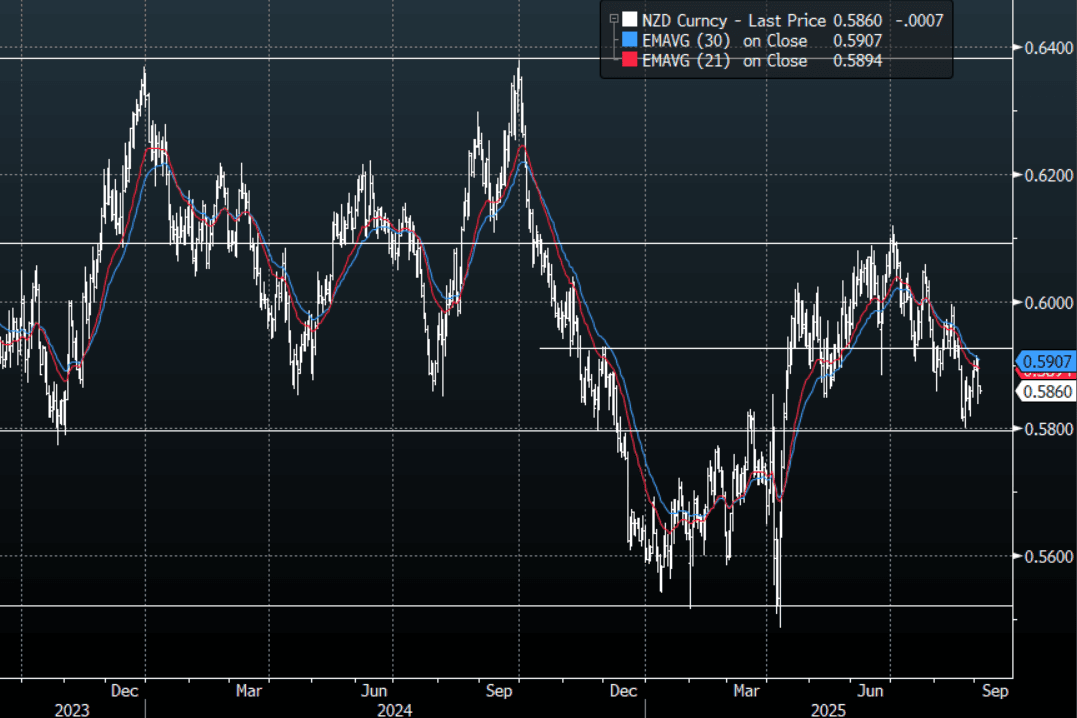

NZD: Asia Wrap - NZD/USD Drifts Lower After Rejecting 0.5900

The NZD/USD had a range of 0.5854 - 0.5867 in the Asia-Pac session, going into the London open trading around 0.5860, -0.12%. The NZD topped out above 0.5900 and moved lower with risk overnight. The NZD sellers should continue to be around looking to fade any bounce back towards the 0.5950 area initially. The USD finding some demand finally has helped put a top in above 0.5900 for now, though NFP on Friday will have a say in if that remains the case.

- Milk Power Auction Price Falls, Back To Late 2024 Levels : Overnight the average price for whole milk powder fell to $3809 versus $4036 at the previous auction, per GDT . This was a 5.3% drop. The whole milk powder price is now at fresh lows for 2025. The terms of trade proxy has matched this fall recently.

- "S&P Is Watching New Zealand’s Current Account, Budget Deficits. S&P Global Ratings is “comfortable” with New Zealand’s sovereign rating outlook, though it’s closely watching the nation’s current account and budget deficits." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD384m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- AUD/NZD range for the session has been 1.1112 - 1.1138, currently trading 1.1125. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Weak Day for China as Others Trend Sideways

The NIKKEI in Japan declined today as political uncertainty increased after Prime Minister Shigeru Ishiba’s key power broker announced his intention to resign with local media suggesting other key power brokers within the LDP are intending to quit. The move higher in developed market bond yields has seen a cautious day in Asia with China down across major bourses, whilst the bounce back in Jakarta continues.

- The NIKKEI is down in the Tokyo trading day by -0.80%, after yesterday's gains of +0.29%

- The major bourses in China are all down with the Hang Seng down -0.40%, CSI 300 down -0.88%, Shanghai down -0.96% and Shenzhen down -0.93%.

- The TAIEX in Taiwan is up marginally by +0.10%.

- The KOSPI has done very little today with gains of +0.08%

- In Malaysia, the FTSE Malay KLCI rose a mere +0.09%

- The Jakarta Composite is up +0.90% today after yesterday's gains of +0.85%.

- The Straits Times in Singapore is down -0.25% whilst the PSEi in the Philippines is down -0.80%

- The NIFT 50 has had a quiet start up just +0.08% after yesterday's losses of -0.18%

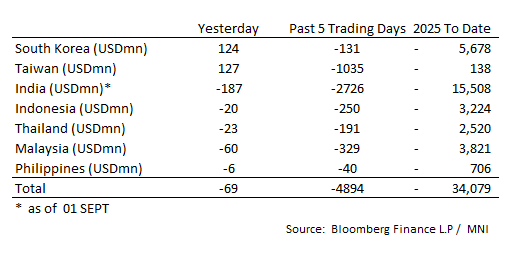

ASIA STOCKS: Large Outflows Moderate

Outflows from India continues, as others see modest inflows.

- South Korea: Recorded inflows of +$124m yesterday, bringing the 5-day total to -$131m. 2025 to date flows are -$5,678. The 5-day average is -$26m, the 20-day average is -$28m and the 100-day average of +$49m.

- Taiwan: Had inflows of +$127m yesterday, with total outflows of -$1,035 m over the past 5 days. YTD flows are negative at -$138. The 5-day average is -$207m, the 20-day average of -$180m and the 100-day average of +$176m.

- India: Had outflows of -$187m as of the 1st, with total outflows of -$2,726m over the past 5 days. YTD flows are negative -$15,508m. The 5-day average is -$545m, the 20-day average of -$225m and the 100-day average of -$15m.

- Indonesia: Had outflows of -$20m yesterday, with total outflows of -$250m over the prior five days. YTD flows are negative -$3,224m. The 5-day average is -$50m, the 20-day average +$30m and the 100-day average -$12m.

- Thailand: Recorded outflows of -$23m yesterday, with outflows totaling -$191m over the past 5 days. YTD flows are negative at -$2,520m. The 5-day average is -$38m, the 20-day average of -$31m and the 100-day average of -$14m.

- Malaysia: Recorded outflows as of -$60m yesterday, totaling -$329m over the past 5 days. YTD flows are negative at -$3,821m. The 5-day average is -$66m, the 20-day average of -$41m and the 100-day average of -$12m.

- Philippines: Recorded outflows of -$6m yesterday, with net outflows of -$40m over the past 5 days. YTD flows are negative at -$706m. The 5-day average is -$8m, the 20-day average of -$4m the 100-day average of -$5m.

Oil Lower But In A Narrow Range, Supply Events Remain Focus

Oil prices are moderately lower during today’s APAC session after rising around 1.5% on Tuesday as risk sentiment is weaker. WTI is down 0.3% to $65.41/bbl after rising to $65.72 earlier then falling to $65.35, a narrow range. Brent is 0.3% lower at $68.92/bbl following a peak of $69.24 and trough of $68.87. The USD index is up 0.1%.

- OPEC+ meets on September 7 to discuss the production target for October. It has increased output over the last few months adding to excess supply concerns but is expected to leave quotas unchanged this time.

- With a global market surplus expected in coming months, inventory data remain important. US industry-based data for last week are released Wednesday.

- Also in terms of supply, the market is watching for developments on the Russia-Ukraine conflict. Progress towards peace appears to have stalled and US Treasury Secretary Bessent said that “all options are on the table”. A move away from Russian crude would increase demand for other global supplies.

- Today the Fed’s Musalem speaks and the Beige Book is published. US July JOLTS job openings & orders, European August services/composite PMIs and July euro area PPI print. Also, ECB President Lagarde, RBA Governor Bullock and BoE Breeden speak.

Gold Retreats From New Record, Benefiting From Risk Appetite Pullback

Gold prices reached a new record high of $3546.96/oz during today’s APAC trading as risk appetite deteriorated. They usually move in the opposite direction to the US dollar but today (BBDXY +0.1%) and yesterday (BBDXY +0.5%) they have rallied despite USD strength. Expectations of Fed easing and concerns over attacks on central bank independence from the US administration have driven bullion higher, while the greenback appears to be normalising with its risk premium declining (calculated by Bloomberg).

- US yields are also higher again which would normally weigh on non-interest bearing gold but currently it appears that markets are nervous regarding rising government debt levels not just in the US, but also the UK and France.

- Gold is currently little changed on the day at $3533.5/oz. It broke above resistance at $3539.7 earlier today.

- Silver in contrast to gold is down 0.4% to $40.72/oz off the intraday low of $40.642.

- Equities are mixed with the S&P e-mini up 0.1% and TAIEX +0.3% but CSI 300 down 0.9% and ASX -1.6%. Oil prices are lower with WTI -0.3% to $65.41/bbl. Copper is 0.3% lower.

- Today the Fed’s Musalem speaks and the Beige Book is published. US July JOLTS job openings & orders, European August services/composite PMIs and July euro area PPI print. Also, ECB President Lagarde, RBA Governor Bullock and BoE Breeden speak.

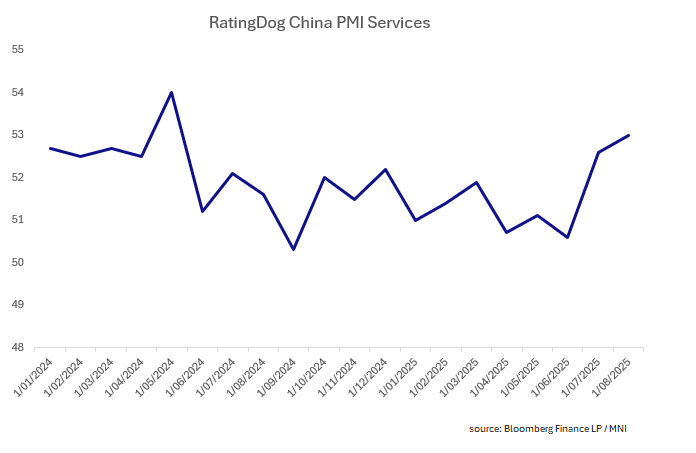

CHINA: RatingDog PMI Services Climbs in August

- The RatingDog services PMI rose to +53.0 in August, from +52.6 in July.

- The release was the highest since May 2024, and above forecasts.

- The employment component moderated to +48.7 from +50.9 and prices charged were down.

- The RatingDog manufacturing PMI jumped to 50.5 from 49.5 in July. The consensus forecast was 49.8 and we projected an unchanged reading at 49.5. This export-focused survey is in contrast to the official one which, with a print of 49.4, pointed to manufacturing contraction.

- The result is the RatingDog Composite is up to +51.9, its highest reading since November 2024.

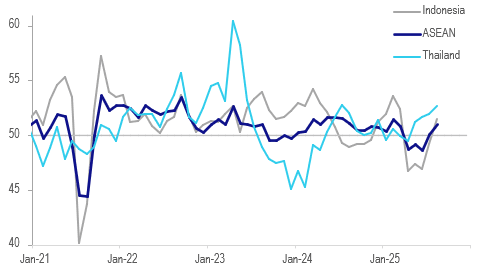

ASIA: ASEAN Manufacturing Sector Sees Improvement In August But Tentative

The S&P Global PMIs across ASEAN generally showed growth in activity in the sector in August with all countries positive except Malaysia. As a result, the aggregate ASEAN PMI rose to 51.0 last month up from 50.1, the highest since February, as moderately higher new orders drove production higher. But there are signs that businesses remain cautious.

- In July, business confidence fell to a 5-year low but improved sharply in August to its best since March but still below the historical average, according to S&P Global. But optimism regarding the outlook was not strong enough for firms to hire and staffing was reduced for the fifth straight month, although at a slower pace.

- New orders grew for the first time after contracting for 4 months.

- Input costs continued to rise but at a slower pace than in July. These were passed onto customers though with selling price inflation at its highest since end-2024.

- In August, Thailand showed the strongest manufacturing growth with the PMI up to 52.7, followed by Indonesia at 51.2, Singapore 51.2, Philippines 50.8, Vietnam & Mynamar 50.4, and Malaysia close to the neutral 50 at 49.9.

ASEAN S&P Global Manufacturing PMI sa

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 03/09/2025 | 0700/0300 | * | Turkey CPI | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0730/0930 | ECB Lagarde Speaks at ESRB Conference | ||

| 03/09/2025 | 0730/0830 | BOE Mann at Signum's London Westminster Day roundtable | ||

| 03/09/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0815/0915 | BOE Breeden at Innovation in Money and Payments Conference | ||

| 03/09/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/09/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/09/2025 | 0900/1100 | ** | EZ PPI | |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book | ||

| 04/09/2025 | 0130/1130 | ** | Trade Balance | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0630/0830 | *** | CPI | |

| 04/09/2025 | 0700/0900 | ** | Unemployment | |

| 04/09/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/09/2025 | 0830/0930 | Decision Maker Panel data | ||

| 04/09/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/09/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 04/09/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 04/09/2025 | 0930/1130 | ECB Cipollone Speaks at Digital Euro Hearing, European Parliament | ||

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI |