BONDS: NZGBS: Back End Yields Notably Higher, 2/10s Curve At +148bps

NZGB yields are flat to 6bps higher, led by the back end of the curve. The steepening theme evident globally has been seen strongly today in NZGB markets. The 2yr yield is barely changed and anchored sub 3.0% at this stage. The 10yr yield is up close to 6bps, last at 4.46% and closing the gap with pre RBNZ highs from August close to 4.50%. These moves leave the NZGB 2/10s curve at +148bps, closing in on April highs near +154bps.

- US Tsy futures initially moved higher in Wednesday Asia Pac trade, but this move has been faded. Cash Tsy yields sit 1-2bps higher in yield terms, with the back end leading. The US 2/10s curve sits at +63bps.

- Outside of US moves, NZ markets have also likely been impacted by ACGB yield gains. These were supported post the better than expected Q2 GDP print (although ACGB front end yields are notably higher, up 9bps for the 2-3yr tenors, compared to NZ's flat 2yr trend today).

- NZ's 2yr swap rate has edged a little higher, last near 2.775%.

- On the news front: " S&P Global Ratings is “comfortable” with New Zealand’s sovereign rating outlook, though it’s closely watching the nation’s current account and budget deficits." (via BBG).

- Data wise, the ANZ August commodity price index rose 0.7%m/m, after a -1.8% fall in July. Overnight we did have a softer whole milk powder auction result though.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - JPY Surges On US Rates And Risk Correcting Lower

The Equity market correction accelerated lower on Friday in response to the NFP data and the implications it has for growth going forward. This morning has seen US futures open a little higher, pulling back a little from Friday’s lows, ESU5 +0.37%, NQU5 +0.40%. The Yen got the double whammy of the move in US rates and as a safe haven as risk wobbled off its highs. Should we see a deeper correction lower in risk I suspect the JPY will continue to outperform in the crosses.

- EUR/JPY - Friday night range 170.29 - 172.23, Asia is trading around 171.05. This pair had a strong bounce last week off its support around 170.00 as JPY longs got squeezed out, but this potential correction lower in risk could add to the pair's headwinds. Watch for any signs of topping out should risk actually start correcting lower, a move sub 169.50/170.00 could signal a deeper pullback is on the cards.

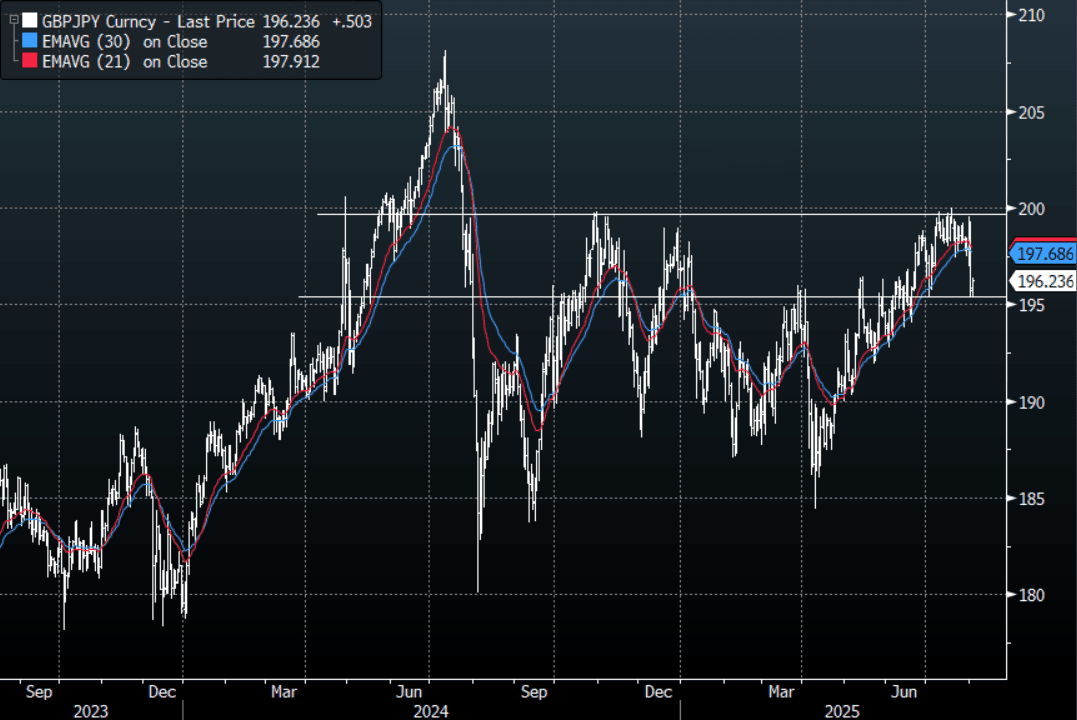

- GBP/JPY - Friday night 195.34 - 198.99, Asia trades around 196.20. The pair sliced through its support around 197.00 and has moved very quickly towards the 195.00 support. The move higher looks to have stalled for now and a sustained break below 195.00 would turn momentum lower again. A bounce back towards 197.00/197.50 should now see sellers.

- NZD/JPY - Friday night range 87.06 - 88.54, Asia is currently dealing 87.40. The pair failed with multiple attempts to break above 89.00. A top looks to potentially be in place now and a break sub 96.50 could signal a deeper correction, expect sellers on any back towards 88.00 initially.

- CNH/JPY - Friday night range 20.4782 - 20.8750, Asia is currently trading around 20.5600. This pair broke through its 20.7000/20.8000 resistance area last week but the price action was pretty ugly as the move higher was rejected in what looks a key day reversal. Initial support is around the 20.40 area but a sustained break back below 2.3000 would begin to turn momentum lower again.

Fig 1 : GBP/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Off Highs As US Tsys Turn Lower, Fiscal Discussions In Focus Onshore

JGB futures sit comfortably earlier highs. We are 138.67, +.59 at the lunchtime break. US Tsy futures are now comfortably lower for the session, unwinding the early bounce. There has also been flows going through in the TSY futures space, which may be contributing to the recent softness. This obviously follows the very sharp rallies we saw on Friday post the US data outcomes.

- For cash JGB yields, we are still mostly down in yield terms, but away from worst levels for the session. The 10yr is back around 1.51%. The 3-7yr tenors are -6 to -7bps down in yield terms. Swap rates are little changed, except for a firmer back end yield backdrop.

- News flow has seen focus on the fiscal outlook, with the following headlines crossing. "*ISHIBA: IMPLEMENTATION OF SUBSIDIES DEPENDS ON TALKS W PARTIES" - BBG, along with "*CDP'S NODA: TO DISCUSS SALES TAX CUT W OTHER OPPOSITION PARTIES, and {JN} "*ISHIBA: MUST MULL HOW SALES TAX CUT MAY IMPACT YIELDS, TRUST" - BBG.

- The LDP coalition has not been in favour of cutting the sales tax, but it is likely to remain on the agenda to some degree.

- Note tomorrow we have a 10yr bond auction.

NEW ZEALAND: Labour Market Data Likely Deteriorated In Q2

The focus of the week will be the Q2 labour market data published on Wednesday. It is expected to show that it weakened in the quarter after some signs of stabilisation in Q1. The unemployment rate is forecast to rise 0.2pp to 5.3% more than the RBNZ’s 5.2% May projection. If the data print as weak as or weaker than the Bloomberg consensus, then a rate cut on August 20 is likely.

- Consensus is forecasting a 0.1% q/q drop in employment driving the annual rate down to -0.9% after -0.7% in Q1. This follows the monthly filled jobs data showing a contraction of 0.3% q/q in Q2. The participation rate is expected to fall 0.1pp to 70.7%. Private wage growth may pick up to 0.5% q/q from 0.4% in Q1.

- RBNZ reported inflation expectations for Q3 are out on Thursday. With the central bank concerned about some recent increase in inflation, the series will be monitored closely ahead of the August 20 decision. The 2-year ahead measure rose 0.2pp to 2.3% in Q2.

- ANZ commodity prices for July are released on Tuesday. They fell 2.3% m/m in June.

- Cotality July home values print late Tuesday night local time. The housing market has been lacklustre over recent months but values rose 0.2% m/m in June. Another positive in July may signal a turning point.