JGBS: Back End Yields Higher, But Away From Best Levels, 30yr Auction Tomorrow

JGB futures have maintained a negative bias, with the Sep future last near 137.34, -.18 versus settlement levels. We haven't tested sub 137.20 so far (session lows rest at 137.23). Broader trends have been skewed towards weaker futures with US 10yr futures back to flat after initially opening firmer. Aussie bond futures are down sharply, aided by a better Q2 GDP outcome.

- The initial impetus in the cash JGB space was for steeper curves, led by the 20-40yr tenors. We sit away from session extremes though. The 10yr outright yield was last near 1.63%, little changed for the session.

- The 30yr was close to 3.26%, earlier highs were around 3.29%. The 2/30s JGB curve was last around +240bps (sessions highs were at +242bps). The 40yr was last up 3bps, near 3.50%, the 20yr around 2.67%, up 3bps.

- BOJ Governor Ueda met with PMI Ishiba to discuss the economy/markets. Ueda reiterated they will raise rates if the economy, prices move in line with forecasts.

- Domestic politics will remain in focus as well: "JAPAN LDP'S ASO SET TO CALL FOR EARLY PARTY ELECTION: MAINICHI" - BBG.

- The strong focus for tomorrow will be on the 30yr debt auction.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Asia Wrap - NZD/USD Consolidates Just Above 0.5900

The NZD/USD had a range of 0.5903 - 0.5923 in the Asia-Pac session, going into the London open trading around 0.5920, +0.03%. US Yields collapsed in response to the NFP data which sparked a kneejerk response lower in the USD. This was also a very bad day for US stocks which finally look to be pulling back from elevated levels. The question for the NZD going forward is does the USD see sellers quickly return in response to the move in rates, or can the USD rise from the ashes and return as a safe haven. NZD/USD bounced nicely off its 0.5850 support but would suspect sellers would return on any bounce back toward 0.6000 initially as the market decides how best to trade the USD.

- “AUCKLAND JULY AVERAGE HOUSE PRICE FALLS 2.4% Y/Y: BARFOOT" - BBG

- NEW ZEALAND: Labour Market Data Likely Deteriorated In Q2. The focus of the week will be the Q2 labour market data published on Wednesday. It is expected to show that it weakened in the quarter after some signs of stabilisation in Q1. The unemployment rate is forecast to rise 0.2pp to 5.3% more than the RBNZ’s 5.2% May projection. If the data print is as weak as or weaker than the Bloomberg consensus, then a rate cut on August 20 is likely.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD3496m Aug 7). - BBG

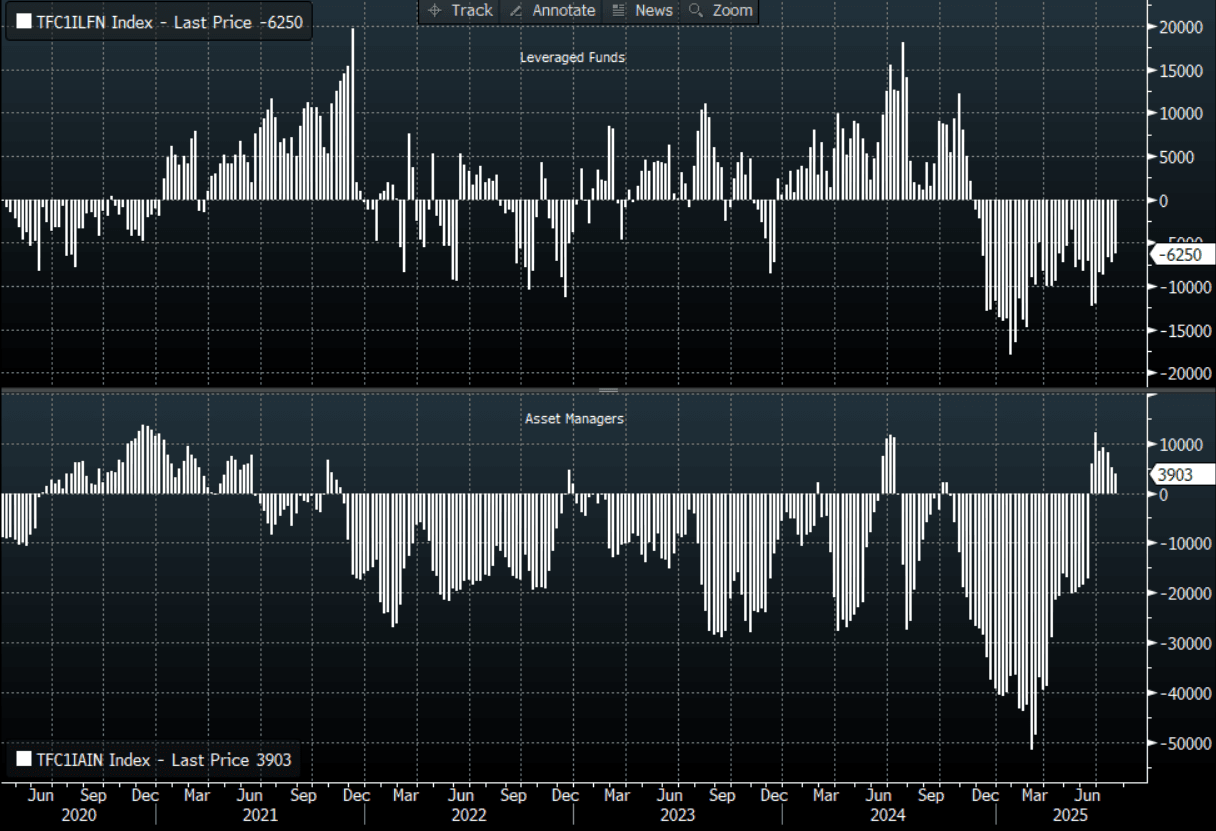

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +3903(Last +5034), the Leveraged community reduced their shorts slightly -6250(Last -7328).

- AUD/NZD range for the session has been 1.0930 - 1.0959, currently trading 1.0950. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Bounces Into The Fix, Demand Fails Towards 148.00

The Asia-Pac USD/JPY range has been 147.06 - 147.91, Asia is currently trading around 147.60, +0.12%. USD/JPY reacted to the capitulation in US yields and had a kneejerk move lower. The JPY got the double whammy of the move in rates and as a safe haven as risk wobbled off its highs. Price moved very quickly away from the pivotal 151/152 area much to the relief of Institutional JPY longs and the BOJ. The Pair opens in Asia testing its first support around 147.00, the more important level will be around 145.00. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. A move sub 145.00 would turn momentum lower once more, until then the 145.00-151-00 range should dominate. USD/JPY moved higher into the Japanese fix, I suspect the price will find it tough back towards 148.50 initially.

- News flow has seen focus on the fiscal outlook, with the following headlines crossing. "ISHIBA: IMPLEMENTATION OF SUBSIDIES DEPENDS ON TALKS W PARTIES" - BBG, along with "*CDP'S NODA: TO DISCUSS SALES TAX CUT W OTHER OPPOSITION PARTIES, and "ISHIBA: MUST MULL HOW SALES TAX CUT MAY IMPACT YIELDS, TRUST" - BBG.

- Otavio Costa on X: “ The yen just recorded its biggest one-day gain against the US dollar since December 2022, when the BoJ loosened its yield curve control and allowed 10-year yields to rise. This isn’t just a one-off move, in my view, it’s part of a broader fiscal survival response. The reality is that both the US dollar and interest rates must come down, in my opinion. This kind of fiscal and monetary adjustment isn’t optional — it’s the last viable path to avoid the US economy hitting a debt wall.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 149.50($752m), 150.00($1.16b), 150.50($967m).Upcoming Close Strikes : 147.65($1.14b Aug 7) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Futures Off Highs, Inflation Gauge Up But Mkt Following Tsys

Australian bond futures sit off earlier highs. The 3yr (YM) got above 96.70 in early dealings, but sits back near 96.65 currently, still +.105 for the session. The 10yr future (XM) got above 95.80, but is now back at 95.72, +.065 for the session.

- Like elsewhere news flow has been fairly light so far today. This has left market largely following US moves, which pared earlier gains. Broader risk appetite has held up ok, which has likely aided some yield retracement (albeit very modest with Friday's yield losses).

- On the data front, the Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA's 2-3% target band and may rise in coming months.

- In a week of second tier data, the focus is likely to be on Tuesday’s June household spending data which will now replace retail sales, which had its last print last week. The Q2 chain volume measure is also out. Bloomberg consensus expects June consumption values to rise 0.8% m/m to be up 4.9% y/y after 4.2% in May. The ABS noted that discounting in the month had boosted June retail sales.