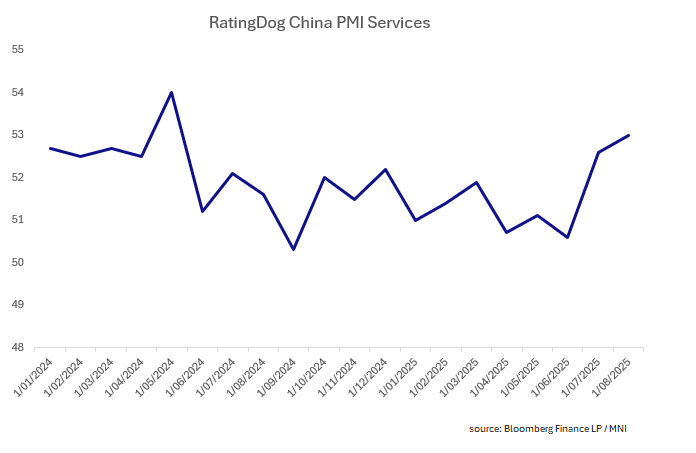

CHINA: RatingDog PMI Services Climbs in August

- The RatingDog services PMI rose to +53.0 in August, from +52.6 in July.

- The release was the highest since May 2024, and above forecasts.

- The employment component moderated to +48.7 from +50.9 and prices charged were down.

- The RatingDog manufacturing PMI jumped to 50.5 from 49.5 in July. The consensus forecast was 49.8 and we projected an unchanged reading at 49.5. This export-focused survey is in contrast to the official one which, with a print of 49.4, pointed to manufacturing contraction.

- The result is the RatingDog Composite is up to +51.9, its highest reading since November 2024.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

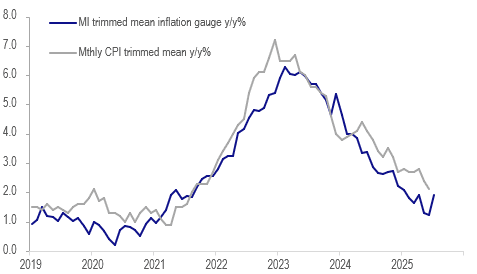

AUSTRALIA DATA: MI Underlying Inflation Gauge Rises Signalling Possible Trough

The Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA’s 2-3% target band and may rise in coming months. The headline inflation gauge has less signal to it. Currently the RBA remains focussed on quarterly CPI data but a more complete monthly series will be released in November.

Australia trimmed mean inflation y/y%

ASIA STOCKS: Mostly Outflows At The End Of Last Week, Taiwan Still Positive

At the end of last week, only Taiwan saw positive inflows into local equities from offshore investors. South Korea saw a very sharp drop in the Kospi on Friday, down 3.88%. We are higher today, last around +1% for the index. Near term focus remains on local government tax shifts. The ruling party will reportedly make its position on capital gains tax known soon: "South Korea’s ruling Democratic Party chief Jung Chung-rae said the party will determine its position on capital gains tax as quickly as possible and inform the public." (via BBG a short while ago).

- More broadly inflow sentiment may be dictated by global equity trends. Friday's NFP report and ISM dip cast a shadow over the US equity market outlook. Futures are are higher in the first part of trade today, with Eminis up around 0.25%.

- Taiwan inflows remained positive, albeit with the 5-day rolling sum of inflows cooler that what we saw through parts of July.

- Indian outflow momentum remained strong to the end of last month. Higher tariff rates have likely weighed on sentiment. The Nifty is back at levels from mid June.

- Thailand also saw outflows on Friday, unwinding some of the recent positive inflows seen.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -549 | 931 | -5483 |

| Taiwan (USDmn) | 171 | 821 | 2516 |

| India (USDmn)* | -703 | -2000 | -11007 |

| Indonesia (USDmn) | -4 | -142 | -3753 |

| Thailand (USDmn) | -58 | 47 | -1837 |

| Malaysia (USDmn) | -3 | -89 | -2949 |

| Philippines (USDmn) | -1 | -8 | -623 |

| Total (USDmn) | -1148 | -441 | -23137 |

| * Data Up To July 31 |

Source: Bloombegr Finance L.P./MNI

CHINA PRESS: PBOC To Balance Growth With Stabilising Risk

China’s central bank is expected to carefully balance stabilizing growth with mitigating risks, with emphasis on technological innovation and financial stability, alongside the flexible application of policy tools and structural reforms, according to Tian Lihui, professor of finance at Nankai University, following the People’s Bank of China’s 2025 second-half work conference last week. Tian noted that the PBOC will likely deploy measures such as reserve requirement ratio (RRR) cuts and the Medium-term Lending Facility (MLF) to ensure ample liquidity, with the primary focus in H2 on revitalising existing funds through optimising credit allocation, curbing idle capital and enhancing capital efficiency.