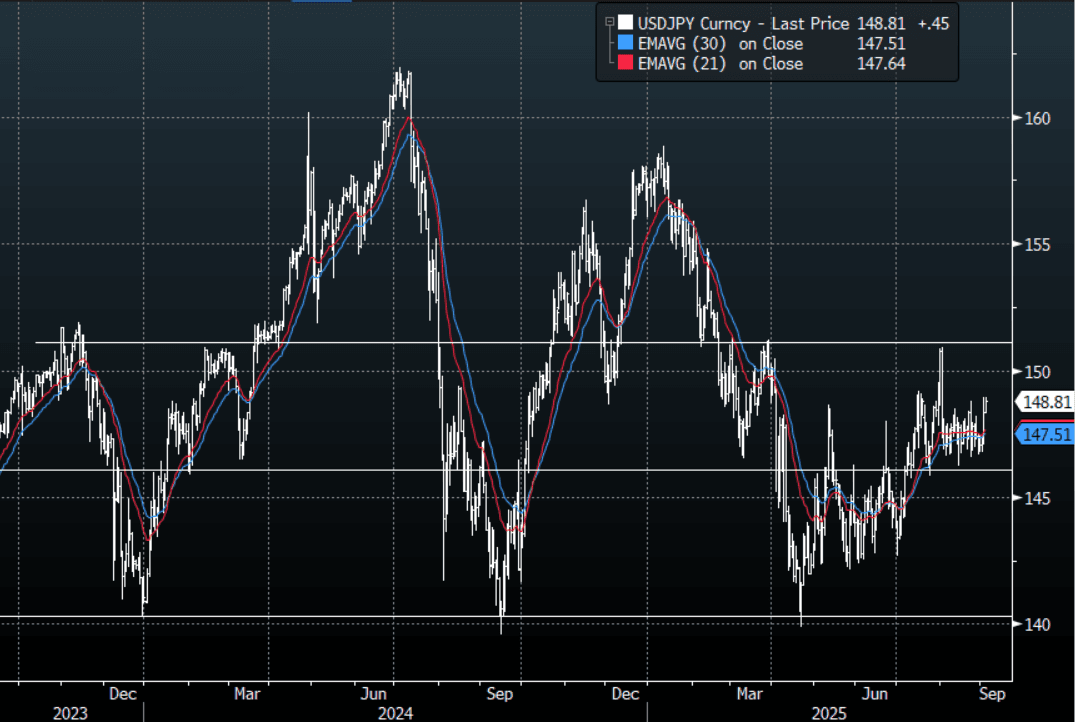

JPY: Asia Wrap - USD/JPY Back To Overnight Highs On A Potential Early Election

The Asia-Pac USD/JPY range has been 148.36-148.92, Asia is currently trading around 148.85, +0.32%. USD/JPY was bid all session moving back toward the overnight highs on a potential early election and 30-Year JGB’s blowing out to 3.28%. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. The price action looks pretty constructive but I would not be expecting any major extensions until the market has had a look at the NFP on Friday unless we get some other catalyst, could an early election be that ?

- Bloomberg - “Japan’s Long Bonds Join Global Slide as Politics Adds to Jitters. Yields on 20-year government bonds rose to 2.69%, the highest level since 1999, while those on the 30-year maturity jumped to 3.28%, the highest since debut.”

- "USD/JPY’s Upward Tilt Encouraged With LDP Early Election Report. USD/JPY is ticking higher after a report the LDP’s Aso is set to call for an early election. This comes as PM Ishiba’s tenure is looking vulnerable following news of a key ally’s intention to step down." - BBG

- “JAPAN LDP'S ASO SET TO CALL FOR EARLY PARTY ELECTION: MAINICHI" - BBG

- “S&P Global Japan Aug. Services PMI 53.1 vs 53.6 in July, S&P Global Japan Aug. Composite PMI 52 vs 51.6 in July" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.15($870m), 146.50($1.39b).Upcoming Close Strikes : 147.10($970m Sept 4), 146.00($2.16b Sept 5) - BBG.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

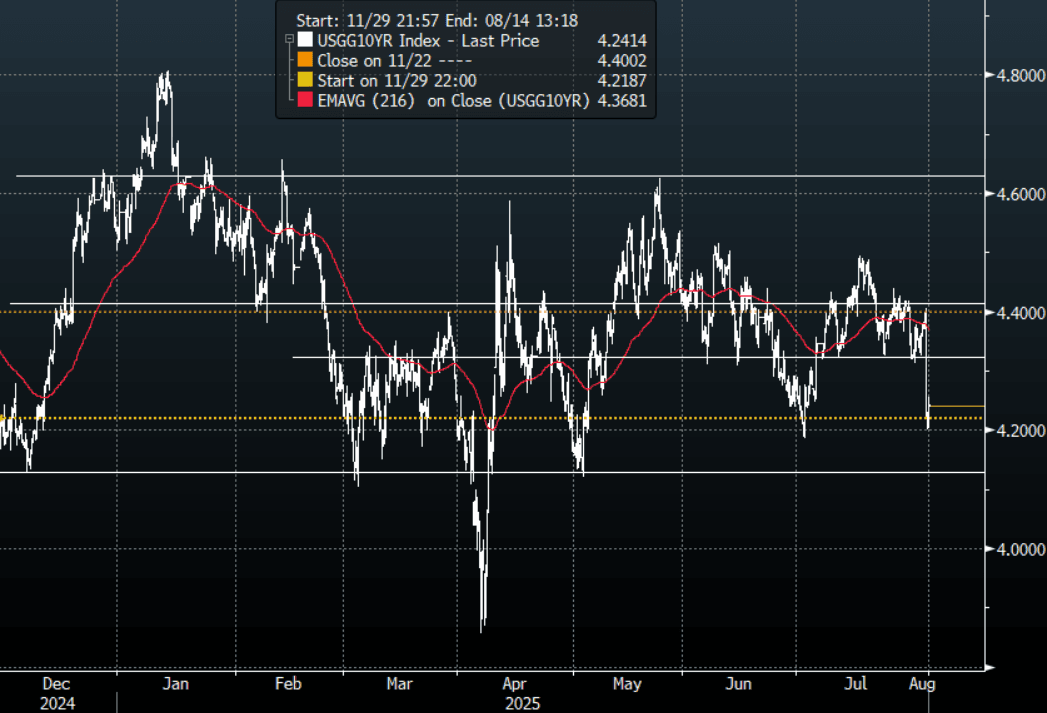

US TSYS: Asia Wrap - Yields Retrace Some Of Friday's Moves

The TYU5 range has been 112 to 112-12 during the Asia-Pacific session. It last changed hands at 112-03+, down 0-03 from the previous close.

- The US 2-year yield has bounced off Friday’s lows trading around 3.696%, up 0.01 from its close.

- The US 10-year yield has also bounced off Friday’s lows trading around 4.241%, up 0.03 from its close.

- (Bloomberg) -- “A block of 2,300 contracts in 10-year bond September futures traded at a price of 114-03 on CBOT. A total of 53,897 contracts traded so far in this session.” There were also multiple block trades executed in both the five-year and two-year contracts.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area. The move was even more aggressive in the 2-year which has rejected the move back towards 4% and now looks to target the pivotal 3.50% area.

- Wei Li(CIS BlackRock) on LinkedIn: “I don’t envy Powell, the Fed challenge is real:

- Slower growth - we had expected tariffs to slow US growth to about HALF its potential, and now it looks like the economy is already there. 3-month average payroll gains of just 35k is below our breakeven estimate of 60-80k, that accounts for demographics and softening immigration flows. Tariffs and trade are distorting other data such as gdp, but it is less the case with labour data/nfp.”

- “Persistent inflation pressure - average hourly earnings rose on the month, puzzlingly strong given weak job creation, although partly attributable to slower immigration crimping labour supply. Furthermore, tariffs are starting to feed through and could further push up goods prices.”

- CrossBorder Capital on X: “US Treasuries looking pretty stable despite the noise!? Term premia decoupling favorably from RoW. Zero evidence of loss of safe haven quality.”

- Data/Events: Factory Orders, Durable Goods

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

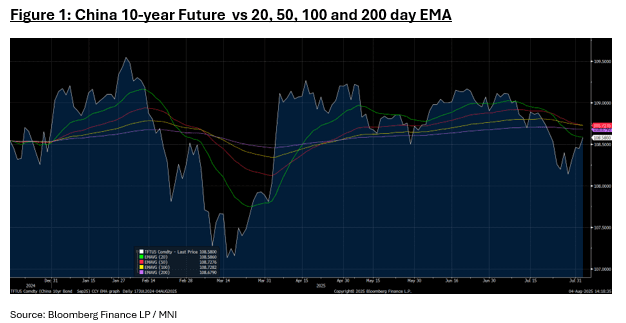

CHINA: Bond Futures Join the Rally

- China's bond futures joined in on the global rally following the US moves on Friday night.

- The 10-year future is up +0.13 to 108.58, touching the 20-day EMA.

- China's 2-year bond future is up +0.03 at 102.37 and sits just below the 20-day EMA of 102.38.

- The CGB10yr is -1bp at 1.68%.

BONDS: NZGB Yields Down But Away From Worst Levels, US Tsy Yields Edge Higher

NZGB yields sit lower, but are away from session lows. We are around 4-5.5bps lower across the benchmarks, with the 15-30yr tenors slightly lagging the other tenors. The 2yr yield is under 3.19%, while the 10yr is back to 4.45%. The 2yr is threatening multi month lows, while the 10yr is around mid range.

- The pick up in US Tsy yields (around +2-3bps across the curve), has helped pull NZGB yields up from session lows.

- In the swap space, the 2yr is holding under 3.00%, off 5bps so far today. The 10yr couldn't sustain an earlier move under 3.90%, last close to 3.92%, off around 4bps.

- The local news flow has been very light with no data out today. Market focus has been on spill over from the Tsy yield plunge on Friday. So far today risk appetite has held up ok, which has likely aided some yield retracement.

- The main data event this week will be Wednesday's Q2 labour market report. It is likely to show a contraction in employment and a further pickup in the unemployment rate and as a result further moderation in wage inflation. Q2 filled jobs fell 0.3% q/q after -0.1% signalling that there was job shedding in the quarter. The unemployment rate was stable in Q1 at 5.1%, helped by a 0.1pp fall in the participation rate, but this was up almost 2pp since the Q1 2022 trough. The economic recovery remains lacklustre despite 225bp of easing and thus given the lags the labour market is yet to pickup again.