GOLD: Gold Retreats From New Record, Benefiting From Risk Appetite Pullback

Gold prices reached a new record high of $3546.96/oz during today’s APAC trading as risk appetite deteriorated. They usually move in the opposite direction to the US dollar but today (BBDXY +0.1%) and yesterday (BBDXY +0.5%) they have rallied despite USD strength. Expectations of Fed easing and concerns over attacks on central bank independence from the US administration have driven bullion higher, while the greenback appears to be normalising with its risk premium declining (calculated by Bloomberg).

- US yields are also higher again which would normally weigh on non-interest bearing gold but currently it appears that markets are nervous regarding rising government debt levels not just in the US, but also the UK and France.

- Gold is currently little changed on the day at $3533.5/oz. It broke above resistance at $3539.7 earlier today.

- Silver in contrast to gold is down 0.4% to $40.72/oz off the intraday low of $40.642.

- Equities are mixed with the S&P e-mini up 0.1% and TAIEX +0.3% but CSI 300 down 0.9% and ASX -1.6%. Oil prices are lower with WTI -0.3% to $65.41/bbl. Copper is 0.3% lower.

- Today the Fed’s Musalem speaks and the Beige Book is published. US July JOLTS job openings & orders, European August services/composite PMIs and July euro area PPI print. Also, ECB President Lagarde, RBA Governor Bullock and BoE Breeden speak.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGB Yields Down But Away From Worst Levels, US Tsy Yields Edge Higher

NZGB yields sit lower, but are away from session lows. We are around 4-5.5bps lower across the benchmarks, with the 15-30yr tenors slightly lagging the other tenors. The 2yr yield is under 3.19%, while the 10yr is back to 4.45%. The 2yr is threatening multi month lows, while the 10yr is around mid range.

- The pick up in US Tsy yields (around +2-3bps across the curve), has helped pull NZGB yields up from session lows.

- In the swap space, the 2yr is holding under 3.00%, off 5bps so far today. The 10yr couldn't sustain an earlier move under 3.90%, last close to 3.92%, off around 4bps.

- The local news flow has been very light with no data out today. Market focus has been on spill over from the Tsy yield plunge on Friday. So far today risk appetite has held up ok, which has likely aided some yield retracement.

- The main data event this week will be Wednesday's Q2 labour market report. It is likely to show a contraction in employment and a further pickup in the unemployment rate and as a result further moderation in wage inflation. Q2 filled jobs fell 0.3% q/q after -0.1% signalling that there was job shedding in the quarter. The unemployment rate was stable in Q1 at 5.1%, helped by a 0.1pp fall in the participation rate, but this was up almost 2pp since the Q1 2022 trough. The economic recovery remains lacklustre despite 225bp of easing and thus given the lags the labour market is yet to pickup again.

INDONESIA: VIEW: JP Morgan Sees 50bp H2 Cuts As Growth Sub-Trend & Core Eases

Indonesian headline CPI jumped to 2.4% y/y in July from 1.9%, its highest in just over a year due to food prices. Core moderated 0.1.pp to 2.3% from 2.4%. It appears to have peaked around 2.5% in April. With inflation around the mid-point of BI’s band and signs of softer consumption, JP Morgan expects another 50bp of easing in H2 2025, dependent on rupiah stability.

- JP Morgan continues “to see core inflation averaging 2.3%oya this year, but now see it dipping below 2%oya in 4Q25 — below the midpoint of BI’s 1.5-3.5% target range. Together with consecutive below-trend GDP prints — we expect 2Q growth to print at 4.9%oya — we think this should lead BI to cut by 25bp at alternate meetings in September and December, but potential easing remains tightly tied to IDR stability”.

- “Excluding volatile food and energy prices, however, the momentum on core CPI has eased sharply over the last few months, sliding from over a 3%ar to 2%ar in the July inflation report. Within the core basket, this easing in momentum is most clearly evident in recreation and food and accommodation services, which signals a softness in underlying private consumption, in our view.”

- “In sequential terms, headline CPI rose 0.3%m/m, sa (0.252% to higher precision) while core CPI posted another soft 0.1%m/m, sa gain. Despite the firm July gain, distortions from recent food price swings and electricity tariff adjustments nonetheless pulled down the 3m/3m run-rate on headline CPI from an elevated 8%ar to 4.5%ar.”

- “The momentum on core CPI also softened to a 2%ar after averaging close to a 3%ar in 1H25, pointing to benign underlying inflationary pressures and, likely, soft domestic demand.”

FOREX: JPY Crosses - JPY Surges On US Rates And Risk Correcting Lower

The Equity market correction accelerated lower on Friday in response to the NFP data and the implications it has for growth going forward. This morning has seen US futures open a little higher, pulling back a little from Friday’s lows, ESU5 +0.37%, NQU5 +0.40%. The Yen got the double whammy of the move in US rates and as a safe haven as risk wobbled off its highs. Should we see a deeper correction lower in risk I suspect the JPY will continue to outperform in the crosses.

- EUR/JPY - Friday night range 170.29 - 172.23, Asia is trading around 171.05. This pair had a strong bounce last week off its support around 170.00 as JPY longs got squeezed out, but this potential correction lower in risk could add to the pair's headwinds. Watch for any signs of topping out should risk actually start correcting lower, a move sub 169.50/170.00 could signal a deeper pullback is on the cards.

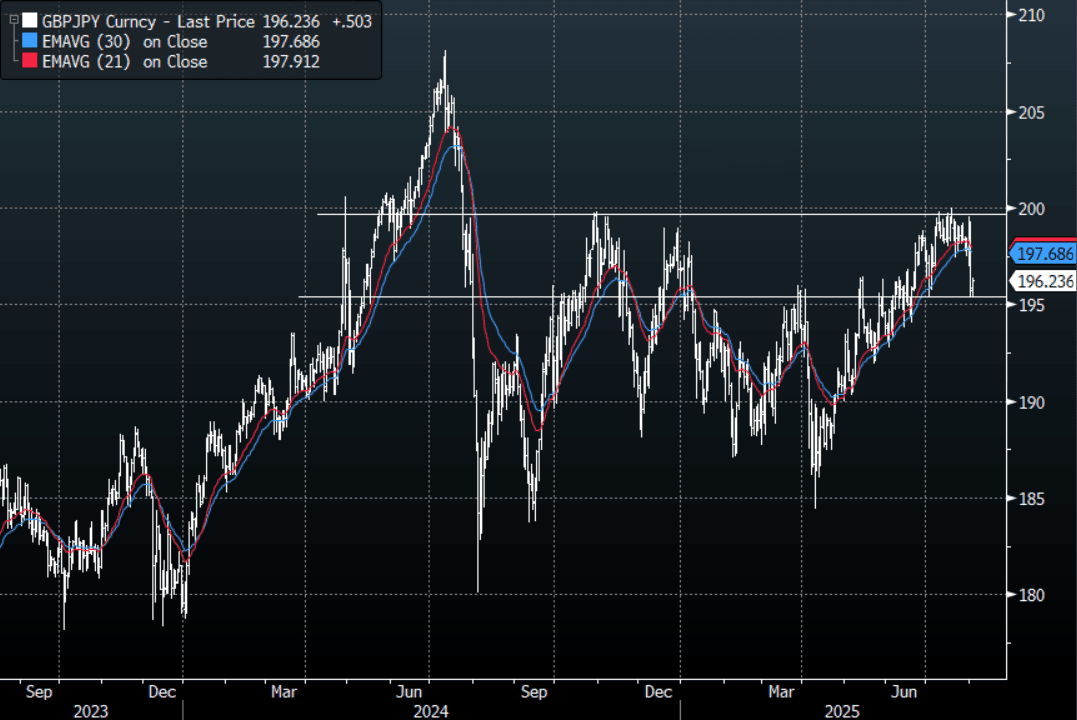

- GBP/JPY - Friday night 195.34 - 198.99, Asia trades around 196.20. The pair sliced through its support around 197.00 and has moved very quickly towards the 195.00 support. The move higher looks to have stalled for now and a sustained break below 195.00 would turn momentum lower again. A bounce back towards 197.00/197.50 should now see sellers.

- NZD/JPY - Friday night range 87.06 - 88.54, Asia is currently dealing 87.40. The pair failed with multiple attempts to break above 89.00. A top looks to potentially be in place now and a break sub 96.50 could signal a deeper correction, expect sellers on any back towards 88.00 initially.

- CNH/JPY - Friday night range 20.4782 - 20.8750, Asia is currently trading around 20.5600. This pair broke through its 20.7000/20.8000 resistance area last week but the price action was pretty ugly as the move higher was rejected in what looks a key day reversal. Initial support is around the 20.40 area but a sustained break back below 2.3000 would begin to turn momentum lower again.

Fig 1 : GBP/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P