OIL: Oil Lower But In A Narrow Range, Supply Events Remain Focus

Oil prices are moderately lower during today’s APAC session after rising around 1.5% on Tuesday as risk sentiment is weaker. WTI is down 0.3% to $65.41/bbl after rising to $65.72 earlier then falling to $65.35, a narrow range. Brent is 0.3% lower at $68.92/bbl following a peak of $69.24 and trough of $68.87. The USD index is up 0.1%.

- OPEC+ meets on September 7 to discuss the production target for October. It has increased output over the last few months adding to excess supply concerns but is expected to leave quotas unchanged this time.

- With a global market surplus expected in coming months, inventory data remain important. US industry-based data for last week are released Wednesday.

- Also in terms of supply, the market is watching for developments on the Russia-Ukraine conflict. Progress towards peace appears to have stalled and US Treasury Secretary Bessent said that “all options are on the table”. A move away from Russian crude would increase demand for other global supplies.

- Today the Fed’s Musalem speaks and the Beige Book is published. US July JOLTS job openings & orders, European August services/composite PMIs and July euro area PPI print. Also, ECB President Lagarde, RBA Governor Bullock and BoE Breeden speak.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Futures Off Highs, Inflation Gauge Up But Mkt Following Tsys

Australian bond futures sit off earlier highs. The 3yr (YM) got above 96.70 in early dealings, but sits back near 96.65 currently, still +.105 for the session. The 10yr future (XM) got above 95.80, but is now back at 95.72, +.065 for the session.

- Like elsewhere news flow has been fairly light so far today. This has left market largely following US moves, which pared earlier gains. Broader risk appetite has held up ok, which has likely aided some yield retracement (albeit very modest with Friday's yield losses).

- On the data front, the Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA's 2-3% target band and may rise in coming months.

- In a week of second tier data, the focus is likely to be on Tuesday’s June household spending data which will now replace retail sales, which had its last print last week. The Q2 chain volume measure is also out. Bloomberg consensus expects June consumption values to rise 0.8% m/m to be up 4.9% y/y after 4.2% in May. The ABS noted that discounting in the month had boosted June retail sales.

AUD: Asia Wrap - AUD/USD Finds Some Demand As Risk Stabilises In Asia

The AUD/USD has had a range of 0.6462 - 0.6484 in the Asia- Pac session, it is currently trading around 0.6483, +0.14%. US Yields collapsed in response to the NFP data which sparked a kneejerk response lower in the USD. This was also a very bad day for US stocks which finally look to be pulling back from elevated levels. The question for the AUD going forward is does the USD see sellers quickly return in response to the move in rates, or can the USD rise from the ashes and return as a safe haven. The AUD bounced nicely off the 0.6400 area but I suspect sellers again back towards 0.6500/50 initially as risk wobbles and the market wrestles about what to do with the USD.

- AUSTRALIAN DATA: MI Underlying Inflation Gauge Rises Signalling Possible Trough. The Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA’s 2-3% target band and may rise in coming months. The headline inflation gauge has less signal to it. Currently the RBA remains focussed on quarterly CPI data but a more complete monthly series will be released in November.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6465(AUD727m), 0.6450(AUD402m). Upcoming Close Strikes : 0.6600(AUD1.97b Aug 7), 0.6800(AUD1.72b Aug 7) - BBG

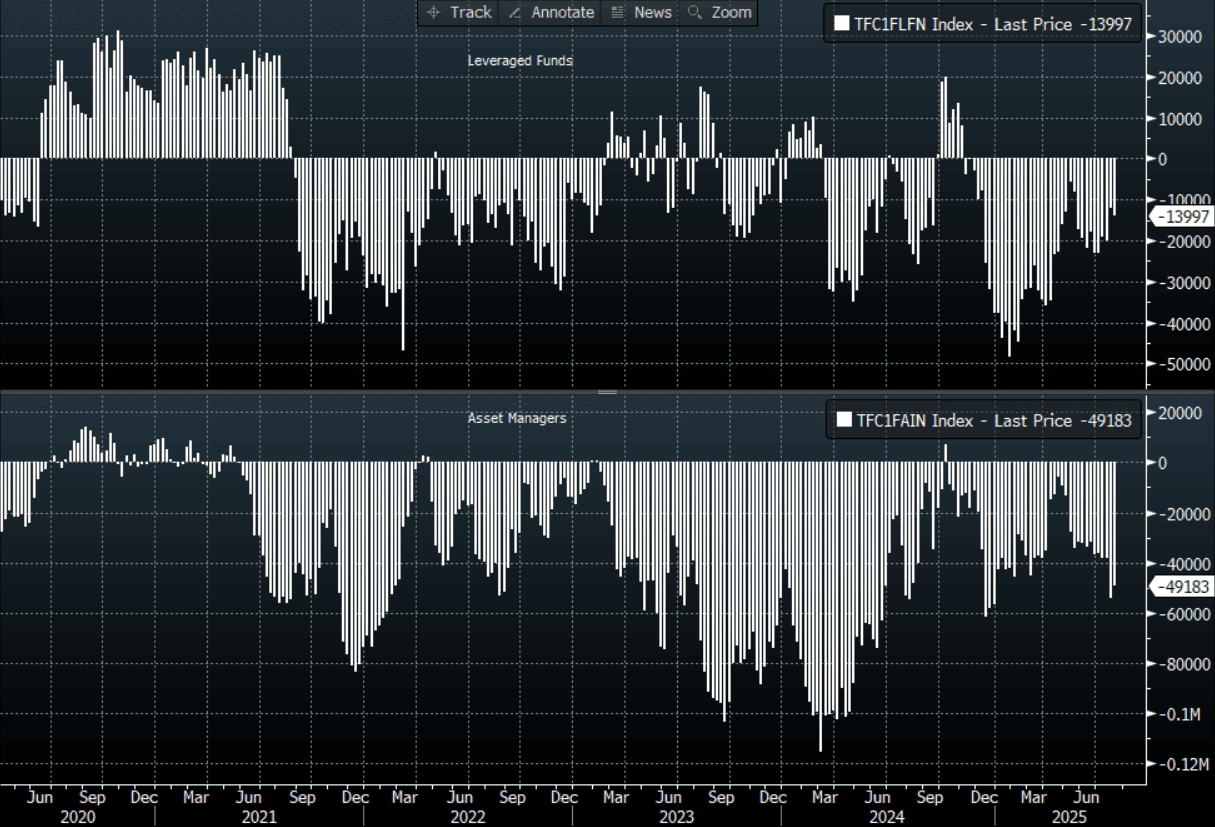

- CFTC Data shows Asset managers reduced their shorts slightly -49183(Last -53959), the Leveraged community added to their own shorts -13997(Last -12010).

- AUD/JPY - Asia-Pac range 95.13 - 95.82, Asia is trading around 95.70. The pair failed on multiple attempts above 97.00 and has moved swiftly back to test its first support around the 95.50 area. With risk having a huge reversal lower last week the headwinds for JPY crosses are growing and should risk remain under pressure I suspect bounces will initially be met with supply.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

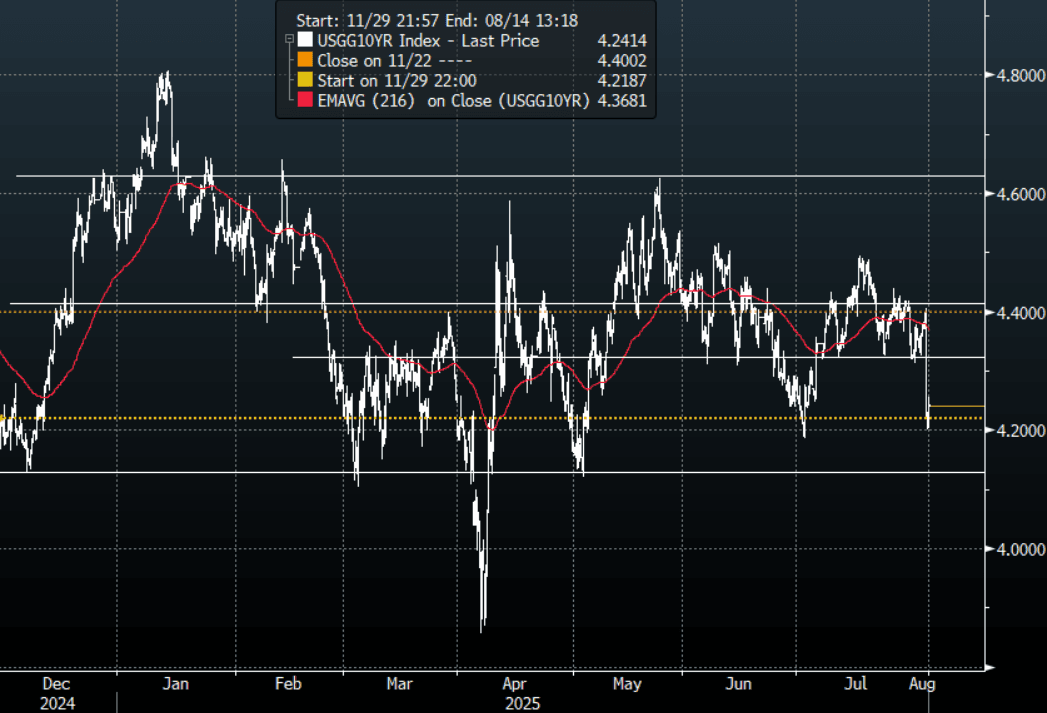

US TSYS: Asia Wrap - Yields Retrace Some Of Friday's Moves

The TYU5 range has been 112 to 112-12 during the Asia-Pacific session. It last changed hands at 112-03+, down 0-03 from the previous close.

- The US 2-year yield has bounced off Friday’s lows trading around 3.696%, up 0.01 from its close.

- The US 10-year yield has also bounced off Friday’s lows trading around 4.241%, up 0.03 from its close.

- (Bloomberg) -- “A block of 2,300 contracts in 10-year bond September futures traded at a price of 114-03 on CBOT. A total of 53,897 contracts traded so far in this session.” There were also multiple block trades executed in both the five-year and two-year contracts.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area. The move was even more aggressive in the 2-year which has rejected the move back towards 4% and now looks to target the pivotal 3.50% area.

- Wei Li(CIS BlackRock) on LinkedIn: “I don’t envy Powell, the Fed challenge is real:

- Slower growth - we had expected tariffs to slow US growth to about HALF its potential, and now it looks like the economy is already there. 3-month average payroll gains of just 35k is below our breakeven estimate of 60-80k, that accounts for demographics and softening immigration flows. Tariffs and trade are distorting other data such as gdp, but it is less the case with labour data/nfp.”

- “Persistent inflation pressure - average hourly earnings rose on the month, puzzlingly strong given weak job creation, although partly attributable to slower immigration crimping labour supply. Furthermore, tariffs are starting to feed through and could further push up goods prices.”

- CrossBorder Capital on X: “US Treasuries looking pretty stable despite the noise!? Term premia decoupling favorably from RoW. Zero evidence of loss of safe haven quality.”

- Data/Events: Factory Orders, Durable Goods

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P