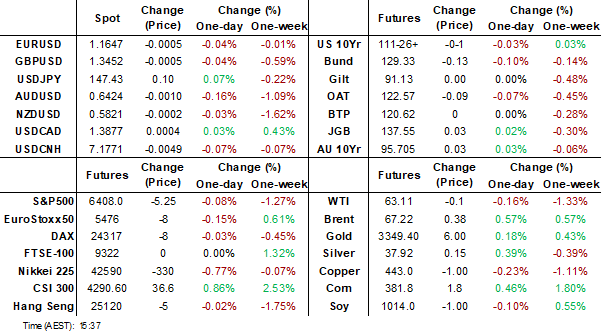

MNI EUROPEAN MARKETS ANALYSIS: August PMIs In Focus

- US Tsy yields are little changed as markets await Jackson Hole. Aggregate USD indices are up a touch, with the AUD down slightly but aggregate moves in this space have also been modest.

- Japan PMIs were mixed with manufacturing up but still sub 50.0. Weekly investment flows saw offshore investors continue to buy Japan stocks, a strong theme in recent months. In Australia, the S&P Global PMI is suggesting that growth picked up in Australia in Q3, while inflation expectations eased. In NZ, after five consecutive merchandise trade surpluses, NZ recorded a deficit in July of $578mn bringing the 12mth sum to $3.94bn down from $4.38bn.

- Later the Fed’s Bostic appears. US preliminary August S&P Global PMIs, August Philly Fed, July lead index, July existing home sales and jobless claims print. There are also European preliminary PMIs and UK July public sector net borrowing.

MARKETS

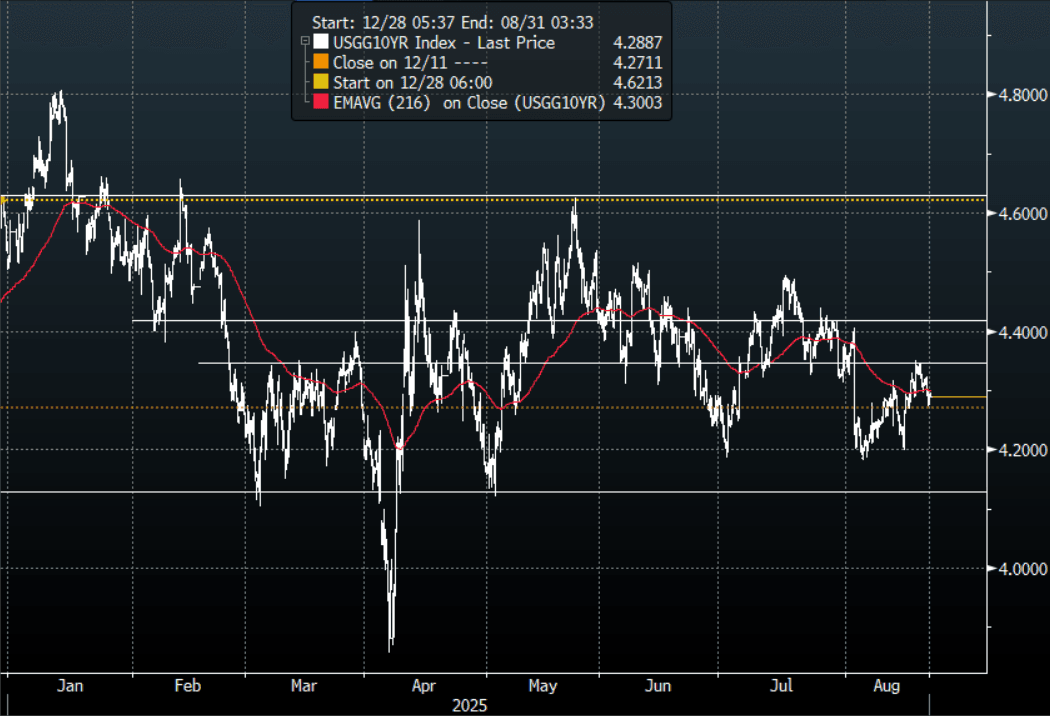

US TSYS: Quiet Session Looking Toward Jackson Hole

The TYU5 range has been 111-26 to 111-29 during the Asia-Pacific session. It last changed hands at 111-27+, unchanged from the previous close.

- The US 2-year yield is trading around 3.745%.

- The US 10-year yield is trading around 4.29%.

- 10-Year Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area found solid demand capping the move higher for now, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

- RenMac on X: “The July FOMC minutes show that it is really tough to push through a 50bp cut in September. Too many on the FOMC are concerned about upside inflation risks and even after a weak jobs number many see the slowdown as a benign labor supply story.”

- Daily Chartbook on X: "Foreigners are not too concerned about a debt crisis in the US. They continue to be significant buyers of US Treasury notes and bonds as well as US government agency bonds and domestic corporate bonds."@yardeni

- Financial Times on X: “Central banks are under growing pressure to keep interest rates artificially low to offset the cost of record government borrowing.”

- Data/Events: Initial Jobless Claims, Phil Fed Business Outlook, S&P US PMI’s, Leading Index, Existing HOme Sales

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Weaken In Afternoon Session, Natl CPI Tomorrow

JGB futures are little changed, +2 compared to the settlement levels.

- (Bloomberg) JGB futures are turning softer in the afternoon, as traders balk at the extra ¥650 billion of bonds sold today, which is helping to nudge 10-year yields to highest since 2008. Investors have been nibbling at long-term JGBs this week as yields approached cyclical highs, but it is the bond bears in the futures market who are calling the shots before BOJ Governor Ueda’s appearance at Jackson Hole.

- (Bloomberg) “Japan’s 20-year government bond yields climbed to fresh multi-decade highs, driven by persistent concerns over fiscal expansion and fading demand from key investors. Yields on bonds of various maturities rose, with the 10-year yield climbing to 1.61%, a level unseen since 2008, and 30-year notes rising to 3.18%, approaching the all-time peak of 3.2% seen in July.”

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are slightly mixed across benchmarks, with yields flat to 2bps higher and the curve steeper. The benchmark 10-year yield is 0.1bp lower at 1.61% versus the cycle high of 1.621% set yesterday.

- Swap rates are 1-2bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will see National CPI.

JAPAN DATA: August Manufacturing PMI Rises But Still Sub 50.0

Japan preliminary PMIs for August were mixed. Manufacturing improved to 49.9 from 48.9, but services eased to 52.7 from 53.6. This left the composite index slightly higher at 51.9 (versus 51.6 in July).

- The manufacturing index is up from March lows (just under 48.5), but hasn't yet re-captured the expansion point. The index has spent little time above 50.0 in recent years. In terms of the detail, output rose to 50.5 from 47.6, while new orders were also up on July levels.

- On the services side, we are just off recent highs, but remain comfortably in expansion territory. BBG notes the employment sub index did contract to 49.6 though, from 50 in July.

- The data is unlikely to shift broader thinking around Japan's macro backdrop, with officials generally characterizing it as a continued modest recovery.

JAPAN DATA: Local Investors Sell Overseas Bonds, Inflows Continued For Equities

Japan outbound flows were muted in the week ending August 15. We saw selling of offshore bonds. Since a surge in buying off offshore bonds from mid June to mid July, we have now seen net selling in this segment in 3 out of the past 4 weeks. To be sure, these recent cumulative outflows only modestly pare back the net buying seen earlier in 2025. Since mid June we have still seen local investors buy just over ¥5.5trln in overseas bonds (up to the end of last week). On the equity side, Japan investors bought overseas stocks for the first time since the end of July.

- In terms of inflows into Japan assets, the standout was the purchases of local equities. This continued the winning streak of inflows into this space back to end June, while it was also the largest weekly inflow since early April this year. The focus will be on whether these trends are sustained given the recent equity market correction, led by the tech side. Japan markets are only modestly off recent record highs.

- Offshore investors also purchased local bonds, albeit in more modest size.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Aug 15 | Prior Week |

| Foreign Buying Japan Stocks | 1161.7 | 495.5 |

| Foreign Buying Japan Bonds | 197.9 | 733.2 |

| Japan Buying Foreign Bonds | -313.6 | 254.7 |

| Japan Buying Foreign Stocks | 395.0 | -225.6 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Richer & Near Session Bests, Jun-54 Supply Tomorrow

ACGBs (YM +2.0 & XM +4.0) are stronger and close to the session’s bests.

- The S&P Global PMI is suggesting that growth picked up in Australia in Q3. The preliminary August composite index rose to 54.9 from 53.8 driven by improvements in both the manufacturing and services sectors. This is the fastest growth in activity since April 2022, before the RBA began its tightening cycle.

- In June, Melbourne Institute consumer inflation expectations jumped 1pp to 5%. They moderated to 4.7% in July and in August to 3.9%, the first print below 4% since March's 3.6%. Looking at the trend, the series has been moving sideways for around the last year.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 2-4bps richer with the AU-US 10-year yield differential at -3bps.

- The bills strip has twist-flattened, with pricing -1 to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$300mn of the 4.75% 21 June 2054 bond.

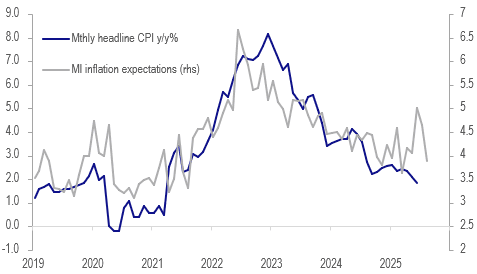

AUSTRALIA DATA: Inflation Expectations Back Below 4%

In June, Melbourne Institute consumer inflation expectations jumped 1pp to 5%. They moderated to 4.7% in July and in August to 3.9%, the first print below 4% since March’s 3.6%. Looking at the trend, the series has been moving sideways for around the last year. It is still too soon to say that inflation expectations are drifting down again with the next few months key in determining that. However, the August moderation in addition to S&P Global reporting an easing in the pace of output price inflation to just above the historical average are likely to reassure the RBA that inflation is sustainably within the target band.

Australia inflation %

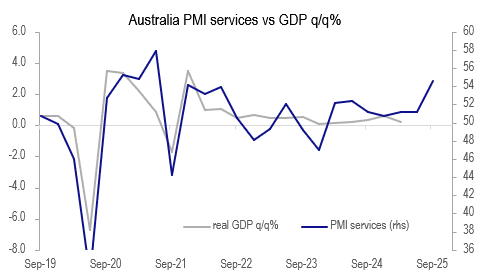

AUSTRALIA DATA: PMI Suggests H2 Pickup In Growth

The S&P Global PMI is suggesting that growth picked up in Australia in Q3. The preliminary August composite index rose to 54.9 from 53.8 driven by improvements in both the manufacturing and services sectors as well as higher new orders, including external, and increased hiring to fill them. This is the fastest growth in activity since April 2022, before the RBA began its tightening cycle. The PMI suggests that while Q2 growth could again be lacklustre there was probably an improvement in H2.

Australia GDP q/q% vs S&P Global services PMI

- New export orders in August rose at their fastest pace in six months with increased demand from Europe, APAC and the US.

- While costs continued to rise driven by raw materials, labour costs and shipping, it was lower than in July for both services and manufacturing. This likely drove a slowdown in the pace of output price inflation to just above the historical average.

- Businesses are also more upbeat about the outlook with business confidence rising which has likely been helped by lower interest rates and a settling in global trade developments.

- The services S&P Global PMI rose to 55.1 from 54.1. Hiring increased at its fastest rate since April 2023.

- The manufacturing PMI increased to 52.9 from 51.3. Despite the pickup in new work, firms cut staff slightly.

Australia S&P Global PMIs

Source: MNI - Market News/ABS/Bloomberg Finance L.P.

BONDS: NZGBS: Extends Post-RBNZ Rally Into The Close

NZGBs closed richer, extending yesterday’s strong post-RBNZ decision by 2-4bps.

- Today’s weekly supply saw solid demand, with cover ratios ranging from 3.11x (May-35) to 4.00x (May-30).

- The NZ-US 10-year yield differential closed 3bps tighter at 6bps, the tightest since February.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally. Today’s US Data/Events: Initial Jobless Claims, Phil Fed Business Outlook, S&P US PMIs, Leading Index and Existing Home Sales.

- Swap rates closed 1-4bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 17-26bps softer across meetings versus yesterday’s pre-RBNZ Policy Decision levels. The market had priced 22bps of yesterday’s 25bp cut going into the decision. 19bps of easing is priced for October, with a cumulative 37bps by November 2025 versus 12bps before the. decision.

- Tomorrow, the local calendar will see Trade Balance data.

NEW ZEALAND: First Trade Deficit Since January

After five consecutive merchandise trade surpluses, NZ recorded a deficit in July of $578mn bringing the 12mth sum to $3.94bn down from $4.38bn. Export growth remains strong, which has been a bright spot in a soft economy.

- Goods exports rose 10% y/y in July with dairy products rising 17% y/y. The sector was helped by higher prices but also increased volumes for milk powder and butter. Beef exports rose 17% y/y with strong increases to the US and Canada but declining to China.

- Shipments to China, NZ’s largest destination, were up 7.1% y/y, to Australia +4.7% y/y and US +7.7% y/y, which slowed from 21.8% y/y in April.

- Goods imports rose 2.6% y/y. Growth has been volatile but the 3-month average is showing a gradual trend higher supported by strong imports of machinery & equipment, vehicles and aircraft.

NZ merchandise trade balance 12-mth sum NZ$bn

FOREX: Asia FX Wrap - The USD Is Steady Heading Into Jackson Hole

The BBDXY has had a range of 1206.68 - 1207.81 in the Asia-Pac session, it is currently trading around 1207, +0.05%. The USD consolidated its recent gains overnight as we await Powell's speech at Jackson Hole. Depending on the contents of Powell's speech this could change very quickly but the BBDXY looks to be putting in a third higher low which would be a worrying sign to the bears that we could be putting in a short-term base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1641 - 1.1656, Asia is currently trading 1.1645. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to extend too far as the market awaits Powell's speech.

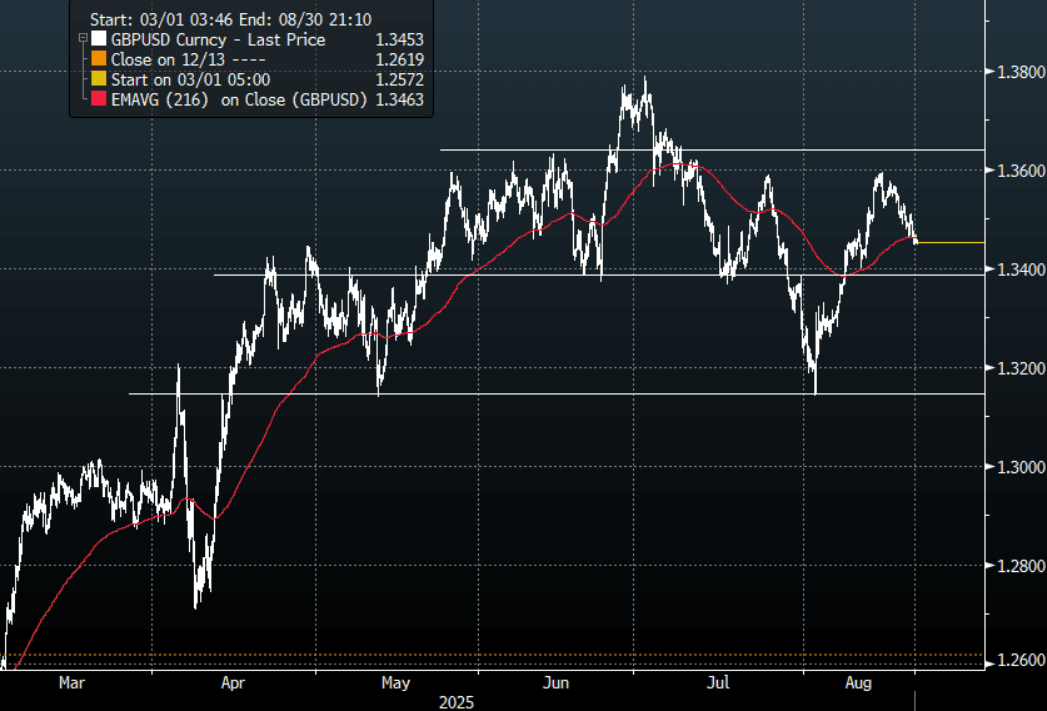

- GBP/USD - Asian range 1.3448 - 1.3467, Asia is currently dealing around 1.3455. Having broken back above its pivot look for dips to again be supported, with risk retracing the pair is probing its first support seen towards 1.3400.

- USD/CNH - Asian range 7.1716-7.1842, the USD/CNY fix printed 7.1287, Asia is currently dealing around 7.1760. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.01%, Gold $3338, US 10-Year 4.29%, BBDXY 1207, Crude Oil $63.07

- Data/Events : EZ HCOB PMI’s/Construction Output/Consumer confidence, Germany HCOB PMI’s, France HCOB PMI’s

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

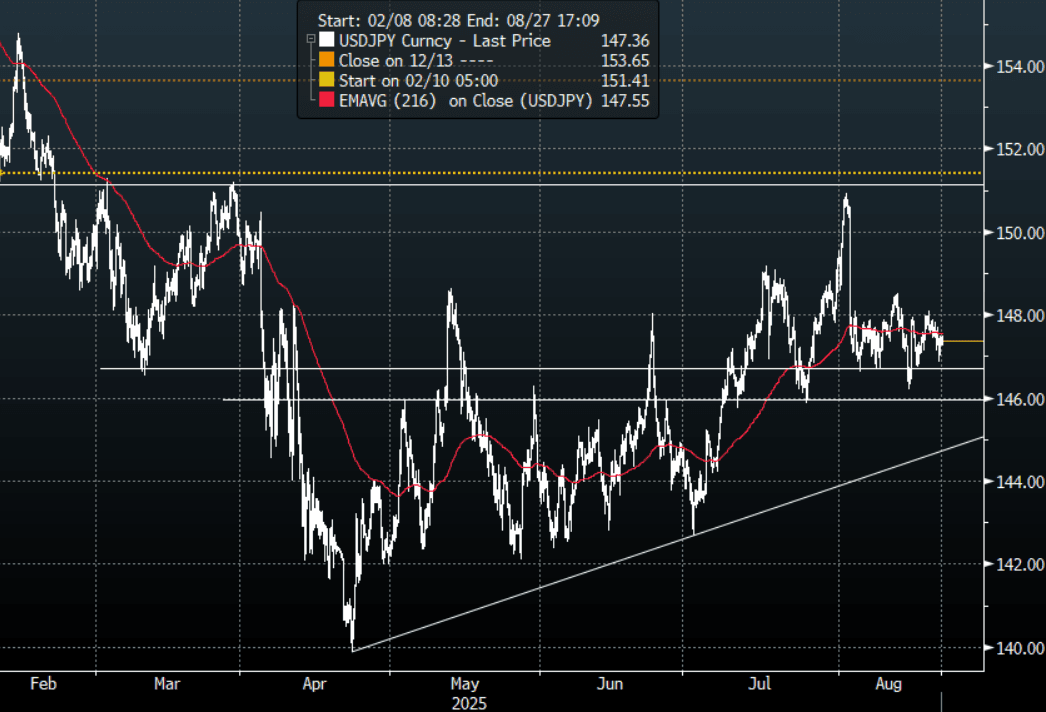

JPY: Asia Wrap - USD/JPY Holds Above 147.00 Ahead Of Jackson Hole

The Asia-Pac USD/JPY range has been 147.26-147.51, Asia is currently trading around 147.40, +0.05%.USD/JPY again found solid demand on a 146 handle overnight as US stocks recovered from a weak opening. Price continues to hold above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. While this plays out it looks to be more range trading within the wider 146.00-151.00 range.

- CFTC Data shows leveraged funds have bought this dip in USD/JPY betting the support remains intact. Powell's speech at Jackson hole will have a say in whether it continues to hold or not.

- Japan Data: August Manufacturing PMI Rises But Still Sub 50.0 : Japan preliminary PMIs for August were mixed. Manufacturing improved to 49.9 from 48.9, but services eased to 52.7 from 53.6. This left the composite index slightly higher at 51.9 (versus 51.6 in July).

- (Bloomberg) - Japan 20-Year Government Bond Yield Rises to Highest Since 1999: Yields on Japan’s super-long government bonds climbed to multi-decade highs, driven by persistent concerns over fiscal expansion and fading demand from key investors.

- "LDP REPORT ON ELECTION TO BE DELAYED TO EARLY SEPT.: TV ASAHI" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.80($1.35b), 150.00($1.06b).Upcoming Close Strikes : 147.90($1.54b Aug 22), 143.00($1b Aug 25), - BBG.

- CFTC data shows last week asset managers maintained their JPY longs +60866( Last +60532), leveraged funds used the dip to add to their newly built short JPY position -41257(Last -29308).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Drifts Lower

The AUD/USD has had a range of 0.6419 - 0.6437 in the Asia- Pac session, it is currently trading around 0.6425, -0.15%. The AUD has continued to trade heavy in our session. The AUD broke below its support just below 0.6500 earlier in the week and looks likely to continue to trade heavy into Powell’s speech. Pivotal support is back towards 0.6300/50 which has been the bottom in its recent multi-month range of 0.6350-0.6650.

- AU Data: Inflation Expectations Back Below 4%In June, Melbourne Institute consumer inflation expectations jumped 1pp to 5%. They moderated to 4.7% in July and in August to 3.9%, the first print below 4% since March's 3.6%. Looking at the trend, the series has been moving sideways for around the last year. It is still too soon to say that inflation expectations are drifting down again with the next few months key in determining that.

- PMI Suggests H2 Pickup In Growth: The S&P Global PMI is suggesting that growth picked up in Australia in Q3. The preliminary August composite index rose to 54.9 from 53.8 driven by improvements in both the manufacturing and services sectors as well as higher new orders, including external, and increased hiring to fill them. This is the fastest growth in activity since April 2022, before the RBA began its tightening cycle. The PMI suggests that while Q2 growth could again be lacklustre there was probably an improvement in H2

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD514m), 0.6600(AUD1.34b). Upcoming Close Strikes : 0.6525(AUD350m Aug 22), 0.6510(AUD520m Aug 25), 0.6400(AUD346m Aug 25) - BBG

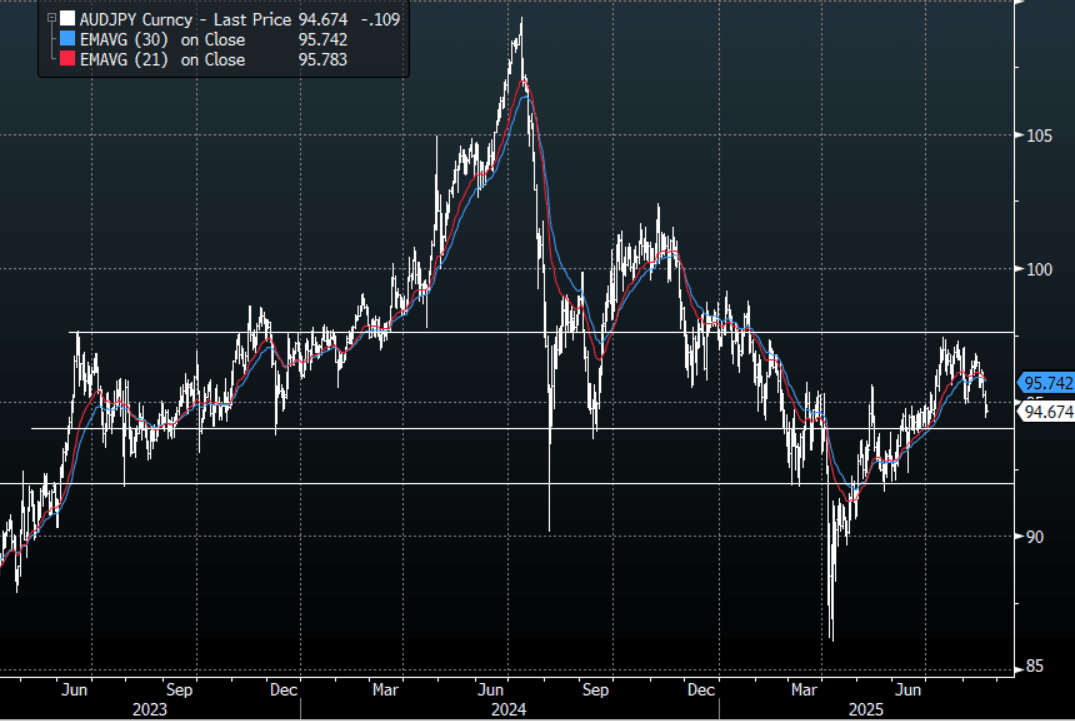

- AUD/JPY - Asia-Pac range 94.59 - 94.91, Asia is trading around 94.65. The pair extended its move lower overnight after breaking below 95.50. Although the price is still in the 94.00-97.50 range the multiple failures towards 97.00 looks like a rounded top and with risk looking vulnerable a test of the lower end of the range looks possible. A sustained break below the 94.00/94.50 area is needed to potentially begin a trend lower again.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

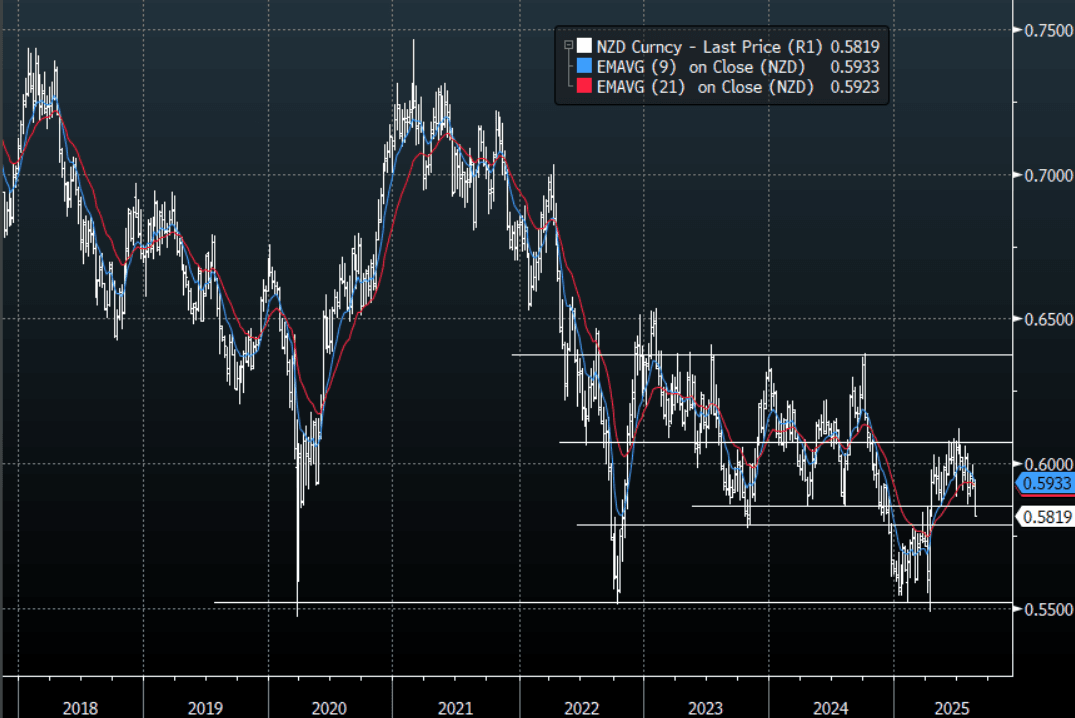

NZD: Asia Wrap - NZD/USD Trading Heavy Testing 0.5800 Support

The NZD/USD had a range of 0.5815 - 0.5833 in the Asia-Pac session, going into the London open trading around 0.5815, -0.12%. A dovish RBNZ that contemplated a cut of 50bps saw NZD/USD break lower yesterday and is now probing some pivotal support in the 0.5800 area. Some of the crosses have broken some key levels AUD/NZD above 1.1000 & NZD/JPY below 86.50, pointing to further NZD weakness ahead. US Futures have had a muted range today, E-minis +0.01%, NQU5 +0.10%.

- (Bloomberg) - RBNZ’s Hawkesby Says Commodity Price Gains Support Economy: Elevated food commodity prices have insulated the New Zealand economy from the negative shock the world is facing, RBNZ Governor Christian Hawkesby said in interview broadcast by CNBC. “It’s one of the things that gives us confidence that with low interest rates and high commodity prices, you’ve got the ingredients there in New Zealand for an economic recovery over the second half of this year and into next”

- "FONTERRA LIFTS FY25 FARMGATE MILK PRICE TO NZ$10.15/KG, SEES FY26 FARMGATE MILK PRICE NZ$9-11/KG" - BBG

- First Trade Deficit Since January: After five consecutive merchandise trade surpluses, NZ recorded a deficit in July of $578mn bringing the 12mth sum to $3.94bn down from $4.38bn. Export growth remains strong, which has been a bright spot in a soft economy.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5980(NZD660m). Upcoming Close Strikes : none - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short adding slightly in the NZD -3679(Last -1811), the Leveraged community though reduced their own shorts slightly -4190(Last -6778).

- AUD/NZD range for the session has been 1.1029 - 1.1056, currently trading 1.1035. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

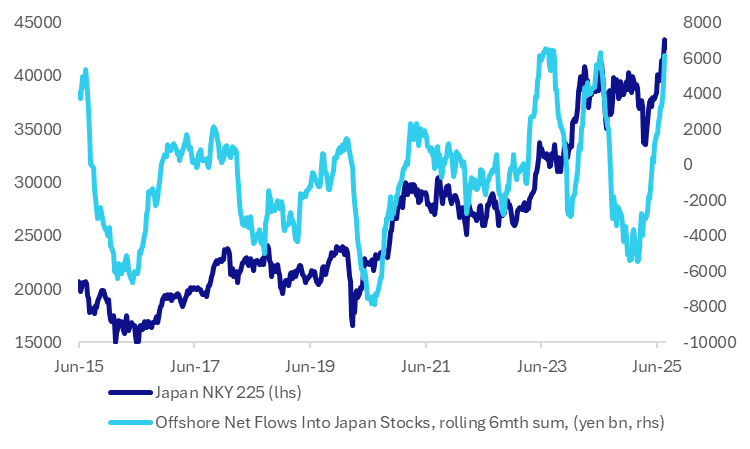

ASIA STOCKS: Japan Softens Further, Other Markets Higher

Outside of further Japan equity market weakness, most Asia Pac equity indices are firmer in the first part of Thursday trade. US equity futures are a touch higher, as are EU futures. In Wednesday cash trade, US markets lost further ground, but both the SPX and the Nasdaq finished well above intra-session lows from the session.

- In Japan, the Topix is off around 0.50%, while the NKY is down slightly more (off 0.60%). Both markets are only marginally off recent record highs. Earlier data showed, up until the end of last week, continued inflows into local stocks from offshore investors. Indeed, since the start of April there has only one week of net selling of local equities out of the past 20 weeks.

- The chart below plots the rolling 6 mth sum of offshore inflows into Japan stocks and the NKY 225 index. We are back close to cycle highs on this flow metric. Loss of momentum in this space could impact Japan equity trends if history is a guide.

- Elsewhere, Taiwan's Taiex has recouped some of yesterday's losses, the index up a little over 1% (after dipping nearly 3% yesterday, amidst nearly $2.4bn in offshore selling). South Korea's Kospi is also tracking up, last up around 0.90%.

- Hong Kong's HSI is down a little, but the CSI 300 in China continues to rally, up a further 0.70% putting the index around the 4300 level. The index continues to close in on intra-session highs from Oct last year.

- Australia's ASX 200 is up firmly, +0.85% to fresh record highs, amidst a broad based rally. NZ markets also continued to rise, up a further 1.1%, after yesterday's strong gains post the dovish RBNZ cut.

- In South East Asia, outside of modest losses for Thailand and Indonesia, markets are modestly higher. The Philippines is out today.

Fig 1: Offshore Inflows Have Surged Into Japan Stocks

Source: Bloomberg Finance L.P./MNI

ASIA STOCKS: Taiwan Outflows Surge Amid Tech Equity Weakness

Large offshore selling pressures for Taiwan equities yesterday were a standout. The near $2.4bn in net selling was the largest single daily outflow since early September last year. The Taiex index fell by nearly 3% yesterday, unwinding a good chuck of the August to date rally. Broader tech concerns continued in Wednesday US trade, with the SOX down a further 0.72%. Our US team noted: Information Technology sector stocks led decliners on the day after Forbes reported the Trump administration "may seek equity in any such firms awarded federal grants under the Biden-era CHIPS Act. Lutnick said the government want to acquire an equity stake in Intel in exchange for grants earmarked under the CHIPS Act." This comes on top of recent concerns around whether the strong AI/chip demand pace can be sustained.

- South Korea also saw outflow pressures yesterday, albeit at a more moderate pace compared to Taiwan. Still, South Korea has seen nearly $900mn in outflows over the past 5 day trading days.

- For India, trends were flat in Tuesday trade from an equity flow standpoint. The headwinds from a 5 day sum standpoint have reduced though.

- In South East Asia, Indonesia inflows remained positive, but negative trends were seen evident for Thailand, while Malaysia outflow momentum picked up.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -187 | -892 | -5333 |

| Taiwan (USDmn) | -2378 | -2944 | 1668 |

| India (USDmn)* | -1 | -282 | -12722 |

| Indonesia (USDmn) | 47 | 232 | -3233 |

| Thailand (USDmn) | -17 | -84 | -1986 |

| Malaysia (USDmn) | -50 | -168 | -3408 |

| Philippines (USDmn) | 3 | -21 | -617 |

| Total (USDmn) | -2583 | -4159 | -25631 |

| * Data Up To Aug 19 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Higher Again Today On Large US Crude Drawdown

Oil prices have continued trending higher today consolidating Wednesday’s rally which was driven by a larger-than-expected US crude drawdown reported by the EIA. WTI is up 0.6% to $63.07/bbl following a peak of $63.19, while Brent is 0.4% higher at $67.12 after rising to $67.29. Crude has trended lower through most of August. The USD index is slightly higher.

- With the IEA forecasting a record oil surplus in 2026, attention is firmly on supply and demand information. For now the US market is looking robust with high refining utilisation and falling inventories.

- The EIA reported a significant crude inventory drawdown of 6.01mn barrels last week. Gasoline stocks fell 2.72mn, fifth consecutive decline, while distillate rose 2.34mn. The refining utilisation rate rose 0.2pp to 96.6%, 4.3pp higher than the same time last year, suggesting demand is robust.

- Later the Fed’s Bostic appears. US preliminary August S&P Global PMIs, August Philly Fed, July lead index, July existing home sales and jobless claims print. There are also European preliminary PMIs and UK July public sector net borrowing.

Gold Lower, Waiting For Fed Powell’s Speech Friday

After rising a percent on Wednesday in reaction to concerns over Fed independence, gold prices are 0.2% lower at $3340.8/oz, close to the intraday low, during today’s APAC trading. The slightly stronger US dollar (USD BBDXY +0.1) will be adding pressure, while yields are little changed. Bullion rallied on Wednesday after US President Trump called for Fed Governor Cook to resign. She was a Biden appointee.

- Currently there is around an 80% chance of a Fed cut at its next meeting on 17 September. Markets are waiting for Fed Chair Powell’s Jackson Hole speech on Friday to read his thinking regarding the timing of a resumption of easing. The July minutes showed that inflation worries persist.

- Fitch Solutions is forecasting gold to move between $3200-3600/oz over the rest of the year, according to Bloomberg.

- Silver is little changed at $37.928 after falling to $37.826 and then reaching $37.974.

- Equities are mixed with the Nikkei down 0.6%, CSI 300 up 0.7% and the S&P e-mini flat. Oil prices have continued higher with WTI +0.5% to $63.03/bbl. Copper is 0.2% lower.

- Later the Fed’s Bostic appears. US preliminary August S&P Global PMIs, August Philly Fed, July lead index, July existing home sales and jobless claims print. There are also European preliminary PMIs and UK July public sector net borrowing.

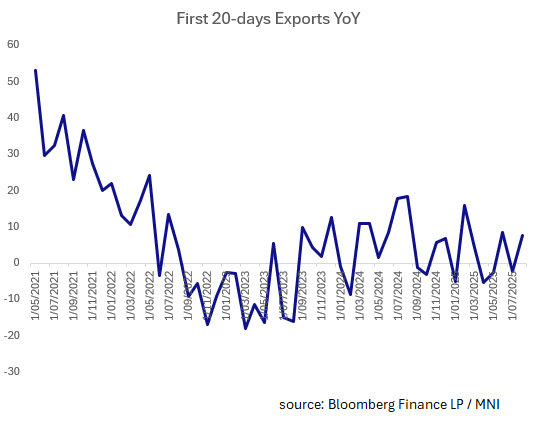

SOUTH KOREA: Early August Exports Up +7.6% YoY

- South Korea First 20 Days of August Exports Rose +7.6% YoY.

- This compares to a contraction of -2.2% in June.

- Early exports have contracted four out of the eighth months of the year to date and continue to be highly volatile as the threat of tariffs have interrupted supply patterns.

- The first 20 days in August of imports were up +0.4% YoY.

- The result is a trade surplus of US$833m.

- First 20 days chip exports rose +29.5% YoY

- First 20 days exports to China rose +2.7% YoY

First 20 days exports to US fell -2.7% YoY.

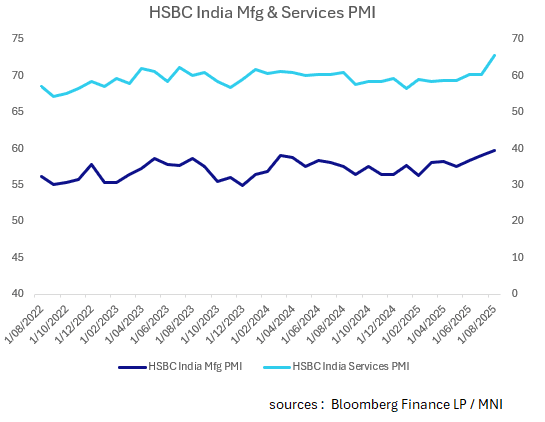

INDIA: PMIs Ignore US Tariff Threat

- HSBC and S&P Global India’s August flash manufacturing purchasing managers’ index index rose to 59.8 from 59.1 in July.

- This is the highest reading since the beginning of 2008 and seemingly ignoring the US tariff threats.

- Output rose to +64.2 from +62.5 and New Orders were higher relative to last month and their highest since late 2020.

- The August services PMI expanded strongly also in July up +65.6 from +60.5 for the highest reading since the series began.

- The employment component rose to +52.7 from +561.4 and prices charged were at their highest since June 2012.

CHINA: Country Wrap: Local Papers Predicting Rate Cuts

- China is likely to lower their benchmark lending rates this year to bolster economic growth, industry analysts interviewed by domestic financial newspapers including Securities Daily predict. (source Securities Daily)

- China's private companies are spearheading breakthrough innovations across various key sectors, supported by favorable government policies that encourage entrepreneurship and unleash market vitality in technological advancement. The latest data shows that the private sector has emerged as a key driving force behind China's technological development, with private firms accounting for over 92 percent of the country's high-tech companies since the beginning of the 14th Five-Year Plan period (2021-2025), according to the National Development and Reform Commission (NDRC). (source Xinhua)

- An offshore onshore divide today with the Hang Seng down -0.13%, CSI 300 up +0.66%, Shanghai Comp up +0.38% and Shenzhen Comp up +0.25%.

- Yuan Reference Rate at 7.1287 Per USD; Estimate 7.1773

- The CGB 10yr is -1bp for the day at 1.77% yet remains +3bps higher for the week.

SOUTH KOREA: Country Wrap: Korean Cos to Invest in US

- South Korea is set to unveil about $150 billion in US investment plans by private companies during a summit between President Lee Jae Myung and US President Donald Trump, the Hankyoreh newspaper reported Thursday. The pledge is likely to include both ongoing and future projects and will be separate from the $350 billion South Korea agreed to invest in the US as part of a trade agreement struck last month. While the $150 billion package will be highlighted at the summit, officials don’t expect further discussion of the $350 billion investment fund, which was a centerpiece of last month’s trade agreement, the newspaper said, citing unidentified government officials. The trade agreement between the two countries reached in July capped US tariffs on imports of Korean goods at 15%, one of the most favorable rates. Lee is set to meet Trump on Aug. 25 (source BBG)

- South Korea to roll out a 45.8t won support package this year to bolster supply chain resilience, combining low-interest financing and public-private funds to target at key industries such as batteries, semiconductors and critical minerals, according to a government statement. Govt to provide a total of 45.8t won in low-interest policy financing, which is composed of 10t won from the Supply Chain Stabilization Fund, 13.3t won from Export-Import Bank of Korea, 18t won from Korea Development Bank and 4.5t won from Industrial Bank of Korea. Additionally, 2 public-private investment vehicles will be launched: a 1.8t won fund, focusing on leading firms, and a 600b won fund aimed at SMEs and mid-sized companies in materials, parts and equipment. The measures will prioritize sectors deemed vital to economic security, including batteries, chips, critical minerals, energy, pharmaceuticals and biotech, as well as logistics infrastructure. (source BBG)

- The KOSPI snapped three days of losses to bounce back +0.48% today.

- The Won is losing ground by -0.15% to 1,398.78 with the move taking it through the 200-day EMA .

- Bonds are modestly better today with the 10yr 0.5bps lower at 2.86%

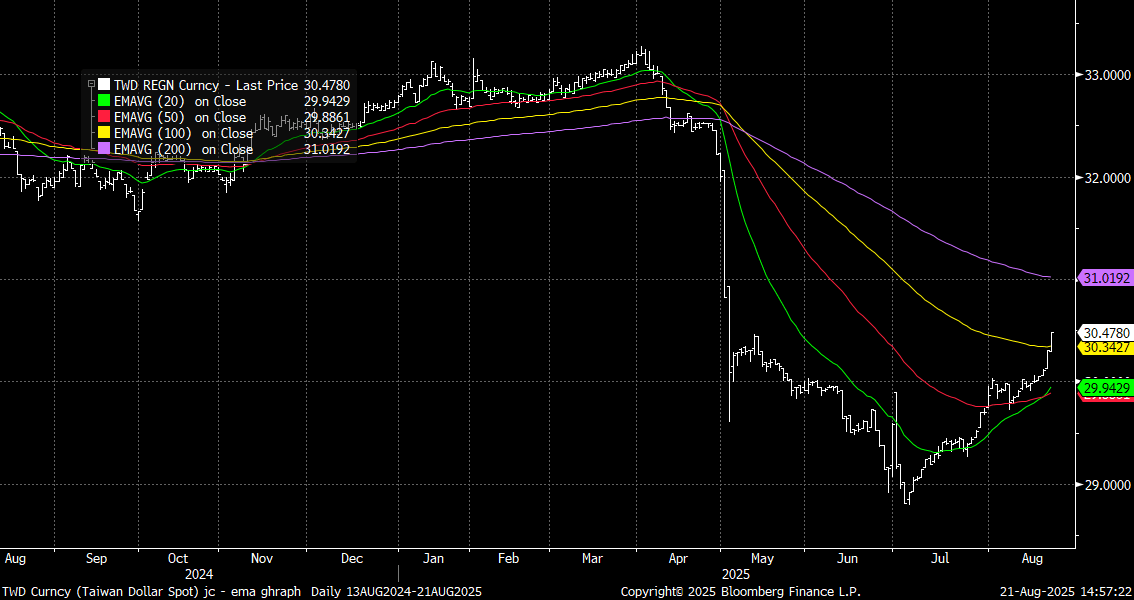

ASIA FX: TWD Weakness Continues, USD/HKD Holding Above Mid Point Of Peg Band

In North East Asia FX, the standout so far today has further TWD weakness. USD/TWD has risen into the 30.45/50 region, fresh highs back to May of this year. There has been little movement elsewhere in the region.

- For USD/TWD we have now cleared all key EMA resistance, except the 200-day, see the chart below. Further TWD weakness comes today, despite a rebound in onshore equities. The Taiex is up around 1.35% in latest dealings, after falling nearly 3% yesterday. Fallout from yesterday's nearly $2.4bn in offshore equity outflows may be a factor weighing on TWD for today as well. Yesterday's data for export orders also suggests headline export growth may moderate in H2.

- For USD/CNH, we saw a fresh low for the USD/CNY fixing back to Nov last year. Onshore USD/CNY spot opened lower, but found support under 7.1700. USD/CNH got to lows of 7.1716, but sits slightly higher now. Spot CNY looks to be lagging the stronger fixing outcomes, but some offset may be coming from mainland capital outflows, with inflows into Hong Kong equities highlighted of late.

- Spot USD/KRW has tracked recent ranges. We were last close to 1399. We haven't tested above 1400 in this most recent run higher.

- Spot USD/HKD sits at 7.8090, stabilizing after the recent move under the middle of the peg band (sub 7.8000). HKD T/N pts are drifting wider, last beyond -10pts, which could encourage re-engagement on long USD/HKD carry trades.

Fig 1: USD/TWD Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

ASIA FX: Little Movement In SEA FX, IDR Not Impacted By BI Cut

In South East Asia FX, aggregate FX moves have proven to be very modest so far in Thursday trade. USD/IDR sits near 16275/80, little changed for the session. Fallout from yesterday's surprise BI cut has been non-existent for FX markets so far. US monetary policy developments are likely to hold larger sway, with Friday's speech at Jackson Hole by Fed Chair Powell to be watched closely. Indonesian equities sit slightly weaker, with the JCI unable to maintain the recent test above 8000 (last near 7900). The country's Q2 current account deficit printed slightly wider than forecast (just over -$3bn, forecasts were at -$2.825bn).

- Elsewhere, USD/THB sits just off recent highs, last at 32.56, little changed for the session.

- USD/MYR is down slightly, last close to 4.2220. We have found selling interest above 4.2300 in recent sessions, which also marks the 20-day EMA resistance point.

- USD/INR is testing sub 87.00 again in the first part of Thursday trade, with August lows marked around 86.93. The 50-day EMA is further south around 86.68.

- Philippines markets are out today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 21/08/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/08/2025 | 0600/0800 | Q2 GDP | ||

| 21/08/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 21/08/2025 | 0900/1100 | ** | Construction Production | |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 21/08/2025 | 1400/1000 | *** | NAR existing home sales | |

| 21/08/2025 | 1400/1000 | * | Services Revenues | |

| 21/08/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 21/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 21/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 21/08/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 30 Year Bond | |

| 22/08/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 22/08/2025 | 2330/0830 | *** | CPI | |

| 22/08/2025 | 0600/0800 | ** | Unemployment | |

| 22/08/2025 | 0600/0800 | *** | GDP (f) | |

| 22/08/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/08/2025 | 0900/1100 | Q2 Negotiated Wage Growth | ||

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1230/0830 | ** | Retail Trade |