OIL: Crude Higher Again Today On Large US Crude Drawdown

Oil prices have continued trending higher today consolidating Wednesday’s rally which was driven by a larger-than-expected US crude drawdown reported by the EIA. WTI is up 0.6% to $63.07/bbl following a peak of $63.19, while Brent is 0.4% higher at $67.12 after rising to $67.29. Crude has trended lower through most of August. The USD index is slightly higher.

- With the IEA forecasting a record oil surplus in 2026, attention is firmly on supply and demand information. For now the US market is looking robust with high refining utilisation and falling inventories.

- The EIA reported a significant crude inventory drawdown of 6.01mn barrels last week. Gasoline stocks fell 2.72mn, fifth consecutive decline, while distillate rose 2.34mn. The refining utilisation rate rose 0.2pp to 96.6%, 4.3pp higher than the same time last year, suggesting demand is robust.

- Later the Fed’s Bostic appears. US preliminary August S&P Global PMIs, August Philly Fed, July lead index, July existing home sales and jobless claims print. There are also European preliminary PMIs and UK July public sector net borrowing.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - USD Drifts Lower With US Yields

The BBDXY has had a range of 1200.18 - 1201.47 in the Asia-Pac session, it is currently trading around 1201, +0.06%. The USD again fell very easily overnight, aided by the move lower in US yields. The market is much more comfortable selling USD’s, while the BBDXY trades below 1220 rallies will continue to find supply. “Scott Bessent called for a review of the Fed’s decision to renovate its headquarters. The central bank should conduct an internal examination of its non-monetary policy operations given the “significant mission creep,” he posted on X.” - BBG

- EUR/USD - Asian range 1.1683 - 1.1696, Asia is currently trading 1.1690. The pair bounced off its first support around the 1.1600 area. The price still looks a little stretched in the short term and is vulnerable to any correction in the USD, first support around 1.1550/1600 then more importantly the 1.1450 area.

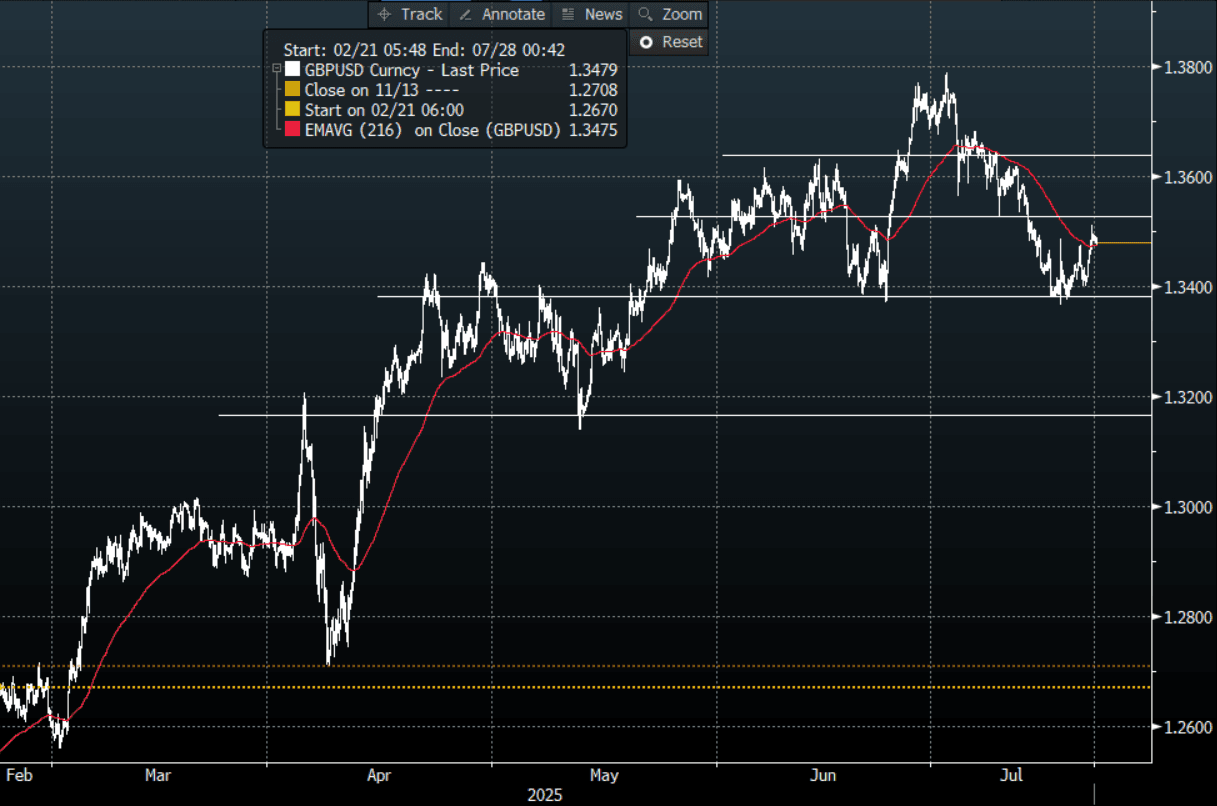

- GBP/USD - Asian range 1.3477 - 1.3494, Asia is currently dealing around 1.3480. The support around 1.3350/1.3400 has proved to be solid first up. Bounces back towards 1.3500/1.3550 should now see offers initially. A sustained move below 1.3350 would signal a deeper correction could be underway, until then market will continue to accumulate longs.

- USD/CNH - Asian range 7.1700 - 7.1749, the USD/CNY fix printed 7.1460, Asia is currently dealing around 7.1720. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.05%, Gold $3389, US 10-Year 4.368%, BBDXY 1201, Crude oil $66.51

- Data/Events : France Retail Sales

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Markets Mixed, Japan Return Weaker, HK and China Outperform

Asian equity markets are mixed in the first part of Tuesday trade. Further gains in Hong Kong and China markets are a positive, but other major indices are down at this stage, including returning Japan markets. US equity futures are down modestly, while EU futures are down by more, Euro Stoxx futures off by around 0.50%.

- Japan markets have returned from the long weekend and following the weekend election result where the LDP coalition lost its majority. At this stage, the Topix is down 0.40%, while the NKY 225 is off by around 0.55%. Onshore bond yields are mixed, slightly firmer at the back end of the curve. Tomorrow, we have a 40yr bond auction, which will test market sentiment post the election outcome. Japan and US officials also spoke for around 2 hours on Monday as the two-sides try to reach a trade deal before the Aug 1 deadline.

- South Korea and Taiwan markets are faltering. The Kospi is down 1.5%, last near 3160, once again struggling to hold above the 3200 level. The Taiex is down around 1%, with the index also moving off recent highs. Recent sessions have delivered less positive offshore impetus, particularly in the tech space.

- China and Hong Kong markets are up modestly, the HSI above 25000 and the CSI 300 around 4100. Onshore media noted the strong buying of local China market ETFs from the sovereign wealth fund through Q2 of this year.

- In Australia, the ASX 200 is down modestly, while in SEA most markets are weaker as well, but this follows strong gains recently, particularly for the likes of Thailand and Indonesia.

BONDS: NZGBS: Closed Richer After A Subdued Session Of Trading

NZGBs closed 1-2bps richer after a subdued session of trading.

- The NZ-US 10-year yield differential widened slightly to 19bps.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally.

- NZ posted a small merchandise trade surplus in June of $42mn, the fifth consecutive positive, after a downwardly revised $1082mn. There was a rise in the 12-month YTD deficit to $4.37bn from $3.93bn, but it is too early to say the trade improvement has stalled. Annual import growth rose sharply last month and was not as weak as exports in Q2.

- Swap rates closed flat to 4bps lower, with a flatter 2s10s curve.

- RBNZ dated OIS pricing closed little changed across meetings today but remains 5-9bps softer versus Monday’s pre-CPI levels. 21bps of easing is priced for August, with a cumulative 38bps by November 2025.

- Tomorrow, the local calendar will be empty.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.0% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 5.0% May-54 bond.