MNI EUROPEAN MARKETS ANALYSIS: All Eyes On US NFP Later

- Japan July labor earnings and household spending data were mixed. Headline earnings beat expectations, aided by bonus payments, while spending was positive but below forecasts. USD/JPY is down slightly, while JGB futures have risen to fresh multi week highs, following a strong offshore lead.

- US Tsy yields are down a touch, as markets await the US NFP print later. The USD is mostly weaker following modest gains on Thursday.

- China equities have rebounded from yesterday's losses. Thailand's parliament is voting for a new PM, with Anutin Charnvirakul expected to win.

MARKETS

US TSYS: Asia Wrap - Yields Drift Lower, Focus Turns To NFP

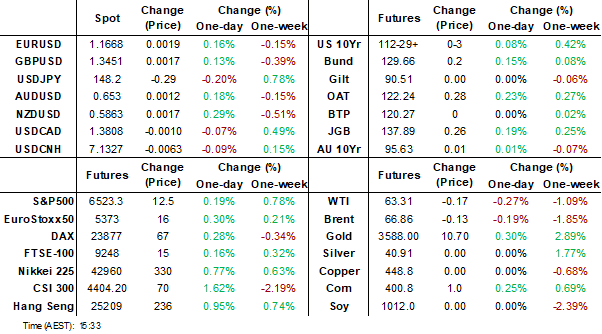

The TYZ5 range has been 112-28 to 112-31 during the Asia-Pacific session. It last changed hands at 112-31, up 0-04 from the previous close.

- The US 2-year yield has edged lower trading around 3.58%, down 0.01 from its close.

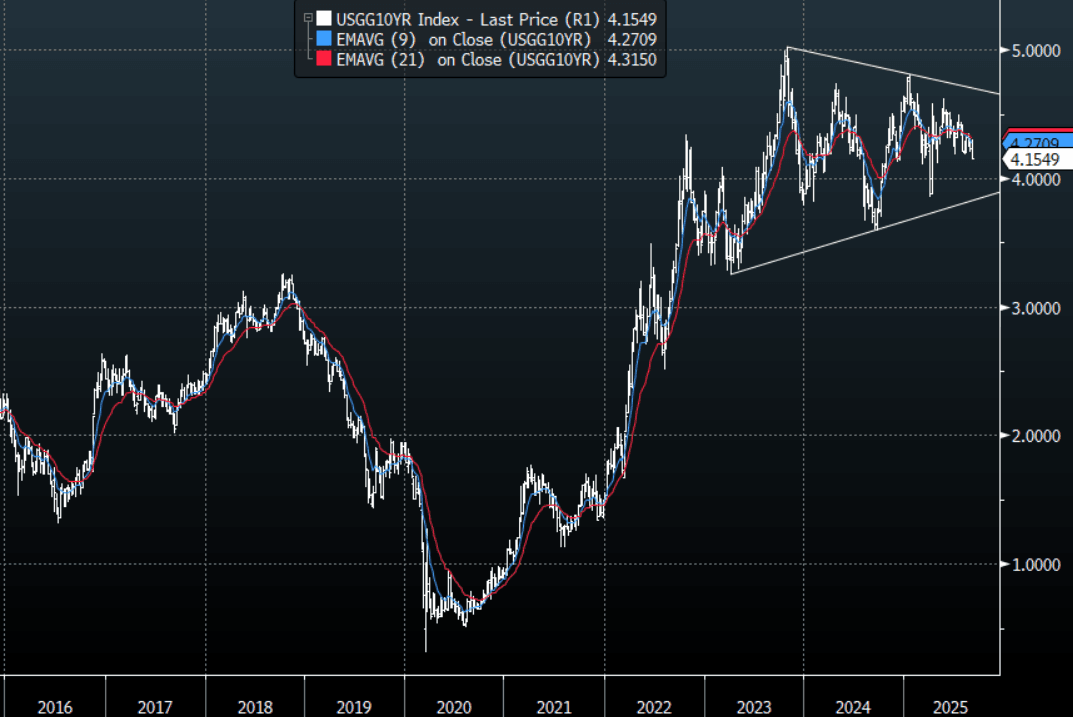

- The US 10-year yield has edged lower trading around 4.153%, down 0.01 from its close.

- 10-Year Yields broke below the 4.18/4.20% support area and goes into NFP with an eye on the next support around 4.10%. A sustained break below here would technically start to look pretty bullish with a target towards 3.80%. The bears will continue to point to supply and deficits as headwinds to this trade

- MNI BRIEF: Fed's Goolsbee - Not Yet Certain On Sept Rate Cut. Federal Reserve Bank of Chicago President Austan Goolsbee said Thursday he still has not yet made up his mind on whether to support cutting interest rates in September, and is still balancing out growing concern about the labor markets with lingering worries about persistent inflation

- The Kobeissi Letter on X: “This is absolutely insane: The BLS is set to revise US jobs numbers for the 12 months ending March 2025. According to Goldman Sachs, a DOWNWARD revision of up to -950,000 jobs is coming. This would be the biggest downward revision since 2010."

- @aahan_prometheus on X: “Reminder, as we go into jobs day tomorrow: Immigration is a drag on employment growth. I expect it to weigh on this print and the coming ones. Doesn't mean a recession, but it's not good.”

- Data/Events: NFP

Fig 1: 10-Year US Yield Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

US LABOR MARKET: MNI US Payrolls Preview: Slack Metrics Eyed With Risks Rising

We have published the MNI US Payrolls Preview, found here.

- Nonfarm payrolls growth is seen at 75k in August (sa) per the broad Bloomberg survey, after 73k in July.

- Revisions are going to be particular focus after last month’s huge downward revisions heavily altered recent trends, with non-health private payrolls growth at best stalling for the past three months, and dominated the market reaction.

- The median primary dealer analyst eyes 70k whilst the Bloomberg whisper currently sits at 83k but with the ADP report still to come after publication of this preview.

- Payrolls figures are increasingly being seen in light of a sharply reduced ‘breakeven’ pace on significant moderation in labor force growth. We generally see estimates between 50-100k/month.

- The unemployment rate is seen at 4.3% but with a sizeable skew towards a 4.2% - it doesn’t take much from 4.25% in July. This rate has moved within a 4-4.25% range since July 2024 and will be watched closely as gauge of labor market slack amid uncertainty over the signal sent by monthly payroll changes.

- An added complication worth considering is the soon-to-be-published preliminary benchmark revision due Tuesday (Sep 9), with expectations of a second year of heavy downward revisions.

- Whilst there has been a dovish build-up to this payrolls report, and with ADP and ISM services still to come before then, we currently assess that risks for market reaction are skewed towards a downside surprise.

JGBS: Futures Higher, 30yr Yield Falls Further, Q2 GDP Revisions Monday

JGB futures sit close to session highs (137.94), the Sep contract last 137.88, +.25 versus settlement levels. We have traded with a positive bias for much of the session, aided by carry over from global futures gains in Thursday trade (the US 10yr future broke higher amid signs of softer labor market outcomes). This, of course, comes ahead of the US NFP print later today.

- Today we saw better headline labor earnings data for July, but this was boosted by bonus payments in the month. Underlying wage trends didn't appear to shift much. Household spending figures for July were positive in y/y terms, but below market expectations.

- There have been numerous headlines around US-Japan trade deal agreement implementation, with the tariff rate set at 15% for most Japan products, while Japan is setting up an investment fund for $550bn of flows into the US. Details emerged that Japan could face higher tariff rates if investment funds for projects aren't provided.

- Via BBG: "Japanese Prime Minister Shigeru Ishiba reiterated his intention to stay on as leader after securing the lowering of US auto tariffs, dismissing the view that implementation of the trade deal with Washington might change his mind.” This comes ahead of a potential LDP leadership vote on Monday.

- Cash JGB yields are lower, led by the back end. The 30 and 40yr tenors were down around 3bps. The 10yr is off 2bps and is back under 1.58%. The 10yr swap rate is under 1.39%.

- Outside of the focus on local politics, next Monday delivers Q2 GDP revisions. Supply focus will be on the 5yr sale, held next Wednesday.

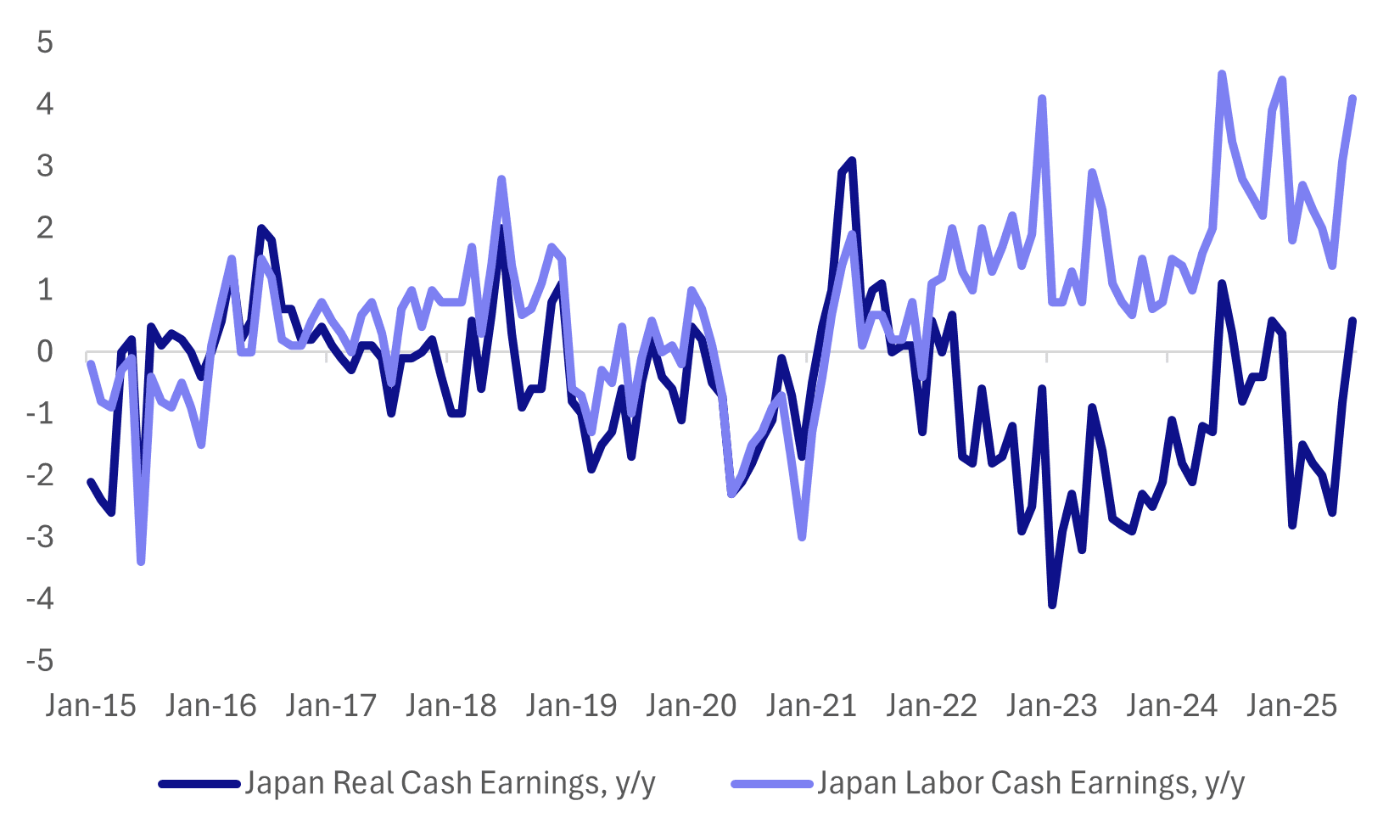

JAPAN DATA: July Cash Earnings Beat Estimates, Aided By Bonus Payments

Japan July labor earnings data was mostly better than forecast. The headline nominal read was +4.1%y/y, against a forecast rise of 3.0% and prior 3.1% (which was revised higher from the initial 2.5% estimate). In real terms, cash earnings rose 0.5%y/y, against a 0.6% forecast and -0.8% prior. The chart below plots nominal and real earnings in y/y terms.

- On a same sample base, cash earnings rose 2.9%, versus the 3.3% forecast (although June was revised up to 3.4% from 3.0%). Scheduled full time pay (same base) rose 2.4%y/y, versus 2.5% forecast and 2.3% prior.

- Bonus payments were up 7.9%y/y in July, versus 4.4% for June. This was the strongest rise since the 14.5% gain in March. This component can be volatile, so if we see a pull back in August it could weigh on the headline earnings outcomes.

- Scheduled full time pay, on a same sample base, painted a resilient picture with earnings up 2.4%y/y for the third straight month. We are off 2024 highs for this metric of 3%y/y, but are still well above historical averages.

- The authorities continue to see sustained positive real wages growth as a key policy goal. Today's data is a step in the right direction, but such trends have been elusive to maintain in recent years.

- From a BoJ standpoint, the result is welcome, but may not change near term thinking, given bonuses were a factor in the upside surprise. It is watching the tariff impact on corporate profitability and flow on effects closely. Household spending for July was also a touch below expectations.

Fig 1: Japan Nominal & Real Earnings Bounce In July

Source: Bloomberg Finance L.P./MNI

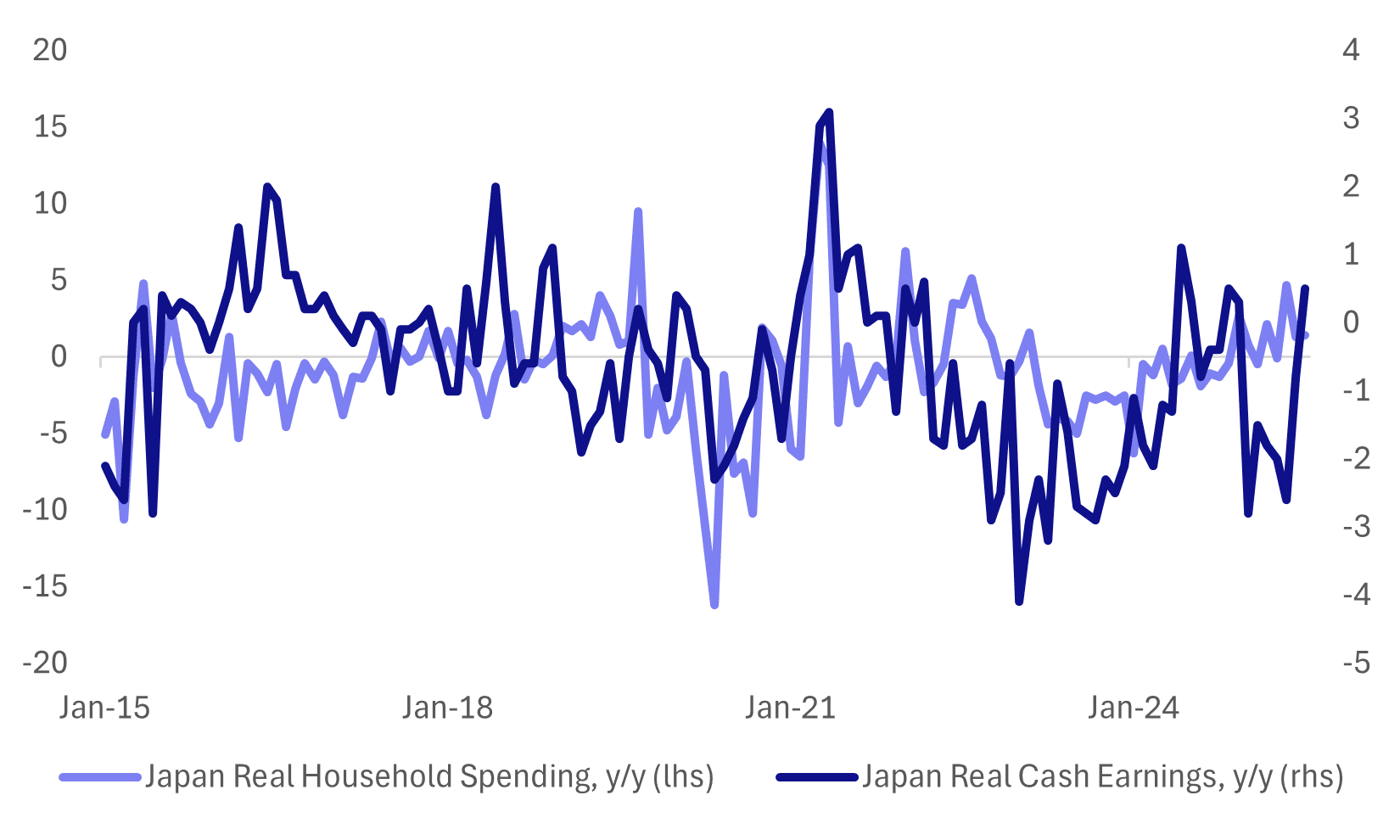

JAPAN DATA: Household Spending Below Forecast, But Wedge With Real Wages Removed

Japan July real household spending was a touch below forecasts. We rose 1.4%y/y, against a 2.3% forecast and 1.3% outcome in June. In m/m terms, we rose a solid 1.7%. The chart below plots real spending and real earnings outcomes, both in y/y terms. Today's updates bring the two series a little more in line with each other. For a number of months spending trends looked too strong relative to a softer real earnings backdrop. In terms of the detail, food and housing spending was negative y/y, while strong gains were seen for transport and medical care.

Fig 1: Japan Real Household Spending & Real Earnings Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Futures Steady, OIS Up In Past Week, Sentiment Readings Next Week

Aussie bond futures sit little changed in Friday dealings, with domestic news/data flow light, while the US non-farm payrolls print is in firm focus later. 10yr futures (XM) were last at 95.63, up 1bps, with earlier highs at 95.645. For the 3yr future (YM), we were at 96.50.

- Cash ACGB yields sit mixed but aggregate moves are less than 1bps at this stage. The 10yr is down a touch to 4.34%, while the 3yr is holding near 3.48%. The 3/10s curve is a touch flatter near +86bps.

- The AU-US 10yr spread is close to +20bps, fresh highs back to early April. The bias in US Tsy futures has been higher today, but cash yield losses have been modest.

- RBA dated OIS contracts sit slightly over the past week. The Dec contract last around 3.30% (against an effective policy rate of 3.59%), we were at 3.26% at the end of last week. The Feb 2026 contract is around 3.21%, up close to 9bps over the past week.

- The Q2 GDP beat, and some hawkish Bullock comments around how easing is likely to be needed, have helped such trends.

- Next week, we get Westpac Consumer Sentiment and the NAB Business survey on Tuesday.

BONDS: NZGBS: Yields Lower Led By Back End

Benchmark NZGB yields sit lower across the curve. Losses have extended modestly as Friday trade unfolded. The back end has led the moves, with the 10yr yield off close to 2.5%, last around 4.39%. The 2yr yield is little changed, sitting near 2.95%. The 2/10s curve is flatter by around 1bps, tracking at +143.5bps currently. These moves largely mirror offshore developments from Thursday, with the US 10yr yield breaking sub 4.20%, on signs of softer labor market data. The bias so far today in US Tsy futures has been firmer.

- The NZ-US 10yr spread is just off multi month highs, last at +25bps. We have spent little time above +30bps for this metric since May of this year.

- The 2yr swap rate is little changed, near 2.76% in latest dealings.

- The data calendar has been empty today: Via BBG: "New Zealand special home-loan interest rates edged lower in August, according to data published Friday in Wellington by the Reserve Bank. Average one-year rate fell to 4.74% from 4.87% at the end of July, and is lowest since May 2022".

- Market pricing for the RBNZ outlook has not changed much this past week, with Feb 2026 OCR rate pricing holding under 2.60%.

- Next Tuesday we get Q2 manufacturing data, then on Wednesday net migration figures for July print.

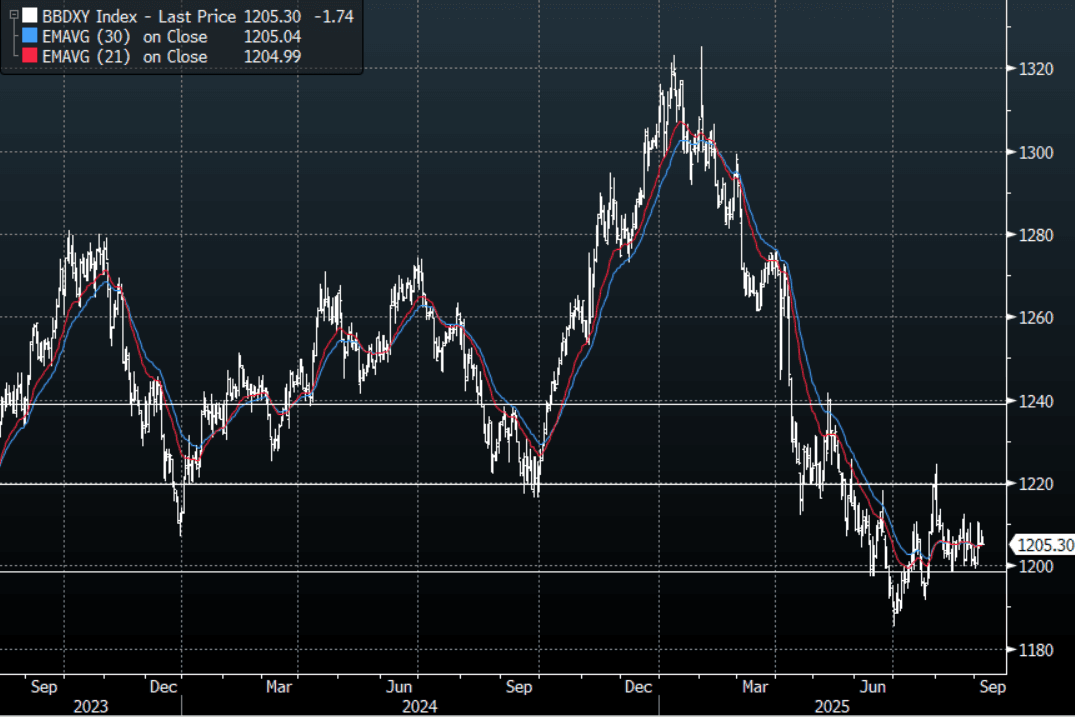

FOREX: Asia FX Wrap - USD Drifts Lower Into NFP

The BBDXY has had a range of 1204.89 - 1207.08 in the Asia-Pac session, it is currently trading around 1205, -0.15%. The USD was surprisingly able to shrug off the extension lower in US yields and actually ground higher overnight. Most of these gains have been retraced in today’s Asian session. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD is looking comfortable for the moment above this support, tonight's NFP print will determine if that remains the case.

- EUR/USD - Asian range 1.1648 - 1.1675, Asia is currently trading 1.1670. The pair is consolidating just above 1.1600 ahead of NFP, firmly within its wider 1.1350-1.1850 range.

- GBP/USD - Asian range 1.3430 - 1.3457, Asia is currently dealing around 1.3450. The pair collapsed in response to moves in UK bonds. Price bounced off its support around 1.3350, though I suspect offers should now find supply on rallies back towards 1.3500. A sustained break below 1.3350 would open up a move back to 1.3100.

- USD/CNH - Asian range 7.1318 - 7.1413, the USD/CNY fix printed 7.1064, Asia is currently dealing around 7.1325. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3557, US 10-Year 4.155%, BBDXY 1205, Crude Oil $63.33

- Data/Events : EZ Govt Expenditure/GDP/Employment, Germany Factory Orders, France Trade Balance, Spain INE House Price Index, Italy Retail Sales,

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

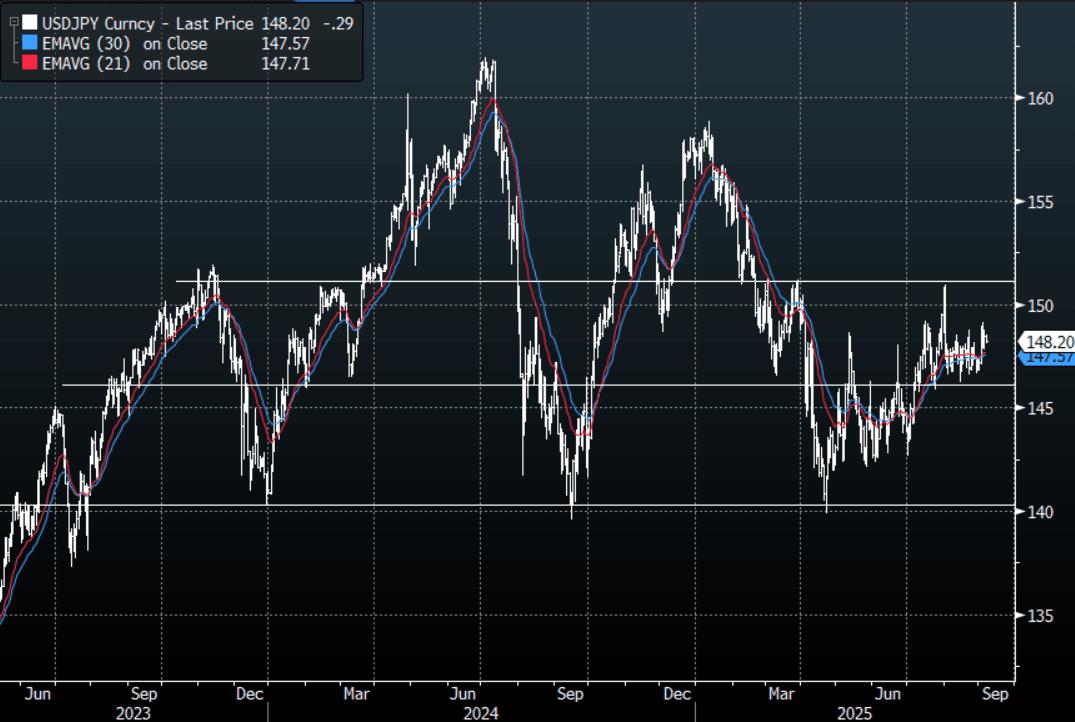

JPY: Asia Wrap - USD/JPY Drifts Back Toward148.00 Ahead Of NFP

The Asia-Pac USD/JPY range has been 148.08-148.54, Asia is currently trading around 148.20, -0.20%. USD/JPY continues to consolidate its recent gains on a 148 handle as we head into NFP. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. The price action looks pretty constructive but I would not be expecting any major extensions until the market has had a look at the NFP tonight, which given the reaction to this week's labour data could be a key driver.

- MNI BRIEF: Japan July Real Wages Positive Since Dec. The inflation-adjusted real wage, a key gauge of households’ purchasing power, turned positive in July for the first time since December 2024, rising 0.5% y/y after -0.8% in June. The rebound was driven by higher bonuses and wage hikes from annual labour negotiations. While supportive for the Bank of Japan’s case to raise rates, officials see the data as insufficient on its own, with focus instead on the likelihood of wage gains carrying into fiscal 2026.

- Bloomberg - “JGB Traders Are Counting On One-and-Done From BOJ. JGB 10-year yields are slightly lower despite today’s strong labor cash earnings data, with traders adopting the stance that one BOJ interest-rate hike is all that is achievable in the months ahead. Japan’s murky political situation will prevent the central bank from raising rates at a quicker pace, even though the agreed trade deal with US will underpin economic growth.”

- "AKAZAWA: NO CHANGE IN JAPAN'S PLAN FOR $550B INVESTMENT VEHICLE, $550 BILLION TO BE INVESTMENT, LOANS, LOAN GUARANTEES" - BBG

- "KATO: WILL DO UTMOST TO SUPPORT FINANCING OF SMALL FIRMS, CONTINUE TO WORK WITH US FOR SWIFT IMPLEMENTATION OF DEAL.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($2.36b), 147.00($1.12b).Upcoming Close Strikes : 146.00($1.1b Sept 8 ), 150.00($1b Sept 9) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

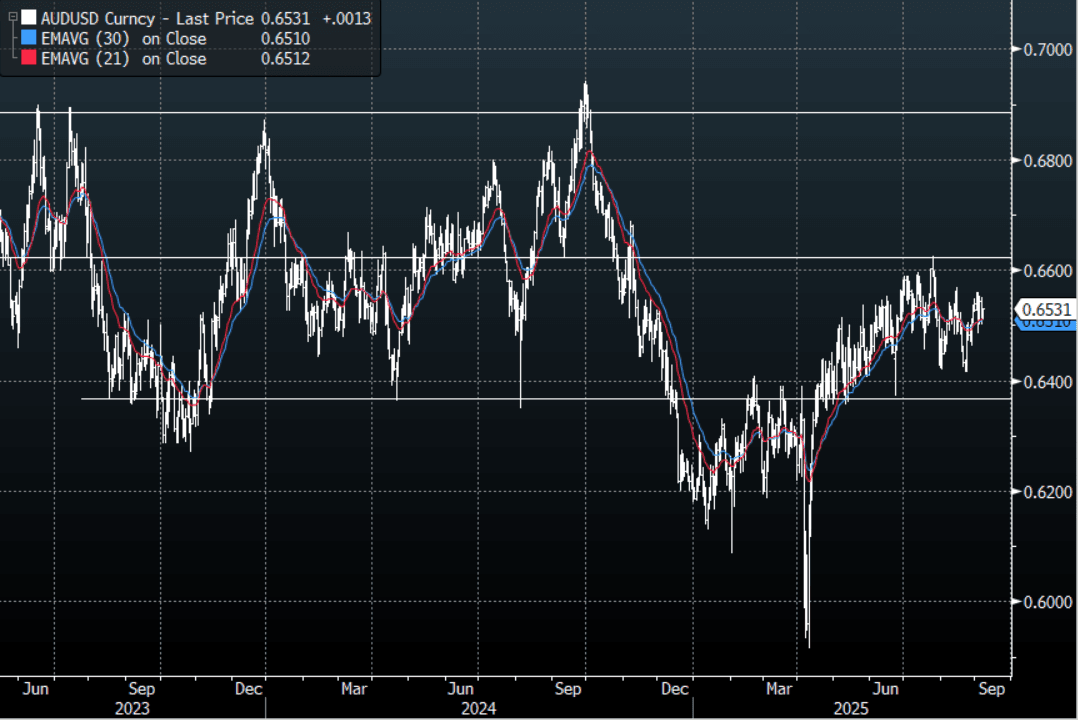

AUD: Asia Wrap - AUD/USD Takes Back Overnight Losses

The AUD/USD has had a range of 0.6515 - 0.6531 in the Asia- Pac session, it is currently trading around 0.6530, +0.20%. The AUD has drifted higher, erasing its overnight losses. The AUD remains in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP tonight to hopefully be a catalyst.

- MNI: China Bad Bank Calls Grow As Debt Overhang Saps Growth. Calls are growing for the creation of dedicated bad banks to absorb nonperforming loans by China’s local government and property developers, prominent scholars and policy advisors told MNI, though some stressed that moral hazard should be avoided to minimise the risk that the problems could recur.

- "AUSTRALIA'S DEFENSE MINISTER MARLES: TO BOOST STRATEGIC PARTNERSHIP WITH JAPAN." - BBG

- Bloomberg - “Dollar’s Distaste for Payrolls Paints Grim Friday Outlook. The dollar is primed for more weakness, with even modest payroll disappointments likely to trigger selloffs ahead of September’s Fed meeting.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD1.12b), 0.6500(AUD1.09b), 0.6600(AUD1.02b). Upcoming Close Strikes : 0.6475(AUD596m Sept 8 ) - BBG

- AUD/JPY - Asia-Pac range 96.68 - 96.83, Asia is trading around 96.80. The pair has broken back above 96.50 which negates the downward direction, a sustained break above 97.50 is needed to reignite the upward trend. Until then looks to be 94.50 - 97.50.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

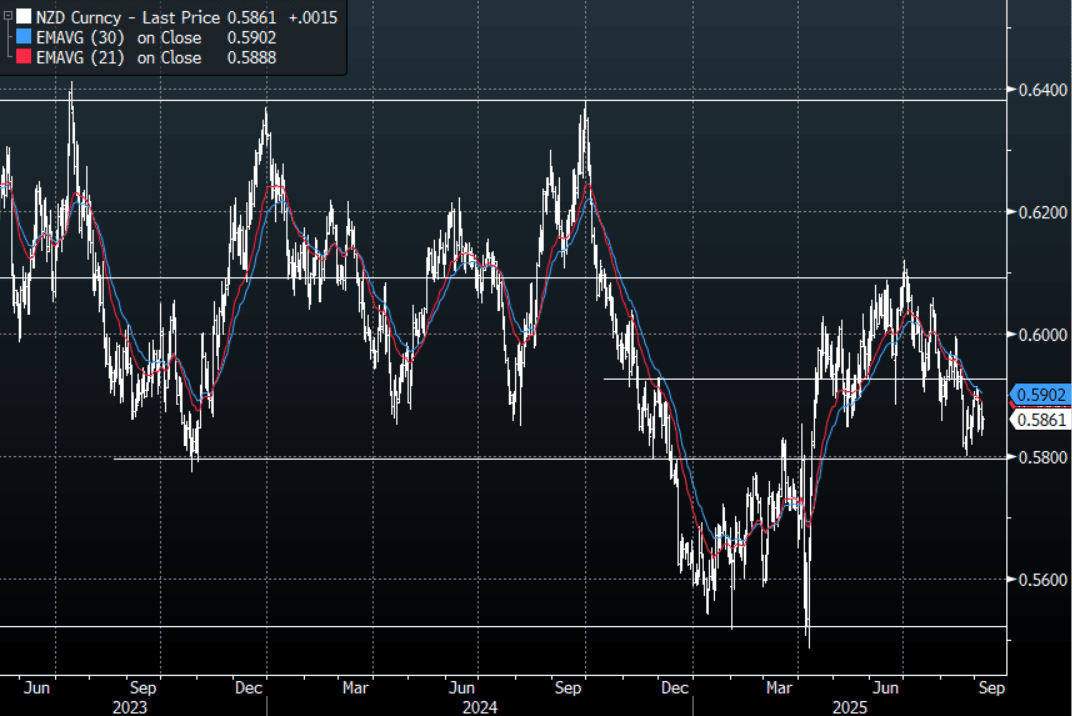

NZD: Asia Wrap - NZD/USD Erases Overnight Losses, Bounces Off 0.5800

The NZD/USD had a range of 0.5842 - 0.5865 in the Asia-Pac session, going into the London open trading around 0.5860, +0.25%. The NZD has drifted higher all session, erasing all its overnight losses as we head into NFP and moving away from its support back towards 0.5800. The NFP will be an important input as to whether this support continues to hold.

- MNI: China Bad Bank Calls Grow As Debt Overhang Saps Growth. Calls are growing for the creation of dedicated bad banks to absorb nonperforming loans by China’s local government and property developers, prominent scholars and policy advisors told MNI, though some stressed that moral hazard should be avoided to minimise the risk that the problems could recur.

- BBG - "New Zealand special home-loan interest rates edged lower in August, according to data published Friday in Wellington by the Reserve Bank. Average one-year rate fell to 4.74% from 4.87% at the end of July, and is lowest since May 2022".

- “Why New Zealand’s Easing Rich Foreigner Housing Rules: In April, New Zealand’s government found itself in a bind. It had just relaunched its golden visa program, offering wealthy foreigners residency in exchange for a minimum NZ$5 million ($3 million) investment. But there was a major hitch: existing laws prevented those investors from buying a home to live in — undercutting one of the main draws of relocating." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD515m Sept 10) - BBG

- AUD/NZD range for the session has been 1.1133 - 1.1154, currently trading 1.1140. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Ends Week with Rally

China announced more policy enhancements, this time aimed at the sporting sector. The State Council announced measures that provide loans and subsidized interest to sport companies and incentives to local / regional governments to boost sport. Companies such as Jiangsu Jinling, China Sports Industry, Jiangsu Kangliyuan Sports Tech, Sanfo Outdoor Product, China Sports Industry Group and Li Ning were up strongly, supporting the market performance today. Japan's stocks had a good end to the week also as the Trump tariff deal is signed, ending the uncertainty.

- The Hang Seng is up +0.62% today and the only one of the major bourses to be ahead (by +0.54%) for the week. The CSI 300 is up today by +0.88% (but down -2.07% for the week), Shanghai +0.35% (-2.05% for the week)) and Shenzhen +1.62% (-3.05% for the week).

- The NIKKEI had a wobble mid week on political concerns but has bounced back to be up +0.65% today, and +0.32% for the week.

- The TAIEX in Taiwan has had strong end to the week, up 1.00% today and +0.76% for the week.

- The KOSPI has done very little today but remains +0.55% higher for the week.

- The FTSE Malay KLCI is flat today and one of the few regional decliners this week, with falls of -0.60%

- The Jakarta Composite is lower today by -0.23% and is down -1.07% for the week as political concerns drove markets lower at the start of the week.

- The NIFTY 50 is marginally lower at the open yet on track for a positive week, currently up +1.15%.

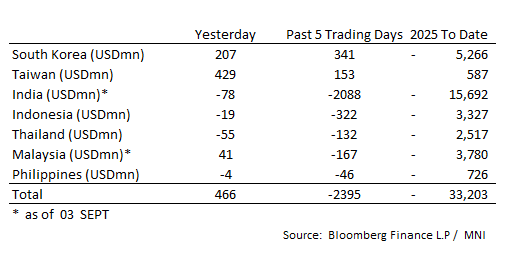

ASIA STOCKS: Equity Flow Update for Major Regional Bourses

Outflows from India continue, as Taiwan and South Korea have another day of inflows.

- South Korea: Recorded inflows of +$207m yesterday, bringing the 5-day total to +$341m. 2025 to date flows are -$5,266m. The 5-day average is +$68m, the 20-day average is -$17m and the 100-day average of +$60m.

- Taiwan: Had inflows of +$429m yesterday, with total inflows of +$153 m over the past 5 days. YTD flows are positive at +$587m. The 5-day average is +$31m, the 20-day average of -$198m and the 100-day average of +$189m.

- India: Had outflows of -$78m as of the 3rd, with total outflows of -$2,088m over the past 5 days. YTD flows are negative -$15,692m. The 5-day average is -$418m, the 20-day average of -$215m and the 100-day average of -$3m.

- Indonesia: Had outflows of -$19m yesterday, with total outflows of -$322m over the prior five days. YTD flows are negative -$3,327m. The 5-day average is -$64m, the 20-day average +$21m and the 100-day average -$13m.

- Thailand: Recorded outflows of -$55m yesterday, with outflows totaling -$132m over the past 5 days. YTD flows are negative at -$2,517m. The 5-day average is -$26m, the 20-day average of -$38m and the 100-day average of -$14m.

- Malaysia: Recorded inflows as of 3rd of +$41m, totaling -$167m over the past 5 days. YTD flows are negative at -$3,780m. The 5-day average is -$33m, the 20-day average of -$35m and the 100-day average of -$10m.

- Philippines: Recorded outflows of -$4m yesterday, with net outflows of -$46m over the past 5 days. YTD flows are negative at -$726m. The 5-day average is -$9m, the 20-day average of -$5m the 100-day average of -$5m.

- Oil is set to finish down for the week as concerns that this weekend's OPEC+ meeting could result in further supply drove oil lower overnight.

- Russian deputy PM Novak added to the pressure suggesting that OPEC+ will 'look at the situation as a whole before making a decision.'

- Adding to the downward pressure was data showing US crude inventories have risen to the highest in several months, suggesting that buying may be curtailed in the third quarter.

- Goldman Sach's analysts suggest that Brent could reach low $50s over the next year according to reports published by BBG.

- WTI is down in the Asia trading day by -0.22% to be at US$63.34. Since the 2025 high of US$80.04 in mid-January, WTI is now lower by over 20% and has no technical support below it, with all major moving averages above.

- For the week, WTI is lower by -1.03%

- Brent is down -0.16% at US$66.88 as it too has broken below all major moving averages.

- For the week, Brent is lower by -1.81%.

- Oil investors will have one eye on Non Farm payrolls tonight for clues as to the next Fed moves on rates.

Gold Holding Near New Highs Ahead of NFP

- After profit taking overnight saw gold prices fall by -0.38%, the rally resumed in the Asia trading day with gains of +0.31%.

- At US$3,556.80, gold sits just below the recent new highs of US$3,559.42.

- The rally that has been ongoing sees the precious metal sit above all major moving averages.

- Gold is currently up +3.20% and if these levels are held, it will be the best weekly return since June.

- The 14 day Relative Strength index is suggesting that Gold has moved into overbought territory.

- Gold investors have the non-farm payrolls tonight to focus on for clues as to the next interest rate cut.

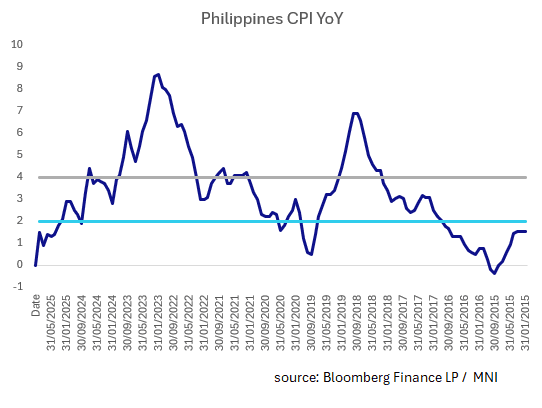

PHILIPPINES: CPI Edges Up in August; Remains Below Target

- Philippines August CPI YoY edged up to +1.5%, beating estimates of +1.2%.

- Despite trending upwards, CPI remains below the lower inflation band as set by the BSP of 2%.

- Core CPI rose +2.7% YoY and prices in the capital up 2.9% YoY

- Year to date CPI is up +1.7% YoY

- The monthly result sees prices up 0.6% MoM versus July 0.3%YoY

ASIA FX: Positive Bias, With TWD & THB Outperforming, INR Weakens Beyond 88.30

Asian currencies have traded with a positive bias against the USD (except for INR), in the first part of Friday dealings. TWD and THB have outperformed at the margins, while INR has lost ground versus the USD.

- USD/CNH is down around 0.10%, last near 7.1320, so within recent ranges. Onshore equities have rebounded today, probably a tailwind to the local FX. The CSI 300 is up 0.88%, back above 4400 in index terms. The USD/CNY fix edged up, while the fixing error was unchanged.

- Spot USD/KRW and USD/TWD are both lower, although have broken away from recent ranges. The better equity tone and some recovery in offshore equity inflows is likely helping. USD/KRW is back to 1392/93, up around 0.20% in won terms. We remain within striking distance of the 1400 level. Spot USD/TWD is back under 30.60, up 0.4% in TWD terms. Later on, we get Aug CPI.

- USD/THB is down around 0.35%, last near 32.22 and not too far from YTD lows. The local parliament is expected to elect a new PM today, while the positive gold price backdrop is another positive for the currency.

- USD/PHP is back under 57.00, but remains within recent ranges. August CPI was a touch above expectations but still sub the 2% target.

- USD/IDR is little changed, last in the 16465/70 region.

- USD/INR is to fresh highs above 88.30, off around 0.20% in INR terms. The pair has consolidated the break above 88.00 seen at the end of August. Exporters are expected to make a case to RBI Governor Malhorta next week for a weaker rupee in order to help offset the US tariff impact.

CHINA: Country Wrap: Cities Attempting to Revive Housing

- Chinese cities are experimenting with novel strategies to absorb unsold housing stock, in a fresh push to clear millions of vacant units, Securities Times reported. Some cities in the eastern province of Zhejiang have bundled rental income and parking fees into the revenue stream of purchased housing projects, lifting rental yields above 3%, where cities like Hefei, the capital of Anhui province, authorities combined urban and suburban residential assets to boost portfolio returns. Rental yields at China’s major 50 cities were at 2.06% only in 2024, below the average yield of 2.29% offered by local government special bonds, (source Securities Times)

- China’s financial market liquidity is expected to remain “reasonably ample” despite mounting pressure, underpinned by rising fiscal expenditures and support from the PBOC, Shanghai Securities News reported. PBOC may inject liquidity through outright reverse repos, Ming Ming, chief economist at Citic Securities, told the newspaper. It may auction 6-month outright reverse repos later this month, Ming was quoted as saying. PBOC may also add medium-term funds to financial system later this month via MLF, a one-year policy loan, says Wang Qing, analyst at Gold Credit Rating (source Shanghai Securities)

- The Hang Seng is up +0.62% today and the only one of the major bourses to be ahead (by +0.54%) for the week. The CSI 300 is up today by +0.88% (but down -2.07% for the week), Shanghai +0.35% (-2.05% for the week)) and Shenzhen +1.62% (-3.05% for the week).

- Yuan Reference Rate at 7.1064 Per USD; Estimate 7.1415

- The CGB 10-Yr is at 1.76%, having closed last night at 1.75%, and -2bp for the week.

SOUTH KOREA: Country Wrap: Korea Wants to Revive CPTPP

- Korea is moving to revive a bid to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), an Asia-Pacific trade bloc led by Japan, as it grapples with a global tariff war. The renewed push comes in response to U.S. President Donald Trump’s sweeping global tariffs, which are exerting pressure on export-reliant economies such as Korea to secure alternative markets and supply chain partners. The Lee Jae Myung administration has repeatedly expressed interest in joining the CPTPP, and on Wednesday confirmed that a potential membership in the trade alliance is under review. (source Korea Times)

- Korea Exchange (KRX) Chairman and CEO Jeong Eun-bo sees a sweeping industrial shift led by the innovative service sectors as key to propelling the benchmark KOSPI to an unprecedented 5,000 points. These promising sectors leverage knowledge, while supporting and integrating with manufacturing, to move away from decades of reliance on traditional brick-and-mortar businesses, according to Jeong. To this end, the chairman reaffirmed his commitment to crack down on underperforming “zombie companies” and promised to root out persistent unfair trading practices which have significantly contributed to the undervaluation of Korean equities. (source Korea Times)

- The KOSPI has done very little today but remains +0.55% higher for the week.

- The Won is one of the worst regional performers this week with falls of -0.15% to 1,391.90.

- Bonds have staged a rally today to see lower yields across the curve. KTB 10-Yr is at 2.86% +4bps for the week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 05/09/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/09/2025 | 0600/0700 | *** | Retail Sales | |

| 05/09/2025 | 0645/0845 | * | Foreign Trade | |

| 05/09/2025 | 0800/1000 | * | Retail Sales | |

| 05/09/2025 | 0900/1100 | * | Employment | |

| 05/09/2025 | 0900/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey | |

| 05/09/2025 | 1400/1000 | * | Ivey PMI | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |