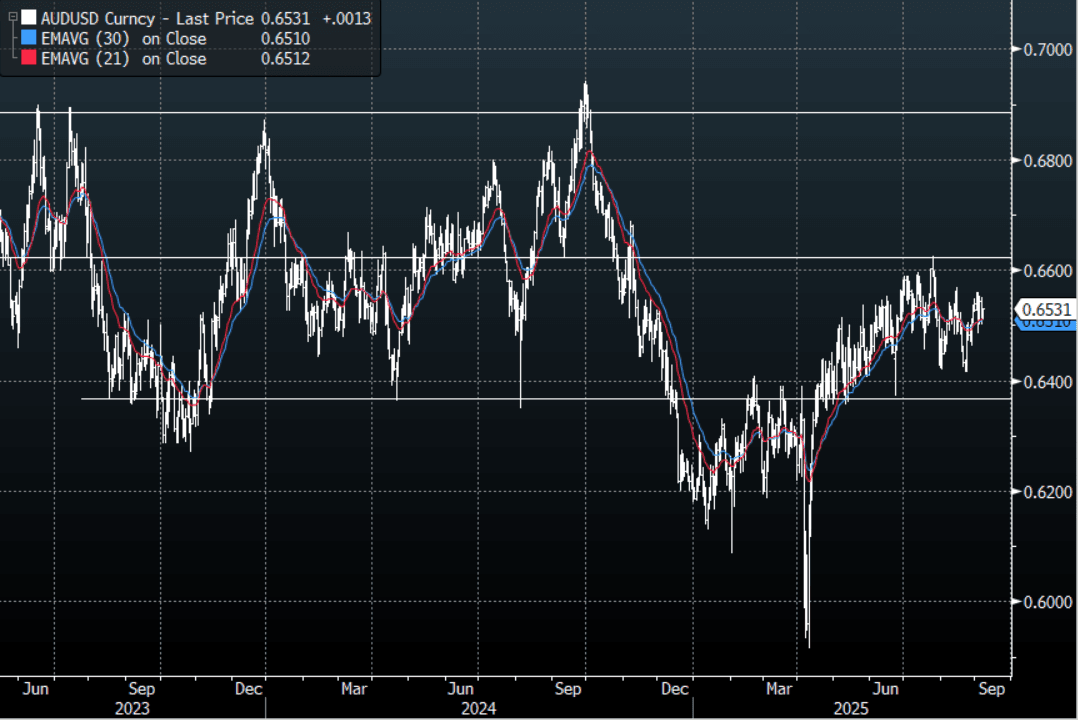

AUD: Asia Wrap - AUD/USD Takes Back Overnight Losses

The AUD/USD has had a range of 0.6515 - 0.6531 in the Asia- Pac session, it is currently trading around 0.6530, +0.20%. The AUD has drifted higher, erasing its overnight losses. The AUD remains in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP tonight to hopefully be a catalyst.

- MNI: China Bad Bank Calls Grow As Debt Overhang Saps Growth. Calls are growing for the creation of dedicated bad banks to absorb nonperforming loans by China’s local government and property developers, prominent scholars and policy advisors told MNI, though some stressed that moral hazard should be avoided to minimise the risk that the problems could recur.

- "AUSTRALIA'S DEFENSE MINISTER MARLES: TO BOOST STRATEGIC PARTNERSHIP WITH JAPAN." - BBG

- Bloomberg - “Dollar’s Distaste for Payrolls Paints Grim Friday Outlook. The dollar is primed for more weakness, with even modest payroll disappointments likely to trigger selloffs ahead of September’s Fed meeting.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD1.12b), 0.6500(AUD1.09b), 0.6600(AUD1.02b). Upcoming Close Strikes : 0.6475(AUD596m Sept 8 ) - BBG

- AUD/JPY - Asia-Pac range 96.68 - 96.83, Asia is trading around 96.80. The pair has broken back above 96.50 which negates the downward direction, a sustained break above 97.50 is needed to reignite the upward trend. Until then looks to be 94.50 - 97.50.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

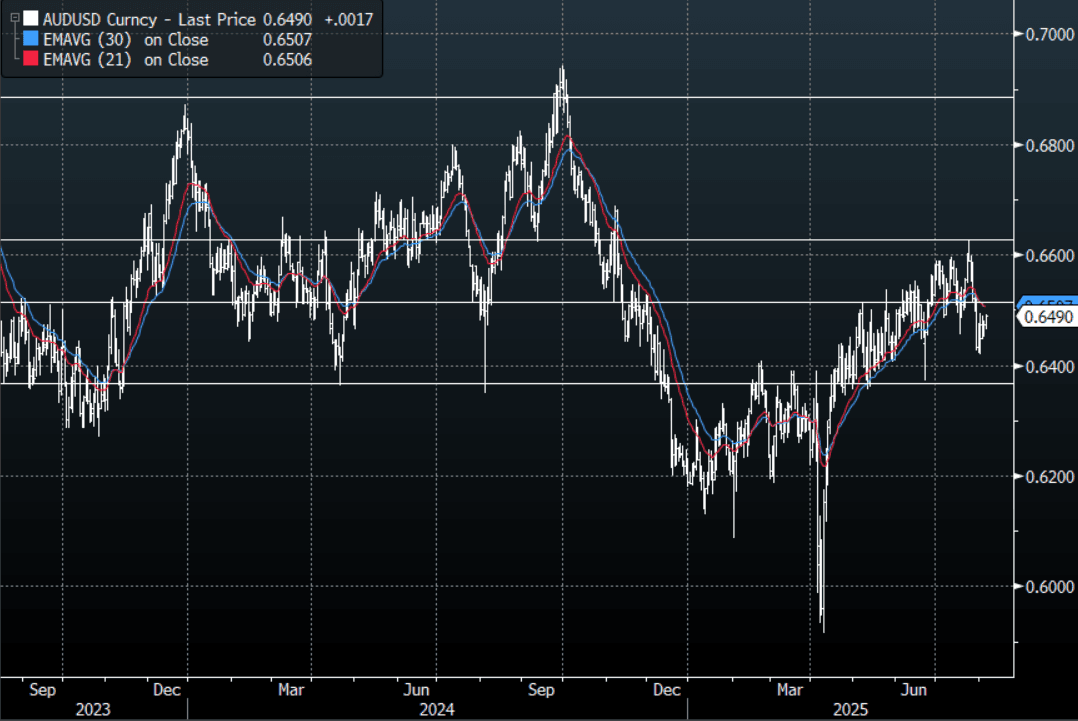

AUD: Asia Wrap - AUD/USD Gets A Boost From A Positive Asian Session For Risk

The AUD/USD has had a range of 0.6465 - 0.6492 in the Asia- Pac session, it is currently trading around 0.6490, +0.25%. The AUD has bounced in our session as Asian equities trade positively ignoring the wobble seen in the US in response to the ISM Services data. The AUD bounced nicely off the 0.6400 area but I suspect sellers might return back towards 0.6500/50 initially. I feel the performance of US equities over August/September will be crucial as seasonality points to some strong headwinds approaching.

- MNI Exclusive - The Reserve Bank of Australia looks set to cut the cash rate by 25 basis points to 3.6% on Aug 12, but further easing could prove a policy mistake and force the Bank to reverse course within six months unless a major global shock intervenes, former RBA board member Warwick McKibbin told MNI.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6575(AUD701m). Upcoming Close Strikes : 0.6500(AUD4.27b Aug 8), 0.6600(AUD1.97b Aug 7), 0.6800(AUD1.72b Aug 7) - BBG

- CFTC Data shows Asset managers reduced their shorts slightly -49183(Last -53959), the Leveraged community added to their own shorts -13997(Last -12010).

- AUD/JPY - Asia-Pac range 95.40 - 95.76, Asia is trading around 95.70. The pair failed on multiple attempts above 97.00 and has moved swiftly back to test its first support toward the 95.00 area. There should be sellers around the 96.00/96.50 area initially, a sustained break below 94.50/95.00 could signal a deeper move lower.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

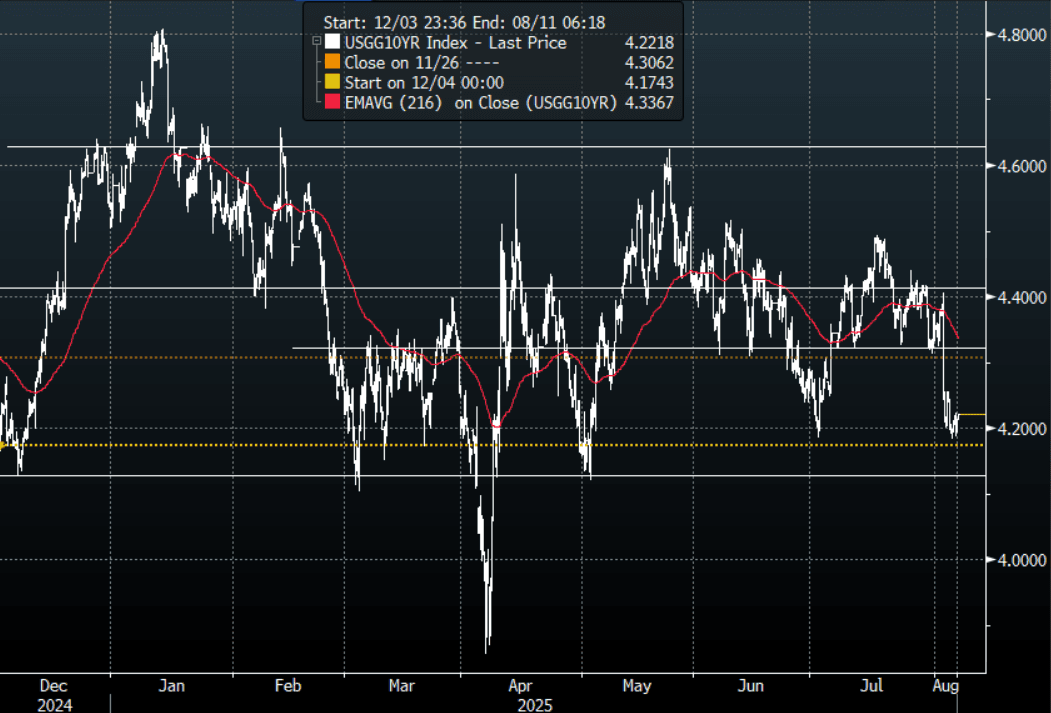

US TSYS: Asia Wrap - Yields Edge Higher In A Quiet Session

The TYU5 range has been 112-04 to 112-07 during the Asia-Pacific session. It last changed hands at 112-04, down 0-05 from the previous close.

- The US 2-year yield has edged higher trading around 3.726%.

- The US 10-year yield has moved higher trading around 4.222%, up 0.01 from its close.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Bloomberg - “Trump said he’ll pick a successor for Adriana Kugler before the end of the week. He added that the replacement for Jerome Powell is down to four people and that Scott Bessent declined to be considered for the role.” - BBG

- The Department of the Treasury will auction $42 billion of August 2035 notes

- Bloomberg - “Bond traders are increasingly betting on up to 75 bps in Fed rate cuts in 2025 amid signs of a weakening US economy. The shift in sentiment follows soft payrolls data and stagnation in the services sector.”

- Truflation on X: “PCE close to 2%! All inflation metrics are falling. No more excuses. No more empty words. It's time to act, Powell.”

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

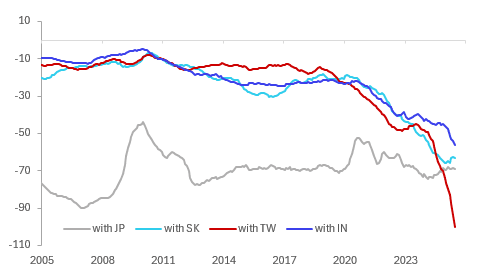

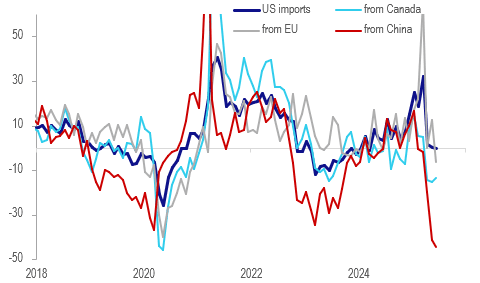

GLOBAL MACRO: Sharp Narrowing In US Deficits With China, EU & Canada

In line with global export growth peaking in March, US data shows that its trade deficit peaked at the same time. Countries front loaded shipments to beat the early April reciprocal tariff announcement. Ship tracking data for May show that the number of container vessels moderated, and consistent with this the US June visible trade deficit fell to its lowest in over two years. Given the bringing forward of shipments, the data is going to be difficult to interpret over H2. It will take time to see what the impact from the increase in the US effective tariff rate to around 16% will be on the deficit.

- Bilateral balances have generally turned over 2025. The deficit with Canada narrowed around $2.1bn in June from March but almost $10bn since January, China’s $8.4bn and $22.2bn respectively and the EU’s $37.6bn and $13.4bn.

- Looking at Asian trends, the 12-month sum of the US deficit with Japan has stabilised, narrowed with China and Korea, but deteriorated with India and especially Taiwan.

US merchandise trade deficit $bn 12mth sum

- The monthly deficit with Taiwan has consistently widened over 2025 as negotiations with the US took place. Its reciprocal tariff was reduced to 20% from 32% but uncertainty over its key chip shipments continues. The number of ships leaving for the US has moderated since late July but remain around the recent average.

- US imports growth peaked in March at 32.3% y/y and fell 0.2% y/y in June driven by sharp declines from its main trading partners. Imports from Canada fell 13.7% y/y, 6.3% from the EU but a sharp 44.5% from China.

- There also seems to have been a frontloading of US exports with growth peaking at 10.8% y/y in April as firms were likely concerned about retaliation. This has moderated since with June only 3.4% y/y.

US merchandise imports y/y%

Source: MNI - Market News/LSEG