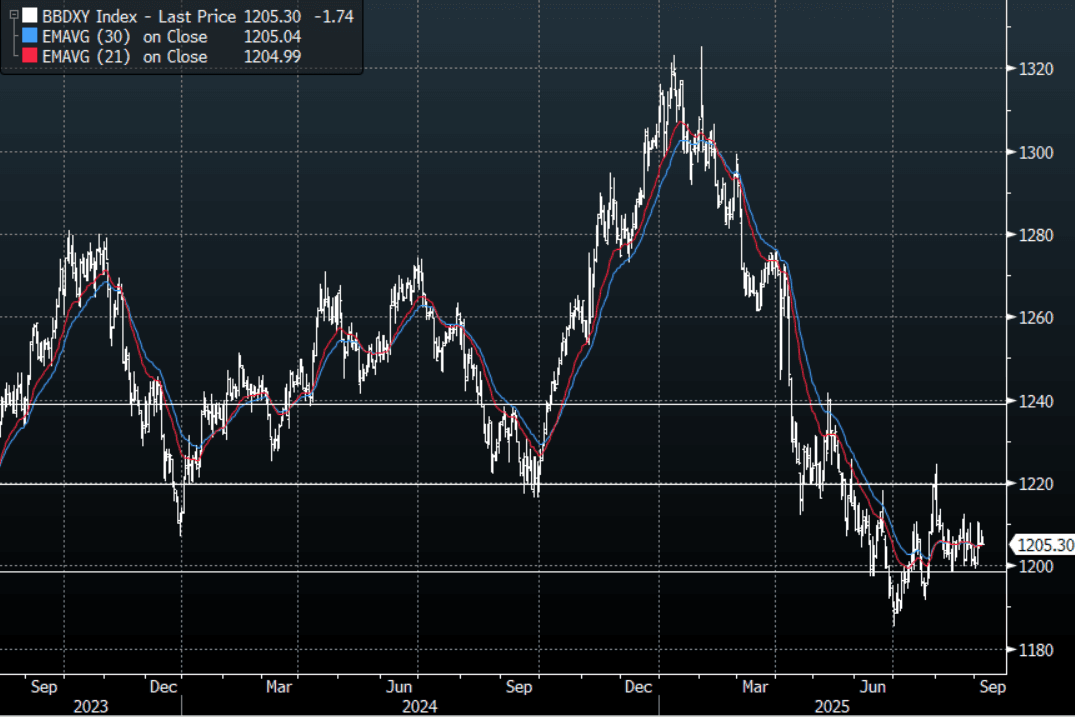

FOREX: Asia FX Wrap - USD Drifts Lower Into NFP

The BBDXY has had a range of 1204.89 - 1207.08 in the Asia-Pac session, it is currently trading around 1205, -0.15%. The USD was surprisingly able to shrug off the extension lower in US yields and actually ground higher overnight. Most of these gains have been retraced in today’s Asian session. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD is looking comfortable for the moment above this support, tonight's NFP print will determine if that remains the case.

- EUR/USD - Asian range 1.1648 - 1.1675, Asia is currently trading 1.1670. The pair is consolidating just above 1.1600 ahead of NFP, firmly within its wider 1.1350-1.1850 range.

- GBP/USD - Asian range 1.3430 - 1.3457, Asia is currently dealing around 1.3450. The pair collapsed in response to moves in UK bonds. Price bounced off its support around 1.3350, though I suspect offers should now find supply on rallies back towards 1.3500. A sustained break below 1.3350 would open up a move back to 1.3100.

- USD/CNH - Asian range 7.1318 - 7.1413, the USD/CNY fix printed 7.1064, Asia is currently dealing around 7.1325. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3557, US 10-Year 4.155%, BBDXY 1205, Crude Oil $63.33

- Data/Events : EZ Govt Expenditure/GDP/Employment, Germany Factory Orders, France Trade Balance, Spain INE House Price Index, Italy Retail Sales,

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Closed At Worst Levels But Only Modestly Cheaper

NZGBs closed 3bps cheaper across benchmarks, with the NZ-US 10-year yield differential little changed on the day.

- Cash US tsys are flat to 2bps cheaper, with a steepening bias, in today's Asia-Pac session after yesterday's twist-flattener. Today’s US calendar will see BA Mortgage Applications.

- NZ employment was weaker in Q2 than the RBNZ projected in May declining 0.1% q/q and 0.9% y/y, in line with consensus, after a downwardly-revised 0.0% q/q & -0.7% y/y in Q1. The unemployment rate rose 0.1pp to 5.2%, highest since Covid-impacted Q3 2020, but as the RBNZ forecast. The next rate decision is on August 20 and will include an updated outlook. With job shedding continuing and activity indicators remaining lacklustre and inflation in the band, another 25bp rate cut is likely.

- Swap rates closed 1-2bps higher, with the 2s10s curve little changed.

- RBNZ dated OIS pricing closed slightly firmer across meetings. 23ps of easing is priced for August, with a cumulative 41bps by November 2025.

- Tomorrow, the local calendar will see RBNZ Inflation Expectations data.

- The NZ Treasury also plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

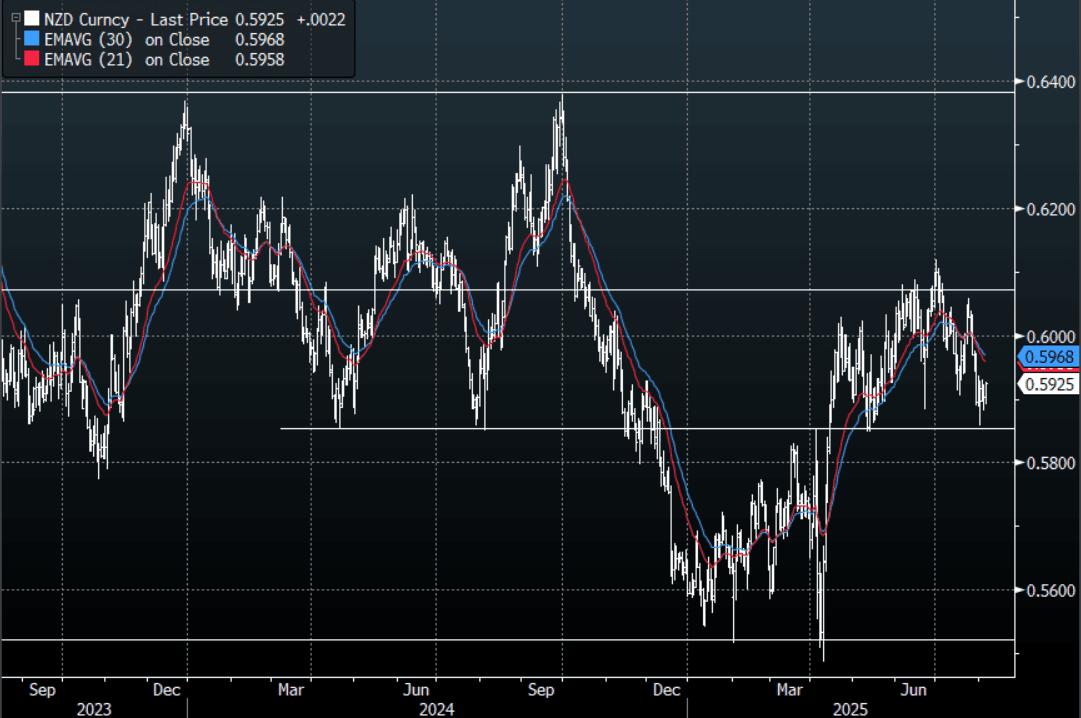

NZD: Asia Wrap - NZD/USD Bounces On a Better Employment Print & Positive Risk

The NZD/USD had a range of 0.5891 - 0.5926 in the Asia-Pac session, going into the London open trading around 0.5925, +0.37%. The NZD has bounced in our session in response to a better than expected unemployment print and Asian equities trading positively ignoring the wobble seen in the US in response to the ISM Services data. NZD/USD bounced nicely off its 0.5850 support but I would suspect sellers could return on any bounce back toward 0.6000. With the seasonality for risk looking poor there is a chance it tests the pivotal 0.5800/50 area, a break of which would open up a move back to the 0.5500 lows.

- NEW ZEALAND: Q2 Sees Increased Labour Market Capacity. NZ employment was weaker in Q2 than the RBNZ projected in May declining 0.1% q/q and 0.9% y/y, in line with consensus, after a downwardly-revised 0.0% q/q & -0.7% y/y in Q1. The unemployment rate rose 0.1pp to 5.2%, highest since Covid-impacted Q3 2020, but as the RBNZ forecast. The next rate decision is on August 20 and will include an updated outlook. With job shedding continuing and activity indicators remaining lacklustre and inflation in the band, another 25bp rate cut is likely.

- “NZ FINANCE MINISTER WILLIS: EXPECT UNEMPLOYMENT TO FALL LATER THIS YEAR, EXPECT EXPORTS TO CONTINUE TO BOOM. INCREASED US TARIFF RATE ON NZ WON'T HAVE BIG IMPACT" - BBG

- Kelly Eckhold(Westpac NZ) on LinkedIn: “Today's labour market reports came in a touch stronger than our forecasts but more or less in line with the RBNZ's thinking. The Unemployment rate rise to 5.2% instead of our 5.3% forecast. While jobs growth remains weak, the under 20's are moving out of the workforce and heading into training. The NEET rate was unchanged this quarter in seasonally adjusted terms. I think this is a return to normality for this younger cohort and bodes well for their future.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD496m Aug 7), 0.5920(NZD483m Aug 11), 0.5930(NZD646m Aug 11). - BBG

AUD/NZD range for the session has been 1.0949 - 1.0982, currently trading 1.0955. The Cross moved lower in response to the better employment print but continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

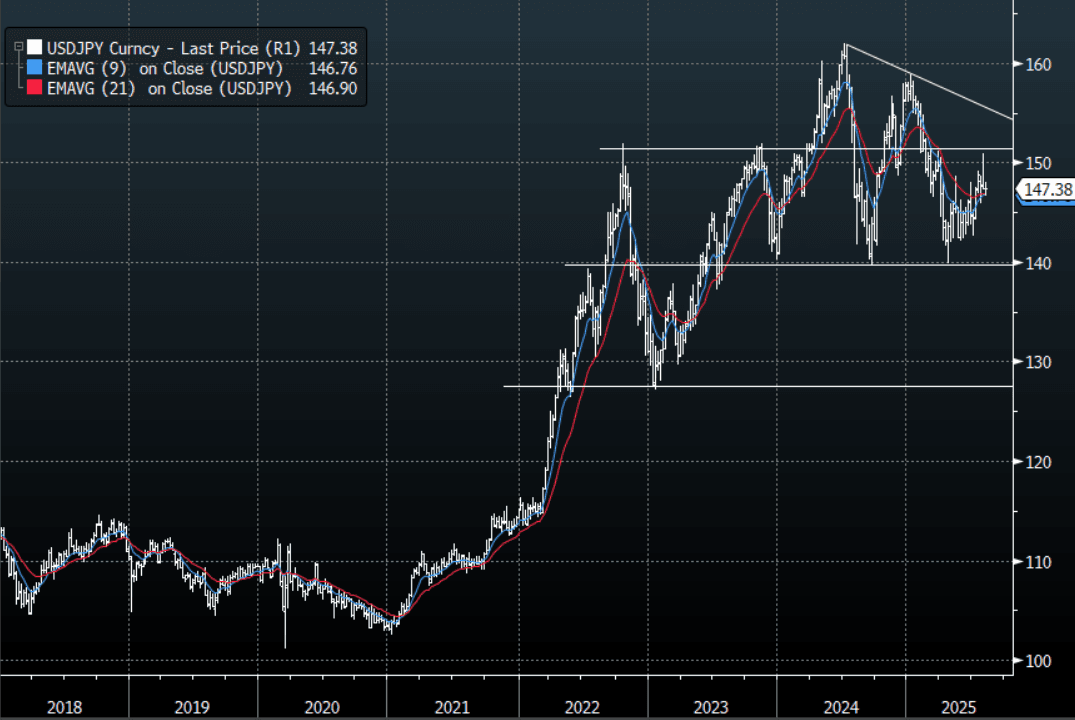

JPY: Asia Wrap -USD/JPY Drifts Lower Shrugging Off Wage Data.

The Asia-Pac USD/JPY range has been 147.34 - 147.75, Asia is currently trading around 147.35, -0.20%. USD/JPY initially tried higher after weaker than expected wage data, but good sellers towards 148.00 continue to cap for now. Price has moved very quickly away from the pivotal 151/152 area much to the relief of Institutional Yen longs and the BOJ. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. Price is holding above the support area around 146.50/147.00 for now, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate.

- "HAYASHI: AGREED W/ US THAT JAPAN PHARM WON'T BE AT DISADVANTAGE” - BBG

- "JAPAN'S KONO: NECESSARY TO RAISE RATES TO STRENGTHEN YEN" - BBG

- (MNI) Japan's inflation-adjusted real wage, a key gauge of household purchasing power, remained in negative territory for a sixth consecutive month in June but narrowed to -1.3% from May's 2.6% decline, preliminary data from the Ministry of Health, Labour and Welfare showed Wednesday.

- (Bloomberg) - The Japanese currency’s recent strength can be expected to wane somewhat after wages data came in substantially weaker than had been expected. That’s likely to be seen as reinforcing the BOJ’s instinctive policy caution, pushing traders to pare back already modest bets on a rate hike this year.

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.5b).Upcoming Close Strikes : 147.65($1.14b Aug 7), 148.50($1.24b Aug 7) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P