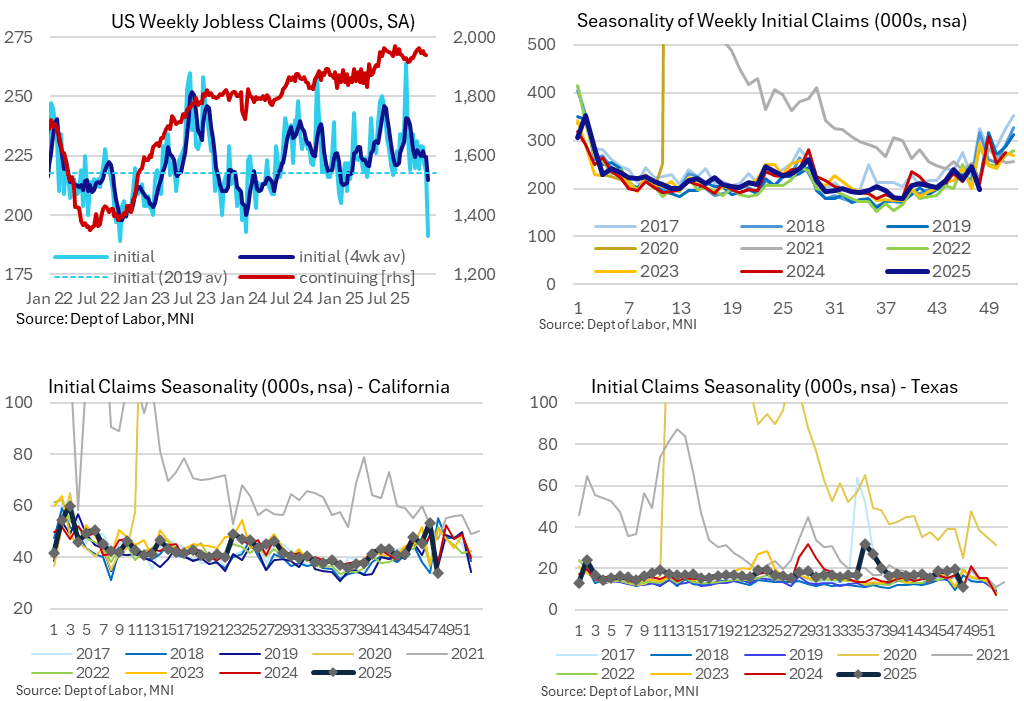

MNI ASIA OPEN: Weekly Jobless/Continuing Claims Slide

EXECUTIVE SUMMARY

- MNI TARIFFS: Trump Administration Teases Withdrawing From USMCA Trade Agreement

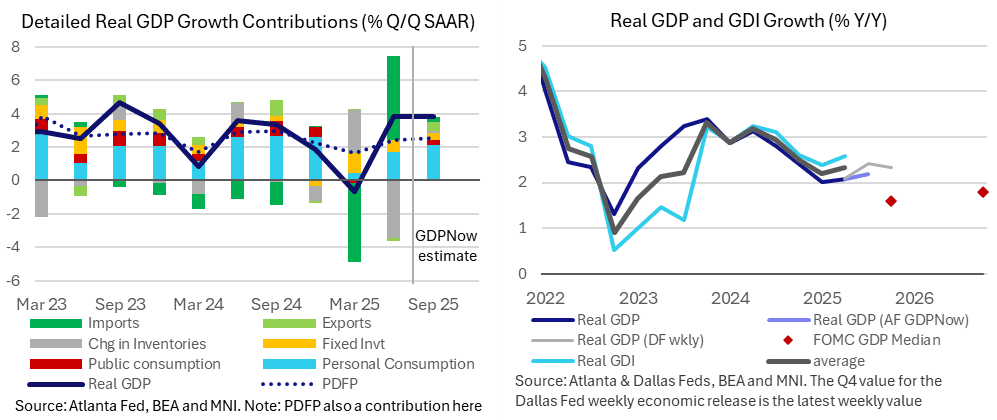

- MNI US DATA: Atlanta and Dallas Fed GDP Tracking Points To Higher FOMC Forecast

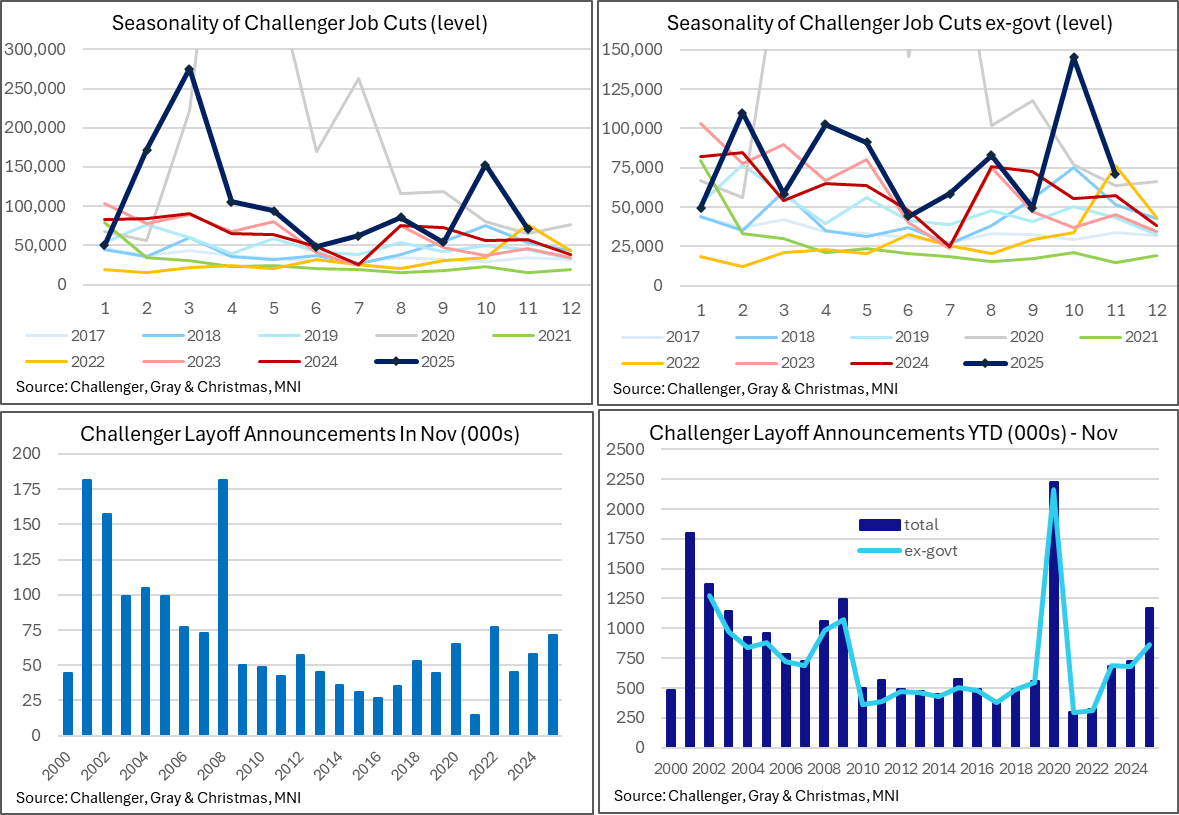

- MNI US DATA: A Less Drastic Increase In Challenger Layoff Announcements

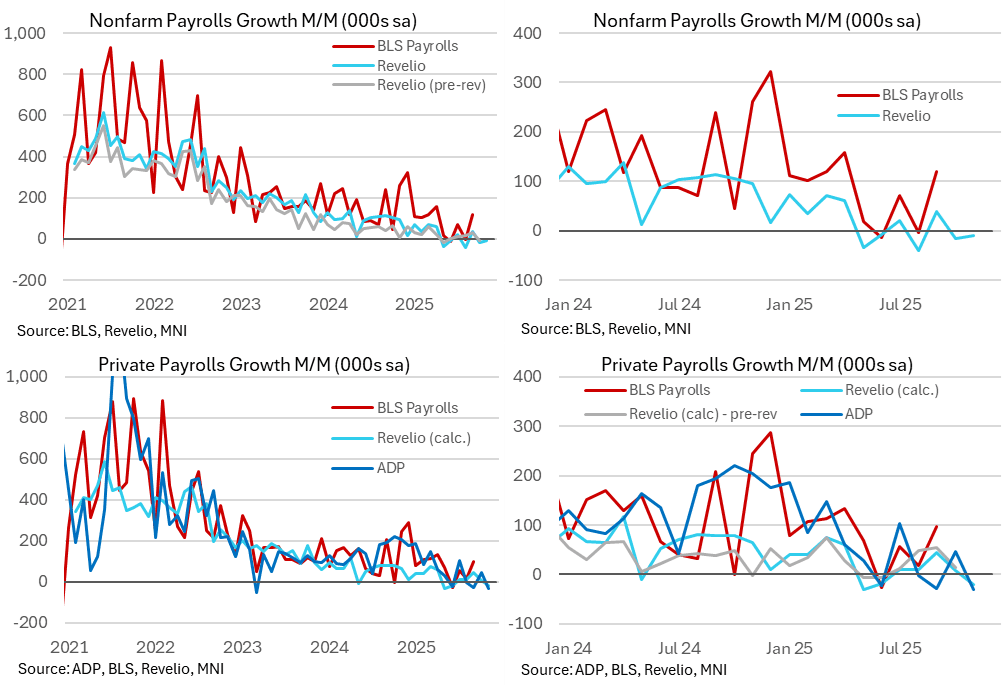

- MNI US DATA: Revelio Labs Echo ADP Decline In November But Revisions Cloud Release

- MNI US DATA: Initial Jobless Claims Slide Lower With A Thanksgiving Caveat

US

FINANCIAL TIMES: US senators seek to block Nvidia sales of advanced chips to China

US: MNI POLITICAL RISK - Trump Pardon Undermines GOP Messaging

- President Donald Trump will greet DR Congo President Felix Tshisekedi and Rwandan President Paul Kagame at the newly renamed “Donald J. Trump Institute of Peace” in Washington, DC, for the signing of a peace deal at 12:10 ET 17:10 GMT.

- Trump announced new fuel economy standards that would roll back Biden-era rules aimed at cutting emissions and promoting electric cars.

- Wall Street executives and bond investors expressed concern to the US Treasury over NEC Director Kevin Hassett's potential nomination as Federal Reserve chair.

- Lawmakers declined to include an AI export control bill in the Pentagon spending bill, amid lobbying from Nvidia.

MNI TARIFFS: Trump Administration Teases Withdrawing From USMCA Trade Agreement

US Trade Representative Jamieson Greer told Politico that President Donald Trump is “flirting with” pulling the US out of the United States-Mexico-Canada trade agreement. When asked about the possibility of withdrawing ahead of July’s mandatory review, Greer said, “that's always a scenario. [Trump] only wants [good deals]. The reason why we built a review period into USMCA was in case we needed to revise it, review it or exit it.” Trump told reporters yesterday, "We'll either let it expire, or we'll maybe work out another deal with Mexico and Canada.”

MNI SECURITY: Witkoff To Brief UKR Officials In Miami, Peace Process Appears Stalled

US Special Envoy Steve Witkoff and US President Donald Trump’s son-in-law, Jared Kushner, will meet Ukrainian national security adviser Rustem Umerov in Miami today to debrief on Tuesday’s meeting with Russian President Vladimir Putin in Moscow. Although Trump described the Moscow meeting as “reasonably good,” it appears to have delivered little progress on peace negotiations.

NEWS

MNI TARIFFS: Optimism For US-India Trade Deal As US Delegation Preps Delhi Trip

The Press Trust of India reports that a US trade delegation is likely to visit New Delhi next week for talks with Indian counterparts. The trip is the latest sign that negotiators could be close to completing the first tranche of a trade deal by year end, understood to include the relaxation of tariffs. The news comes as Indian Prime Minister Narendra Modi hosts Russian President Vladimir Putin for a two-day visit - his first since the start of the Ukraine war - aimed at deepening commercial and political ties.

US TSYS

MNI US TSYS: Revisiting Early Session Lows, Surprise Weekly Claims Decline

- Treasuries look to finish near early Thursday session lows - grinding lower all day after rebounding from this morning's knee-jerk sell-off following lower than expected weekly and continuing jobless claims data.

- Currently, TYH6 trades -11.5 at 112-24 vs. 112-22 low, key support and Nov 5 low below at 112-07.

- Initial jobless claims were far lower than expected at 191k (sa, cons 220k) in the week to Nov 29 after a marginally upward revised 218k (initial 216k). It’s the lowest seasonally adjusted figure since Sep 2022 although we’re always cautious about reading too much into a single week around the Thanksgiving holiday.

- Continuing claims were also better than expected but less surprisingly so, at 1939k (sa, cons 1963k) in the week to Nov 22 after another downward revision to 1943k (initial 1960k).

- The Atlanta Fed’s GDPNow has been revised down marginally from 3.85% to 3.81% for annualized real GDP growth in Q3. Ahead of next week’s FOMC meeting, it currently paints a very similar picture to the 3.84% in Q2. What’s more, the drivers behind this quarterly growth are indicative of underlying strength, with private domestic final purchases estimated at ~2.9% annualized after 2.86% in Q2.

- Look ahead to Friday: Personal Income/Outlays, UofM Consumer Survey. Non-Farm payrolls are not released tomorrow but are rescheduled for December 16.

OVERNIGHT DATA

MNI US DATA: Initial Jobless Claims Slide Lower With A Thanksgiving Caveat

Initial jobless claims contained by far the biggest surprise of today’s 0830ET labor releases, sliding to a seasonally adjusted 191k for its lowest single week since Sep 2022 in a move that we suspect is distorted by Thanksgiving adjustment difficulties. California and Texas also accounted for more than half the weekly decline in the NSA data. Continuing claims meanwhile pulled back from close to cycle highs in the 1960ks whilst its previous weekly value was unsurprisingly revised lower for a mixed comparison with recent payrolls reference periods.

- Initial jobless claims were far lower than expected at 191k (sa, cons 220k) in the week to Nov 29 after a marginally upward revised 218k (initial 216k). It’s the lowest seasonally adjusted figure since Sep 2022 although we’re always cautious about reading too much into a single week around the Thanksgiving holiday.

- Continuing claims were also better than expected but less surprisingly so, at 1939k (sa, cons 1963k) in the week to Nov 22 after another downward revision to 1943k (initial 1960k).

MNI US DATA: Revelio Labs Echo ADP Decline In November But Revisions Cloud Release

Revelio Labs estimate non-farm payrolls growth of -9k in November (sa M/M) after -15k in October (revised from -9k), 38k in Sep (from 33k) and a large downward revision to -40k back in Aug (from 14k in last month’s vintage).

- Large revisions are a theme of this month’s release and as such we caution placing too much weight on the report until we have a better understanding of benchmarking – it was un-paywalled in the government shutdown so we don’t have much track history of month-to-month revisions.

- Whilst the Oct level of nonfarm payrolls estimate is near unchanged, the Jan 2021 level is 2.25m lower that with last month’s release, i.e. seeing an additional 2.25m jobs created). It had been undershooting alternate measures of employment growth so this closes the gap somewhat.

MNI US DATA: A Less Drastic Increase In Challenger Layoff Announcements

Challenger job cut announcements pulled back after October’s surge although still saw a solid increase on an year ago. Latest weekly initial jobless claims for the week to Nov 22 (Nov 29 lands at 0830ET) don’t yet appear to show signs of these recent increases but will continue to be watched as lags can be quite long.

- Challenger reports job cut announcements summed to 71.3k in November, a 24% Y/Y increase.

- It pulls back from a particularly sharp increase to 153k in October, a 175% Y/Y rise for its highest October since 2003.

- Latest optics are still weak however with the 71k for a November last higher in 2022 and before that 2008.

MNI US DATA: Atlanta and Dallas Fed GDP Tracking Points To Higher FOMC Forecast

The Atlanta Fed’s GDPNow has been revised down marginally from 3.85% to 3.81% for annualized real GDP growth in Q3. It continues a slow moderation from 4.2% estimates in the second half of November but is still towards the high end of the longer than usual window for Q3 estimates. This extended run for the GDPNow is because the government shutdown has meant we missed the BEA advance and second estimates on Oct 30 and Nov 26 respectively. The next release is set for an “initial” estimate on Dec 23.

- Ahead of next week’s FOMC meeting, it currently paints a very similar picture to the 3.84% in Q2. What’s more, the drivers behind this quarterly growth are indicative of underlying strength, with private domestic final purchases estimated at ~2.9% annualized after 2.86% in Q2.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 64.14 points (-0.13%) at 47816.37

S&P E-Mini Future down 1 points (-0.01%) at 6860

Nasdaq up 26.3 points (0.1%) at 23478.07

US 10-Yr yield is up 4.1 bps at 4.1039%

US Mar 10-Yr futures are down 11/32 at 112-24.5

EURUSD down 0.0028 (-0.24%) at 1.1643

USDJPY down 0.15 (-0.1%) at 155.1

WTI Crude Oil (front-month) up $0.71 (1.2%) at $59.66

Gold is up $4.59 (0.11%) at $4208.02

European bourses closing levels:

EuroStoxx 50 up 23.52 points (0.41%) at 5718.08

FTSE 100 up 18.8 points (0.19%) at 9710.87

German DAX up 188.32 points (0.79%) at 23882.03

French CAC 40 up 34.61 points (0.43%) at 8122.03

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +4.618, 39.24 (L: 34.62 / H: 40.66)

2Y10Y +0.352, 57.924 (L: 56.616 / H: 58.115)

2Y30Y -0.622, 123.699 (L: 122.326 / H: 124.7)

5Y30Y -1.6, 108.368 (L: 107.521 / H: 109.996)

Current futures levels:

Mar 2-Yr futures down 2.75/32 at 104-10.875 (L: 104-10.25 / H: 104-13.625)

Mar 5-Yr futures down 7.75/32 at 109-12.75 (L: 109-11.5 / H: 109-19.75)

Mar 10-Yr futures down 11/32 at 112-24.5 (L: 112-22 / H: 113-02)

Mar 30-Yr futures down 19/32 at 116-3 (L: 115-30 / H: 116-19)

Mar Ultra futures down 24/32 at 119-7 (L: 119-02 / H: 119-26)

MNI US 10YR FUTURE TECHS: (H6) Bearish Tone

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-11/22+ High Dec 1 / High Nov 25

- PRICE: 112-25+ @ 1120 ET Dec 4

- SUP 1: 112-22 Low Dec 02 & 04

- SUP 2: 112-10+ Low Nov 20

- SUP 3: 112-07 Low Nov 5 and a key support

- SUP 4: 112-02+ Low Sep 25

A bearish theme in Treasuries remains intact. Price has this week pierced support around the 50-day EMA, at 112-27. A clear breach of this average would undermine a recent bull theme and signal scope for a deeper retracement. This would open 112-07, the Nov 5 high and a bear trigger. A reversal higher is required to once again refocus attention on the key resistance and bull trigger at 113-29+, the Oct 17 high.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.008 at 96.270

Mar 26 -0.020 at 96.450

Jun 26 -0.030 at 96.675

Sep 26 -0.040 at 96.830

Red Pack (Dec 26-Sep 27) -0.055 to -0.045

Green Pack (Dec 27-Sep 28) -0.06 to -0.055

Blue Pack (Dec 28-Sep 29) -0.06 to -0.06

Gold Pack (Dec 29-Sep 30) -0.065 to -0.06

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.95% (-0.06), volume: $3.360T

- Broad General Collateral Rate (BGCR): 3.90% (-0.06), volume: $1.331T

- Tri-Party General Collateral Rate (TCR): 3.90% (-0.06), volume: $1.302T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $153B

FED Reverse Repo Operation

RRP usage slips to $2.233B while counterparties retreat by 1 to 39 this afternoon from $2.514B Wednesday. Compares to last Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $3.5B Rep of South Africa 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 12/04 $3.5B #Rep of South Africa $1.75B 12Y 6.25%, $1.75B 30Y 7.375%

- 12/04 $500M *Yapi Kredi WNG 10.5NC5.5 7.55%

- 12/04 $500M OneMain Finance 7.75NC3 6.75%

- 12/04 $Benchmark MercadoLibre 7Y +135

EGBS

• 2y/10y bunds are closing +1bp/+2bp at 2.07%/2.77%. UST 10yr +3.7bps as initial claims came in low.

• €IG closes -1.2bp on average.

• Supply - EUR Fins: DB (Long 5NC4 SP). GBP Corps: ARNDTN (7yr SUN).

• SX5E/SPX futures are +0.5%/-0.1% at 5730pts/6857pts. €IG movers included Hyundai Motor Co (+6%), 3i Group (+6%), Daimler Truck Holding (+5%), Renault (+5%), PVH (-11%), Koninklijke Philips (-6%), Tauron Polska Energia (-4%), LyondellBasell Industries (-4%).

• Main/XO finish +0.3bp/+1bp at 52.8bp/256bp

MNI FOREX: USD Index Plumbs Fresh Pullback Lows Before Stabilising

- The USD traded with more mixed sentiment on Friday, as initial momentum selling may have stalled in respect of the well below-forecast initial jobless claims data – providing a moderately more optimistic short-term view of the US labour market. The USD index traded down to a pullback low of 98.77, however, looks set to post a small winning day as we approach the APAC crossover.

- USDJPY was a focus through European trade, as headlines surrounding the December BOJ meeting helped bolster expectations for an imminent hike. The yen received a decent boost, prompting USDJPY to reach a new weekly low of 154.51, before the post-data stabilisation has seen spot edge closer to 155 at typing. Most recent price action has strengthened the chances for a deeper correction, targeting the 50-day EMA at 153.34.

- In similar vein, GBPUSD briefly extended its impressive surge on Wednesday, rallying as high as 1.3385. Sterling strength was driven by both the key break of 0.8746-51 in EUR/GBP as well as the continued unwind of pre-Budget vol. 3m GBPUSD implied vol is now at the second-lowest level for this time of year of this century, after 2012.

- AUDUSD also traded through the late October highs of 0.6618 and has now posted 9 consecutive sessions of higher highs. While negative carry for long AUDUSD remains, acute pressure in the front-end of the curve means the 3m carry / vol ratio is at the highest level since April.

- In emerging markets, USDMXN slipped to an 11-week low and hovers just above the cycle lows and key support level at 18.20. Importantly, President Sheinbaum is expected to meet President Trump tomorrow, providing some more tepid optimism over upcoming trade discussions. We have emphasised the dominant downtrend in place, signalling the potential for a larger move towards 17.4491.

- Canadian employment data headlines tomorrow’s economic calendar. US monthly PCE data and Michigan sentiment figures will also be released.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/12/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/12/2025 | 0730/0730 | DMO to publish issuance calendar for FQ4 | ||

| 05/12/2025 | 0745/0845 | * | Industrial Production | |

| 05/12/2025 | 0745/0845 | * | Foreign Trade | |

| 05/12/2025 | 0800/0900 | ** | Industrial Production | |

| 05/12/2025 | 0900/1000 | * | Retail Sales | |

| 05/12/2025 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit |