FOREX: USD Index Plumbs Fresh Pullback Lows Before Stabilising

- The USD traded with more mixed sentiment on Friday, as initial momentum selling may have stalled in respect of the well below-forecast initial jobless claims data – providing a moderately more optimistic short-term view of the US labour market. The USD index traded down to a pullback low of 98.77, however, looks set to post a small winning day as we approach the APAC crossover.

- USDJPY was a focus through European trade, as headlines surrounding the December BOJ meeting helped bolster expectations for an imminent hike. The yen received a decent boost, prompting USDJPY to reach a new weekly low of 154.51, before the post-data stabilisation has seen spot edge closer to 155 at typing. Most recent price action has strengthened the chances for a deeper correction, targeting the 50-day EMA at 153.34.

- In similar vein, GBPUSD briefly extended its impressive surge on Wednesday, rallying as high as 1.3385. Sterling strength was driven by both the key break of 0.8746-51 in EUR/GBP as well as the continued unwind of pre-Budget vol. 3m GBPUSD implied vol is now at the second-lowest level for this time of year of this century, after 2012.

- AUDUSD also traded through the late October highs of 0.6618 and has now posted 9 consecutive sessions of higher highs. While negative carry for long AUDUSD remains, acute pressure in the front-end of the curve means the 3m carry / vol ratio is at the highest level since April.

- In emerging markets, USDMXN slipped to an 11-week low and hovers just above the cycle lows and key support level at 18.20. Importantly, President Sheinbaum is expected to meet President Trump tomorrow, providing some more tepid optimism over upcoming trade discussions. We have emphasised the dominant downtrend in place, signalling the potential for a larger move towards 17.4491.

- Canadian employment data headlines tomorrow’s economic calendar. US monthly PCE data and Michigan sentiment figures will also be released.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

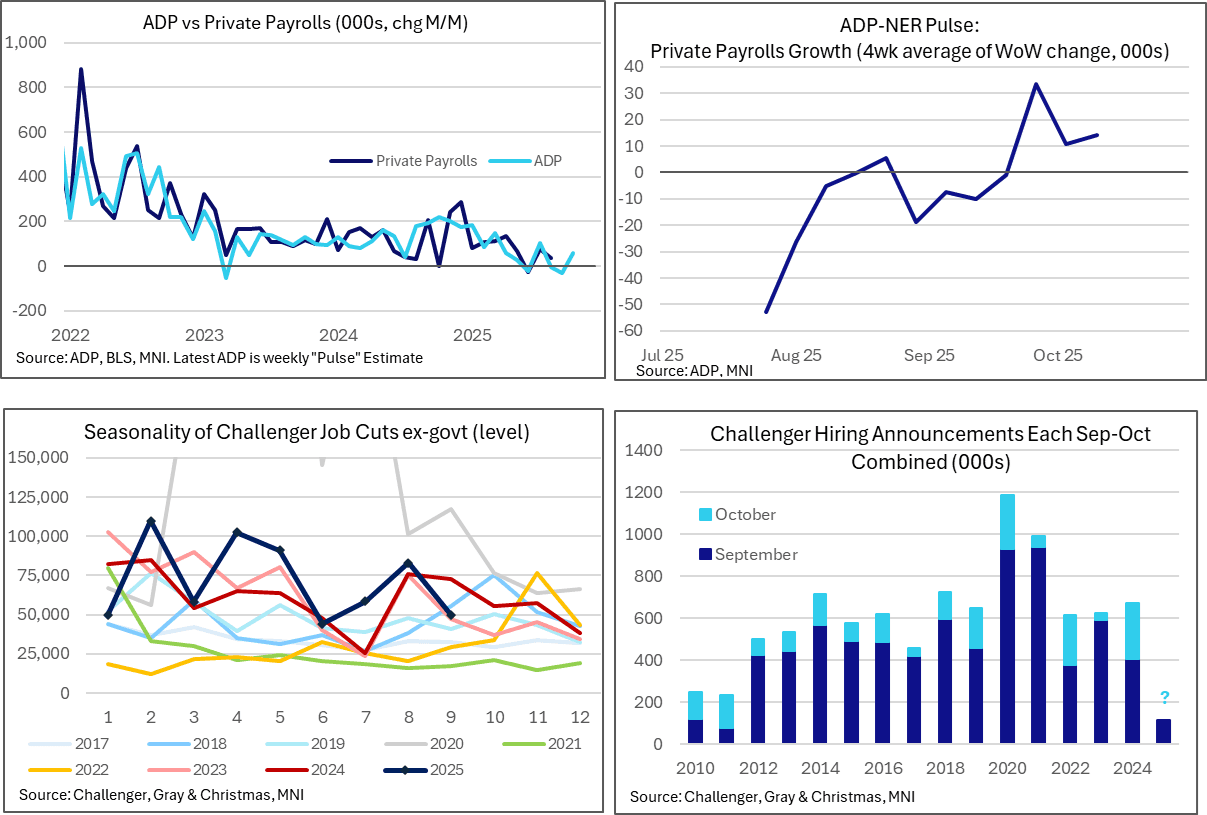

US DATA: Private Labor Indicators To Watch Over The Next Two Days

The next two days see some private sector labor indicators that likely will see particular attention this week with a lack of BLS releases. ADP is expected to see some stabilization after recent job losses, with added questions over how its regular monthly report correlates with a newly published weekly series, whilst the Challenger report offers a look at hiring plans for a second important seasonal month.

- The ADP employment report on Wednesday is expected to point to a 40k increase in private payrolls in October after a surprisingly weak -32k in September and -3k in August.

- Surprisingly released last week, the ADP weekly “Pulse” report pointed to private payrolls growth of 57k over the course of the four weeks ending Oct 11, reported as an average weekly increase of 14.25k.

- There are question marks as to how this weekly series correlates with the longer standing monthly report but with clearly some expectation that the labor market stabilized in October vs prior ADP-implied additional weakness.

- The Challenger report on Thursday meanwhile will be watched not only for its usual summary of layoffs in October but also the second useful month for hiring plans, being highly sensitive to seasonal hiring typically announced in September and October.

- Layoffs encouragingly fell 26% Y/Y in last month’s report for September, the largest decline since January, albeit flattered by an unusually high Sep 2024.

- Hiring plans were extremely low however in a key month of September, at just 117k vs 404k last year, and should be watched for October. There should be a 250k contribution from Amazon in October, although that was also the case in Oct 2024, i.e. the timing of Amazon plans wasn’t behind last month’s weak reading. Rather, anecdotal evidence points to broader hiring lethargy, with Target for instance in 2024 announcing 100k of seasonal workers (as has been the case since 2021) but this year it has in part instead offered additional hours to its current employees.

EURUSD TECHS: Bear Cycle Extension

- RES 4: 1.1728 High Oct 17

- RES 3: 1.1669 High Oct 28 and key resistance

- RES 2: 1.1577/1618 Low Oct 22 / 20-day EMA

- RES 1: 1.1542 Low Oct 9

- PRICE: 1.1492 @ 16:13 GMT Nov 4

- SUP 1: 1.1460 1.382 proj of the Oct 17 - 22 - 28 price swing

- SUP 2: 1.1425 1.500 proj of the Oct 17 - 22 - 28 price swing

- SUP 3: 1.1392 Low Aug 1 and bear trigger

- SUP 4: 1.1313 Low May 30

A bear leg in EURUSD remains intact and Tuesday’s extension reinforces current conditions. The move down maintains the bearish price sequence of lower lows and lower highs. Furthermore, the pair has breached a number of important short-term supports, the most recent being 1.1516, the 76.4% retracement of the Aug 1 - Sep 17 bull leg. This exposes key support at 1.1392, the Aug 1 low. Initial resistance is 1.1542, the Oct 9 low.

OPTIONS: Condors Remain In Vogue Across Rates

Tuesday's Europe rates/bond options flow included:

- RXZ5 131/132cs, bought for 4 in 3.8k

- ERM6 98.125/98.50/98.875 call fly, bought for 5 in 10k

- ERM6 98.75 call, paper pays 1.0 in 9k

- ERM6 98.18/98.25/98.37/98.43c condor, bought for 0.75 in 4k total

- SFIZ5 96.15/96.25/96.35/96.45 c condor, sold at 4.5 in 5k

- SFIG6 96.50/96.40/96.25/96.05p condor sold at 3.75 and 3.5 in 4.56k

- SFIH6 96.45/96.55/96.65/96.75c condor vs 96.25/96.15ps, bought the condor for 1.5 in 11k total on the day

- SFIJ6 96.70/96.80 call spread paper paid 2.75 on 8K vs. 96.555