US TSYS: Revisiting Early Session Lows, Surprise Weekly Claims Decline

Dec-04 20:53

- Treasuries look to finish near early Thursday session lows - grinding lower all day after rebounding from this morning's knee-jerk sell-off following lower than expected weekly and continuing jobless claims data.

- Currently, TYH6 trades -11.5 at 112-24 vs. 112-22 low, key support and Nov 5 low below at 112-07.

- Initial jobless claims were far lower than expected at 191k (sa, cons 220k) in the week to Nov 29 after a marginally upward revised 218k (initial 216k). It’s the lowest seasonally adjusted figure since Sep 2022 although we’re always cautious about reading too much into a single week around the Thanksgiving holiday.

- Continuing claims were also better than expected but less surprisingly so, at 1939k (sa, cons 1963k) in the week to Nov 22 after another downward revision to 1943k (initial 1960k).

- The Atlanta Fed’s GDPNow has been revised down marginally from 3.85% to 3.81% for annualized real GDP growth in Q3. Ahead of next week’s FOMC meeting, it currently paints a very similar picture to the 3.84% in Q2. What’s more, the drivers behind this quarterly growth are indicative of underlying strength, with private domestic final purchases estimated at ~2.9% annualized after 2.86% in Q2.

- Look ahead to Friday: Personal Income/Outlays, UofM Consumer Survey. Non-Farm payrolls are not released tomorrow but are rescheduled for December 16.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

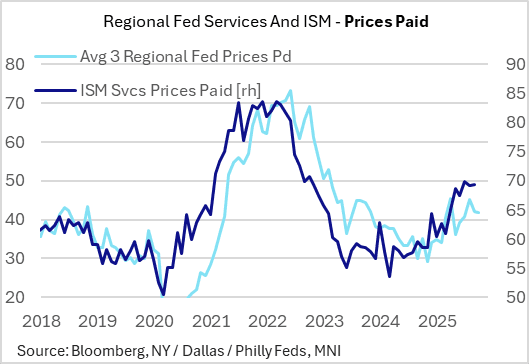

US PREVIEW: Oct ISM Services: Price Gauge Seen At 4-Month Low (2/2)

Nov-04 20:49

The ISM Services Prices Paid gauge is seen falling to 67.8 in October from 69.4 prior. That would represent a 4-month low.

- The flash October PMI report however suggested that output, rather than input prices were softer: "Prices charged for goods and services rose at the slowest rate since April, but firms' costs continued to increase sharply, attributed to the impact of tariffs alongside upward wage pressures."

- Regional Fed surveys don't contradict the expected ISM pullback in current prices paid though the evidence is quite mixed. NY Fed and Richmond current prices paid rose, while KC, Dallas, and Philly Fed gauges fell to 3/4-month lows.

- The Richmond Fed was the clear outlier to the upside but it uses a different methodology to express price pressures (on a Y/Y % change basis, it rose to a 15-month high 5.5%) versus the other Feds which are sequential.

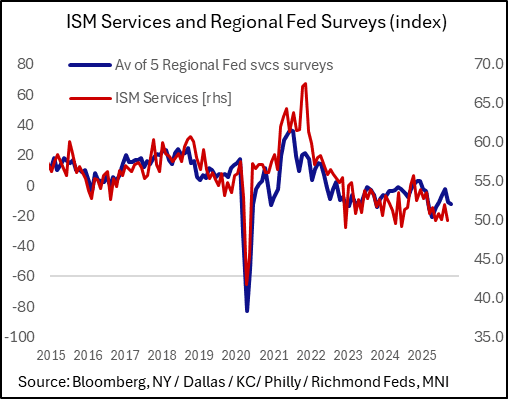

US PREVIEW: Oct ISM Services: Activity Steadying Out At A Weak Level (1/2)

Nov-04 20:38

The ISM Services survey for October (Wednesday, 1000 ET) is expected to see a modest uptick in the headline PMI index to 50.8 (50.0 prior), with the Employment sub-gauge steady at 47.3 (47.2 prior). The latter will be particularly closely watched in a week that will see the October nonfarm payrolls release postponed indefinitely due to the government shutdown.

- September's ISM reading was below expectations, marked a 4-month low and came amid a notable pullback in new orders (50.4), while the Business Activity index at 49.9 indicated the first contraction since May 2020.

- October's Manufacturing ISM out Monday was weaker than expected, in terms of the headline index (48.7 vs 49.1 in Sep, and consensus 49.5), with continued softness in new orders and employment.

- Activity across regional Feds' services surveys was quite mixed in October, with NY, Philly and Dallas all deteriorating vs improvements in KC and Richmond. At best it implies a steady ISM services reading vs September (see chart).

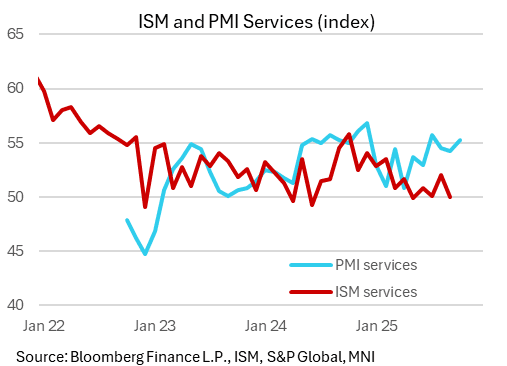

- As with the Manufacturing surveys, the S&P Global PMI has been more positive on the Services sector relative to ISM: it printed 55.2 in the October flash, for a 3-month high. The overall PMI report (including manufacturing) pointed to the 2nd fastest growth of the year, with improvements in output and new work in services.

US TSYS: Tsys Hold Higher Levels Ahead Midweek Data & Tsy Refunding Annc

Nov-04 20:33

- Treasuries look to finish modestly higher Tuesday - upper half of narrow session range as markets await Wednesday's non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services as well as US Tsy Quarterly Refunding annc.

- Currently, the Dec'25 10Y contract trades +4.5 at 112-26 vs. 112-28.5 high, 10Y yield -.0272 at 4.0832%. The contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

- The next two days see some private sector labor indicators that likely will see particular attention this week with a lack of BLS releases. ADP is expected to see some stabilization after recent job losses, with added questions over how its regular monthly report correlates with a newly published weekly series, whilst the Challenger report offers a look at hiring plans for a second important seasonal month.

- Analysts' outlooks for Wednesday's refunding reflect almost no expectations for any major changes, but there is increasing attention being paid to the likelihood of increased bill issuance ahead as coupon sizes aren't increased until well into 2026 at least.

- Greenback underpinned Tuesday, prompting the USD index to establish its position back above the 100 mark, at fresh recovery highs. The index traded to within 4 pips of the August 01 highs. Price action led an impressive lurch lower for spot gold, which briefly extended declines to 1.8% on the day to $3,930/oz.

- Stocks expected to announce earnings after the close include: Arista Networks Inc, Live Nation Entertainment, Corteva, Rivian Automotive, Advanced Micro Devices, American International Grp, Mosaic Co, Pinterest, Match Group, AES Corp, Super Micro Computer, Amgen Inc.