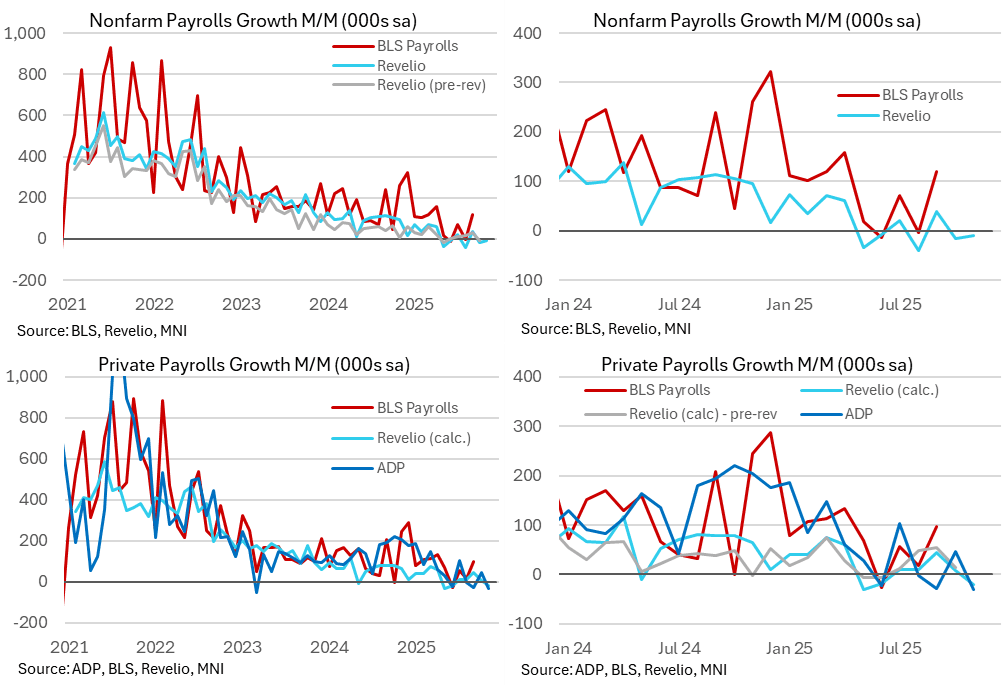

US DATA: Revelio Labs Echo ADP Decline In November But Revisions Cloud Release

Dec-04 14:24

- Revelio Labs estimate non-farm payrolls growth of -9k in November (sa M/M) after -15k in October (revised from -9k), 38k in Sep (from 33k) and a large downward revision to -40k back in Aug (from 14k in last month’s vintage).

- Large revisions are a theme of this month’s release and as such we caution placing too much weight on the report until we have a better understanding of benchmarking – it was un-paywalled in the government shutdown so we don’t have much track history of month-to-month revisions.

- Whilst the Oct level of nonfarm payrolls estimate is near unchanged, the Jan 2021 level is 2.25m lower that with last month’s release, i.e. seeing an additional 2.25m jobs created). It had been undershooting alternate measures of employment growth so this closes the gap somewhat.

- Treating with caution, five of the past seven months have seen employment declines in its overall payrolls estimate. Private payrolls (total ex public administration) have seen weaker recent momentum however, rolling over with-19k in Nov after an 8k increase in Oct, having last declined in May (-30k) and June (-19k).

- A reminder on Revelio's methodology: they estimate monthly changes in unemployment by looking at professional profiles sourced from professional networking websites eg LinkedIn: "RPLS provides a set of employment statistics derived from over 100 million professional profiles sourced from professional networking websites. After deduplication, adjustments for reporting lags, and reweighing to ensure that the data resembles the national distribution of the workforce, these data yield timely and detailed measures of employment dynamics."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUR: FX Exchange traded Call Buyer

Nov-04 14:12

EURUSD (6th Mar) 1.1800c, bought for 0.008 in ~4.6k.

EFSF ISSUANCE: New 5-year Nov-30 / 2.875% Jan-2035 tap: Priced

Nov-04 14:04

New 5-year benchmark

- Reoffer: 99.629 / 2.580%

- Spread set earlier at MS+22bps (guidance was MS+24 bps area)

- Size: E3.0bln (E2.5-3.5bln)

- Final books in excess of E23.5bln (ex JLM interest)

- Maturity: 11 November 2030

- Coupon: 2.50%

- Hedge ratio: 100% vs 2.20% Oct-30 Bobl (Spot ref 99.755 +33.0bp)

- ISIN: EU000A2SCAV2

- Timing: TOE 13:37GMT / 14:37CET. FTT immediately.

2.875% Jan-2035 tap

- Reoffer: 98.928 / 3.009%

- Spread set earlier at MS+39bps (guidance was MS+42 bps area)

- Size: E1.5bln (middle of MNI's expected E1.0-2.0bln)

- Final books in excess of E22.5bln (ex JLM interest)

- Hedge ratio: 98% vs 2.50% Feb-35 Bund (Spot ref 99.064 + 39.5bp)

- ISIN: EU000A2SCAS8

- Timing: TOE 13:38GMT / 14:38CET. FTT immediately.

For both:

- Settlement: 11 November 2025 (T+5)

- Bookrunners: BNPP / BofA (DM/B&D) / NATWEST

From market source / MNI colour

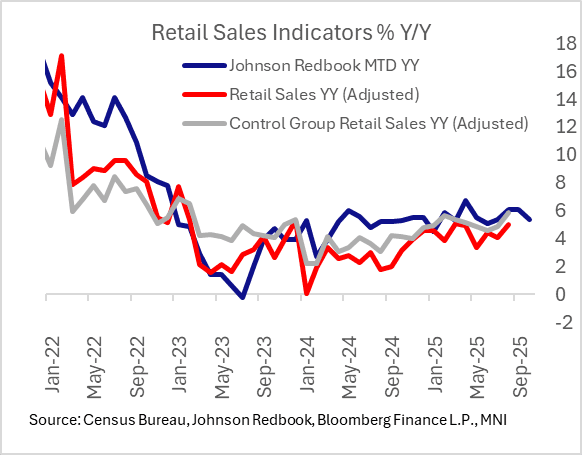

US DATA: Redbook Retail Sales Close Out October On Solid Footing

Nov-04 13:58

Retail sales growth picked up in the final week of October to 5.7% Y/Y from 5.2% prior, per the Johnson Redbook index. This kept October's sales at +5.4% Y/Y, same as the month-to-date figure estimated for the prior week albeit slightly below retailers' targeted 5.6% gain.

- The report notes that "the past week saw an increase in customer traffic and sales, primarily driven by demand for Halloween merchandise. However, the holiday may have negatively impacted shopping patterns on Friday, a key day for retailers, by diverting customers away from stores while boosting sales at those catering to Halloween shoppers."

- There will be more detail on October sales out this Thursday with the Johnson Redbook Same-store Flash Report based on stores' reported sales for the month that are out that day. For now Johnson Redbook is targeting 6.2% Y/Y sales growth in November, noting " This month features several significant shopping promotions, including those around Election Day, Veterans Day, and Thanksgiving."

- Overall October retail data look to have been solid, between Redbook's figures and Chicago CARTS' preliminary estimate of ex-auto sales equivalent to a 4.3% Y/Y rise in ex-auto sales gains for a 2nd consecutive month (though of course we don't yet have official September data let alone October due to the federal government shutdown).