MNI ASIA OPEN: Warsh Fed Chair Nomination, Partial US Shutdown

EXECUTIVE SUMMARY

- MNI: Trump Names Kevin Warsh New Fed Chair

- MNI: Warsh Credible Pick, Must Earn FOMC Support: Ex-Officials

- MNI BRIEF: China Jan Manufacturing PMI Falls Below 50

- BBG: OPEC+ on Track to Ratify March Output Pause, Delegates Say

- GUARDIAN: US GOVERNMENT FUNDING LAPSES, TRIGGERING PARTIAL SHUTDOWN

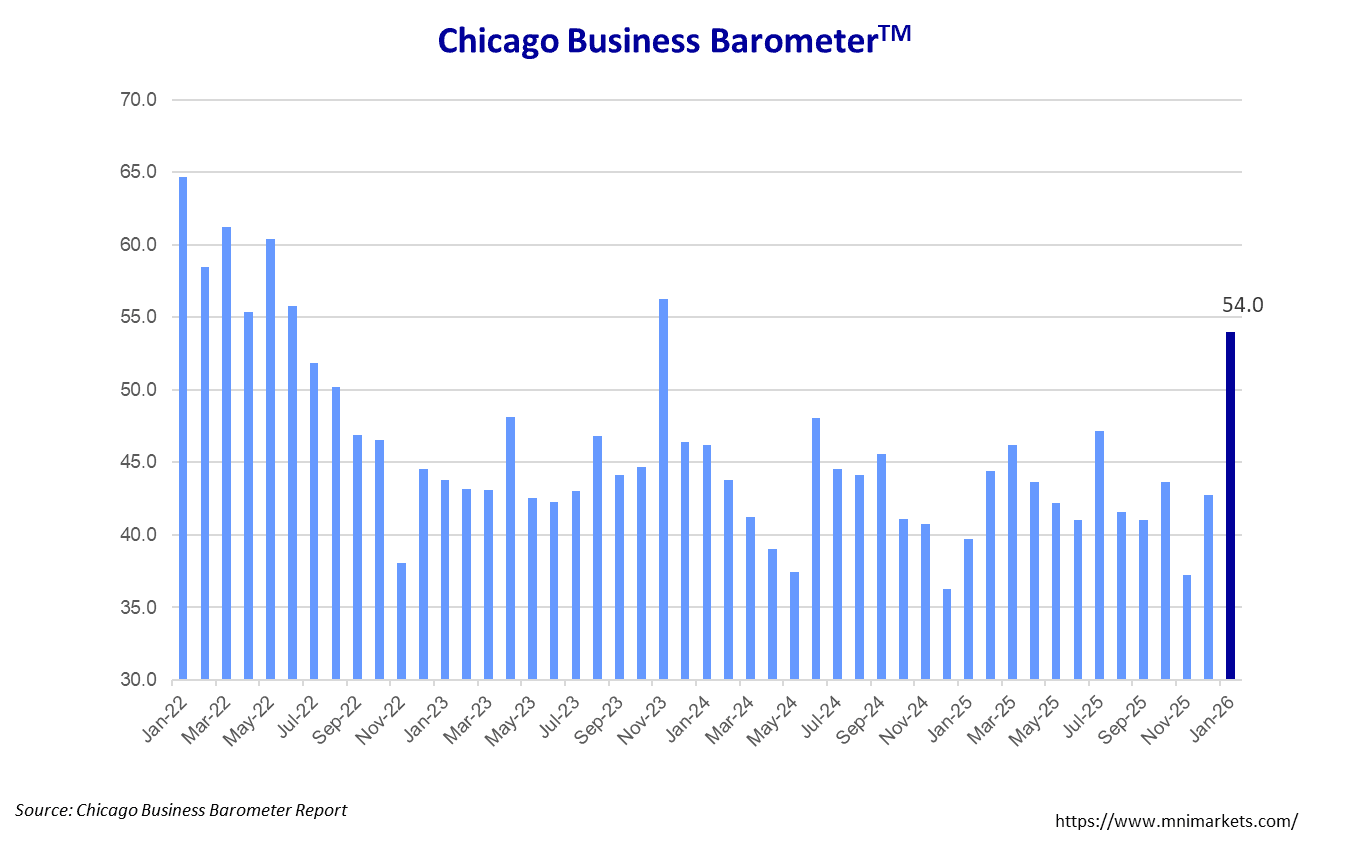

- MNI US DATA: Chicago Business Barometer™ - Jumped to 54.0 in January

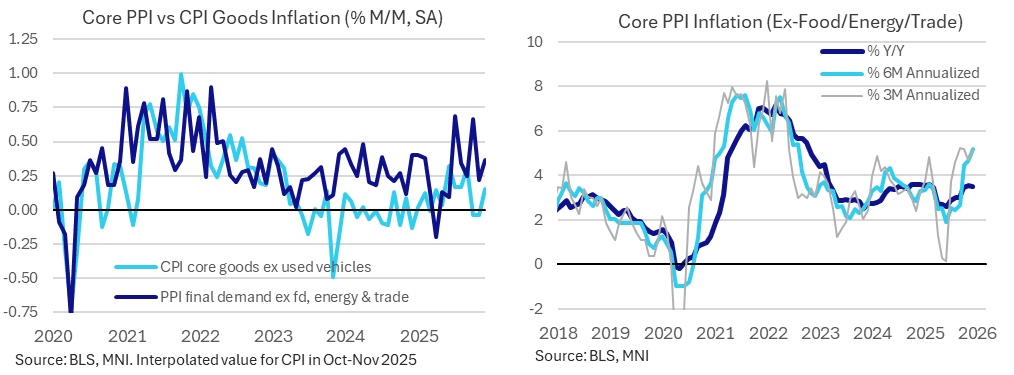

- MNI US DATA: Core PPI Inflation Trends Accelerate Further Into Year-End

US

MNI: Trump Names Kevin Warsh New Fed Chair

U.S. President Donald Trump said Friday he will appoint former Fed Governor Kevin Warsh to replace Jerome Powell as chair of the Federal Reserve when his term expires in May, capping off a year-long search that left financial markets on edge about a the risk of a loss of Fed independence.

MNI: Warsh Credible Pick, Must Earn FOMC Support: Ex-Officials

Former Fed officials Friday welcomed the nomination of Kevin Warsh as Federal Reserve Chair, telling MNI he is a seasoned central banker who knows the institution but he will need to work to persuade the FOMC on his policy ideas and earn the institution's trust as a leader.

MNI FED: St Louis's Musalem: "Unadvisable" To Cut Now

St Louis Fed's Musalem (not a 2026 FOMC voter but a hawkish-leaning member) on Friday echoed comments he made prior to the December meeting in suggesting that it would be "unadvisable" to cut rates at this time. That said, if the data were to align, then he is open to the possibility of cuts in future. Key quotes from his speech:

- He says he supported this week's decision to hold rates, and "given the current data and the balance of risks, I believe it would be unadvisable to lower the rate into accommodative territory at this time...I believe that policy is now well positioned to respond as needed to either of the Fed’s dual mandate objectives."

MNI FED: Gov Waller Eyes 50-75bp Cuts As Labor Market "Not Remotely Healthy"

Gov Waller explains his dissent at the January FOMC meeting in favor of a 25bp rate cut (link) by arguing "monetary policy is still restricting economic activity, and economic data make it clear to me further easing is needed". He calls for bringing the policy rate closer to neutral, "which the median FOMC participant estimates is 3 percent, and not where we are—50 to 75 basis points above 3 percent.". That's unchanged from his pre-FOMC stance though it was a bit of a surprise that he dissented at this meeting given he had sounded more patient in the lead-up (though the cynical view of many was that he was signalling to the White House that he would pursue easy policy if named Chair - a position which we now know is going to Kevin Warsh).

MNI FED: Gov Miran: A Lot Of Warsh's Views Are Really Right

Fed Gov Miran - who dissented against this week's rate hold in favor of a 25bp cut (smaller than the 50bp he called for at the prior 3 meetings) - continued to argue for easier policy in a CNBC appearance Friday. The post-blackout period Fedpseak has of course been overshadowed by the White House's nomination of Kevin Warsh as the next Fed Chair, and one of the big questions was whether Warsh would take Miran's seat on the Board. Miran tells CNBC that "I would assume" that Warsh will take his seat since it's "the only one available". "I guess we'll see when the President formally sends the nomination over to the Senate" but at present he expects to remain in the seat at least through the March FOMC meeting.

NEWS

MNI FED: Sen Tillis Repeats He Won't Support Board Nominees Until DOJ Probe Resolved

Republican Senator Tillis - who has said he'd block any Trump Fed nominees until the Powell/Fed DOJ investigation is resolved - has reiterated that position in a post on X.com.

- @SenThomTillis: "Kevin Warsh is a qualified nominee with a deep understanding of monetary policy. However, the Department of Justice continues to pursue a criminal investigation into Chairman Jerome Powell based on committee testimony that no reasonable person could construe as possessing criminal intent. Protecting the independence of the Federal Reserve from political interference or legal intimidation is non-negotiable. My position has not changed: I will oppose the confirmation of any Federal Reserve nominee, including for the position of Chairman, until the DOJ’s inquiry into Chairman Powell is fully and transparently resolved."

GUARDIAN: US GOVERNMENT FUNDING LAPSES, TRIGGERING PARTIAL SHUTDOWN - Funding lapsed for several US government departments on Saturday, the result of a standoff in Congress over new restrictions on federal agents involved in Donald Trump’s mass deportation campaign following the killings of two US citizens in Minneapolis.

BBG: Negotiations Over $100B OpenAI, Nvidia Deal Stall - WSJ - Nvidia's plan to invest up to $100 billion in OpenAI has stalled after some inside the chip giant expressed doubts about the deal.

BBG: TRUMP: PLEASED TO NOMINATE BRETT MATSUMOTO AS BLS COMMISSIONER

BBG: OPEC+ on Track to Ratify March Output Pause, Delegates Say - OPEC+ is on track to ratify its plans to pause production increases in March, delegates said ahead of the group’s online meeting on Sunday. Key members led by Saudi Arabia and Russia agreed back in November to halt a rapid revival of output during the first quarter, citing a seasonal slowdown in oil consumption.

US TSYS

MNI US TSYS: Rate Up With US$ Recovery on Fed Chair Nomination: Kevin Warsh

- Treasuries look to finish mixed, curves twisting steeper with 2s-5s outperforming weaker 10s-30s by the bell. Rather decent volumes (TYH6 over 2.1M) as markets price in Pres Trumps nomination for Fed Chairman: Kevin Warsh, with multiple Fed speakers fresh out of Blackout voicing their opinion on policy.

- TYH6 is currently -1 at 111-26.5 (111-17.5 low / 111-28 high), Initial firm resistance to watch is at the 20-day EMA, currently at 111-31+. The 50-day EMA is at 112-09. The area between the 20- and 50-day averages represents a key resistance zone.

- Fed Gov Miran initmated a lot of Warsh's views "are really right". Miran had dissented against this week's rate hold in favor of a 25bp cut (smaller than the 50bp he called for at the prior 3 meetings) - continued to argue for easier policy in a CNBC appearance Friday.

- St Louis Fed's Musalem (not a 2026 FOMC voter but a hawkish-leaning member) on Friday echoed comments he made prior to the December meeting in suggesting that it would be "unadvisable" to cut rates at this time. That said, if the data were to align, then he is open to the possibility of cuts in future.

- Warsh's nominated, not confirmed: Republican Senator Tillis - said he'd block any Trump Fed nominees until the Powell/Fed DOJ investigation is resolved - reiterated that position in a post on X.com: "Kevin Warsh is a qualified nominee with a deep understanding of monetary policy. However, I will oppose the confirmation of any Federal Reserve nominee, including for the position of Chairman, until the DOJ’s inquiry into Chairman Powell is fully and transparently resolved."

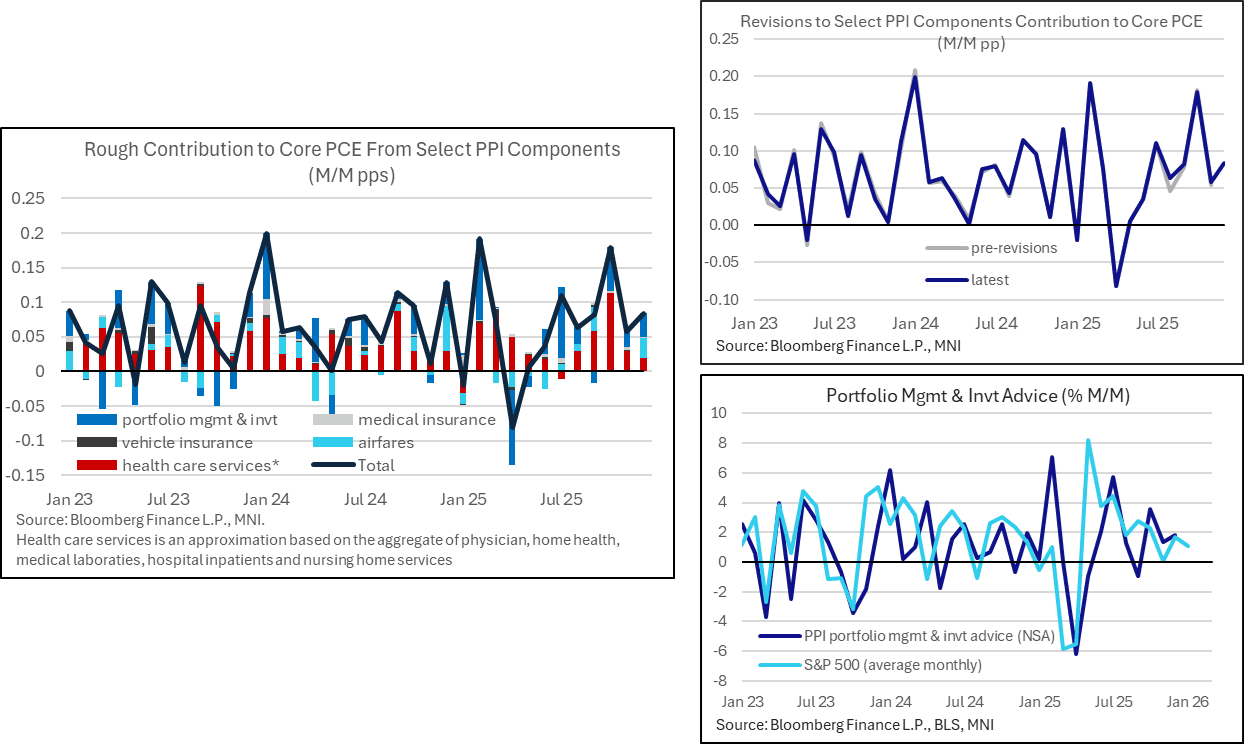

- PPI details offered a slightly stronger readthrough to core PCE inflation for December than was the case in November. Our best guess is that analysts will continue to expect core PCE inflation around 0.4% M/M in Dec after the 0.16% M/M in Nov (potentially revised up marginally).

- Cross-Asset update: Friday's broad rally in the US dollar (BBDXY +9.55 at 1187.45) prompted as extreme sell-off in metals prices, particularly precious metals which have plunged sharply: Spot gold fell to a low of $4,690/oz in recent trade, down more than $700 on the day, before bouncing slightly.

- Look ahead: US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed’s Powell and Warsh ahead. The employment report for January next Friday.

OVERNIGHT DATA

MNI BRIEF: China Jan Manufacturing PMI Falls Below 50

China's Manufacturing Purchasing Managers Index dropped by 0.8 points to 49.3 in January from December, falling below the breakeven 50 mark, mainly due to traditional off-season and insufficient demand, data from the National Bureau of Statistics showed on Saturday. The production sub-index declined by 1.1 points to 50.6, remaining in the expansionary zone. But new orders sub-index fell further into the contraction territory, by 1.6 points to 49.2.

- The non-manufacturing PMI registered 49.4, down 0.8 points from the previous month. The business activity sub-index for the service sector decreased by 0.2 points to 49.5, while that of the construction industry dropped 4.0 points to 48.8, as construction slowed due to low temperatures and the approaching Spring Festival holiday.

MNI US DATA: PPI Details Support Already Strong Core PCE Estimates For Dec

PPI details offered a slightly stronger readthrough to core PCE inflation for December than was the case in November. Our best guess is that analysts will continue to expect core PCE inflation around 0.4% M/M in Dec after the 0.16% M/M in Nov (potentially revised up ma ginally).

MNI US DATA: Core PPI Inflation Trends Accelerate Further Into Year-End

Core PPI was a little stronger than expected in December, building on recent strength to leave a Y/Y running at 3.50% and the last six months at 5.2% annualized for the strongest since mid-2022. Final demand PPI inflation was easily stronger than expected in December at 0.45% M/M (cons 0.2) after 0.24% M/M, but it was boosted by the volatile trade services category bouncing 1.7% M/M.

MNI US DATA: Chicago Business Barometer™ - Jumped to 54.0 in January

The Chicago Business Barometer™, produced with MNI, jumped 11.3 points to 54.0 in January. The index is in expansionary territory for the first time since November 2023, after twenty-five consecutive months below the key 50 mark. The rise was driven by increases in Employment, New Orders, Order Backlogs and Production. A decline in Supplier Deliveries provided a marginal offset.

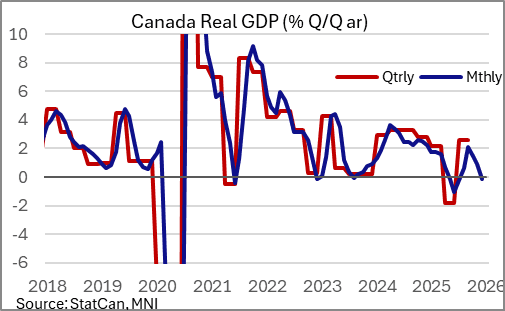

MNI CANADA DATA: Growth Momentum Stalled Badly In Q4

StatCan's November GDP by industry report underlined that activity in Q4 looks to have been flat at best, though likely contracted modestly. The 0.0% M/M November outturn was actually slightly contractionary (-0.02% unrounded) and lower than the advance estimate of 0.1% (albeit up from October's -0.3%), with goods-producing industries continuing to struggle with a 0.3% decline offset by a 0.1% rise in services.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 203.5 points (-0.41%) at 48868.45

S&P E-Mini Future down 37 points (-0.53%) at 6956.25

Nasdaq down 255.6 points (-1.1%) at 23431.44

US 10-Yr yield is up 1.2 bps at 4.2434%

US Mar 10-Yr futures are down 2/32 at 111-25.5

EURUSD down 0.0112 (-0.94%) at 1.1858

USDJPY up 1.53 (1%) at 154.65

WTI Crude Oil (front-month) up $0.36 (0.55%) at $65.78

Gold is down $498.46 (-9.27%) at $4876.91

European bourses closing levels:

EuroStoxx 50 up 55.86 points (0.95%) at 5947.81

FTSE 100 up 51.78 points (0.51%) at 10223.54

German DAX up 229.35 points (0.94%) at 24538.81

French CAC 40 up 55.17 points (0.68%) at 8126.53

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +1.836, 57.945 (L: 56.388 / H: 59.992)

2Y10Y +4.668, 71.488 (L: 67.411 / H: 71.499)

2Y30Y +5.824, 134.805 (L: 129.7 / H: 134.906)

5Y30Y +4.273, 107.814 (L: 104.046 / H: 107.885)

Current futures levels:

Mar 2-Yr futures up 1.375/32 at 104-7.875 (L: 104-04.875 / H: 104-08.125)

Mar 5-Yr futures up 1.25/32 at 108-29.5 (L: 108-22.75 / H: 108-30.5)

Mar 10-Yr futures down 2/32 at 111-25.5 (L: 111-17.5 / H: 111-28)

Mar 30-Yr futures down 5/32 at 115-2 (L: 114-12 / H: 115-06)

Mar Ultra futures down 15/32 at 117-10 (L: 116-21 / H: 117-24)

MNI US 10YR FUTURE TECHS: (H6) Bear Threat Remains Present

- RES 4: 112-31 High Dec 18 and key short-term resistance

- RES 3: 112-22 High Jan 7

- RES 2: 112-09 50-day EMA

- RES 1: 111-31+ 20-day EMA

- PRICE: 111-25 @ 1240 ET Jan 30

- SUP 1: 111-09 Low Jan 10 and the bear trigger

- SUP 2: 111-00 Round number support

- SUP 3: 110-30+ 1.618 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 110-22+ 1.764 proj of the Oct 17 - Nov 5 - 25 price swing

A bear threat in Treasuries remains intact and recent short-term gains still appear corrective. Initial firm resistance to watch is at the 20-day EMA, currently at 111-31+. The 50-day EMA is at 112-09. The area between the 20- and 50-day averages represents a key resistance zone. For bears, a resumption of weakness would refocus attention on the bear trigger at 111-09, the Jan 10 low. A break of this level resumes the downtrend.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 steady00 at 96.380

Jun 26 +0.020 at 96.570

Sep 26 +0.025 at 96.750

Dec 26 +0.030 at 96.820

Red Pack (Mar 27-Dec 27) +0.020 to +0.030

Green Pack (Mar 28-Dec 28) steadysteady0 to +0.015

Blue Pack (Mar 29-Dec 29) -0.01 to steady

Gold Pack (Mar 30-Dec 30) -0.025 to -0.015

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.65% (+0.01), volume: $3.166T

- Broad General Collateral Rate (BGCR): 3.63% (+0.01), volume: $1.324T

- Tri-Party General Collateral Rate (TCR): 3.63% (+0.01), volume: $1.294T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 3.63% (-0.01), volume: $187B

FED Reverse Repo Operation

RRP usage climbs to $9.629B with 8 counterparties this afternoon vs. $2.852B Thursday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

PIPELINE - No new issuance Friday after $40.75B priced on the week

- Date $MM Issuer (Priced *, Launch #)

- $23.75B Priced Thursday

- 01/29 $7B *Morgan Stanley $2.5B 4NC3 +60, $500M SOFR+77, $4B 11NC10 +85

- 01/29 $6.5B *AT&T $1.5B 5Y +60, $1.25B 7Y +75, $1.25B 10Y +90, $1.25B 20Y +105, $850M 30Y +115

- 01/29 $3.25B *IBM $500M 3Y +40, $500M 5Y +53, $500M 7Y +62.5, $1B 10Y +75, $750M 30Y +95

- 01/29 $3B *Capital One $1.5B 6NC5 +92, $1.5B 11NC10 +117

- 01/29 $3B *JP Morgan 11NC10 +97

- 01/29 $1B *CVR Energy $600M 5NC2 7.5%, $400M 8NC3 7.875%

MNI BONDS: EGBs-GILTS CASH CLOSE: Week Closes On A Mixed Note Ahead Of ECB, BOE

EGB and Gilt yields closed Friday little change, sealing Bund outperformance of Gilts for the week.

- Most of the session's price action was dictated by movements in US Treasuries as opposed to anything Europe-centric.

- Specifically, the White House naming Kevin Warsh as the nominee to lead the Federal Reserve triggered some bear steepening, the logic appearing to be: he is seen as less dovish on short rates than some of his competitors for the role, but he has long been vocal in calling for a smaller Fed balance sheet.

- That said, European data was on the hawkish side, with slightly firmer-than-expected Eurozone Q4 GDP (0.3%) and ECB inflation expectations, as well as an upside surprise in German and Spanish flash January inflation.

- The German curve leaned bear flatter on the day with the UK's bear steepening. Periphery/semi-core EGB spreads closed mixed but little changed overall.

- For the week the German curve bull flattened (2Y -4bp, 10Y -6bp), with Gilts twist steepening lightly (2Y -1bp, 10Y +1bp).

- S&P is scheduled to review Italy's sovereign rating after the cash close; an upgrade in the outlook to Positive is seen possible. Next week's calendar is packed, with the BOE and ECB decisions and the conclusion of the Eurozone January flash inflation round.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.6bps at 2.089%, 5-Yr is down 0.1bps at 2.417%, 10-Yr is up 0.3bps at 2.843%, and 30-Yr is up 0.5bps at 3.494%.

- UK: The 2-Yr yield is up 0.4bps at 3.718%, 5-Yr is up 0.4bps at 3.95%, 10-Yr is up 1.1bps at 4.522%, and 30-Yr is up 1.5bps at 5.285%.

- Italian BTP spread up 0.4bps at 61.3bps / French OAT down 0.3bps at 58.5bps

MNI FOREX: USD Recovers Amid Precious Metals Crash

- Despite some notable moves across the G10 on Friday, all the action was a bit of a sideshow compared to the aggressive moves seen in the precious metals space. Spot silver dropped as much as 36%, while gold followed suit by declining 12.75% at its worst point of the session. Headlines suggesting Iran want to make a deal, and the confirmation of Kevin Warsh as President trump’s nomination for the new Fed Chair have driven the dramatic corrections, providing a more constructive backdrop for the USD to recover.

- The USD index is trading around half a percent in the green as a result, with the late derisking leaving the Australian dollar as the worst performing currency in the G10. Declines for AUDUSD total around 1% and look set to end the consecutive winning streak for the pair, having reached as high as 0.7094 this week and trading around 0.6980 as we approach the weekend close. Profit taking dynamics may also be coming into play as we approach next week’s expected RBA hike.

- In similar vein, the likes of EURUSD and GBPUSD are roughly 0.7% lower on the session, while USDJPY has rallied back to 154.50. The removal of Fed Chair noise and intervention speculation may place the spotlight back on Japanese politics as we approach next month’s election. Indeed, the USDJPY recovery is also allowing an oversold position to unwind, with initial firm resistance intersecting at 155.80, the 50-day EMA.

- A 2.3% decline for the South African rand against the dollar is the best reflection of today’s turnaround/correction for precious metals. Today’s recovery has seen USDZAR completely erase the week’s selloff, with the 20-day EMA providing initial resistance around 16.20.

- US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed’s Powell and Warsh ahead.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 02/02/2026 | 0700/0800 | ** | Retail Sales | |

| 02/02/2026 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 02/02/2026 | 1145/1145 | BOE Breeden on Payments | ||

| 02/02/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/02/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/02/2026 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 03/02/2026 | 0030/1130 | * | Building Approvals | |

| 03/02/2026 | 0330/1430 | *** | RBA Rate Decision |