US DATA: Core PPI Inflation Trends Accelerate Further Into Year-End

Jan-30 13:46

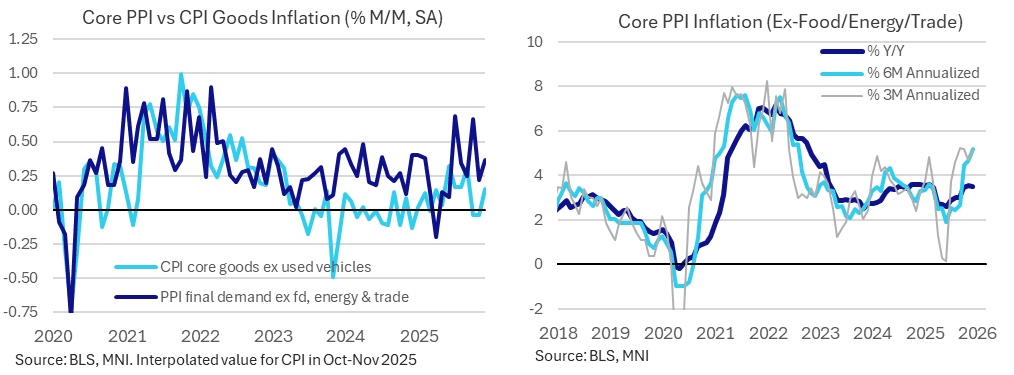

Core PPI was a little stronger than expected in December, building on recent strength to leave a Y/Y running at 3.50% and the last six months at 5.2% annualized for the strongest since mid-2022.

- Final demand PPI inflation was easily stronger than expected in December at 0.45% M/M (cons 0.2) after 0.24% M/M, but it was boosted by the volatile trade services category bouncing 1.7% M/M.

- We focus on PPI ex food, energy & trade services, which was also firmer than expected but by a lesser extent at 0.36% M/M (cons 0.3).

- This core CPI metric saw minimal revisions to prior months (a touch lower recently, with offsetting strength further back), leaving months oscillating between solid and strong readings including 0.22% M/M in Nov, 0.67% in Oct, 0.25% in Sep, 0.34% in Aug and 0.68% in Jul.

- It left core PPI inflation running at 3.50% Y/Y (cons 3.4) after a slightly upward revised 3.54% in Nov, with these latest two 3.5% months running at their highest since March.

- Recent trend rates point to further upward momentum in the Y/Y, with the six-month running at 5.2% annualized for its strongest since Aug 2022.

- Core goods CPI inflation has been more subdued recently, with the ex-used vehicles series firming to only 0.16% M/M in December after falling an average -0.04% M/M across Oct-Nov.

- Indeed, Fed Chair Powell said at the FOMC press conference that “a lot” of the tariff impact has already worked its way through the economy.

- However, as we noted the NY Fed’s GSCPI pointed to the highest global supply chain pressures in nearly three years in December at 0.5 standard deviations above average.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-Weekly Claims React

Dec-31 13:34

- Treasury futures extend lows after lower than expected weekly & continuing claims, the prior figure for continuing claims is reduced.

- Currently, TYH6 trades 112-16 (-4.5) vs. 112-15.5 low / 112-25.5 high.

- The trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection.

- Curves mixed: 2s10s at 67.256 +.107, 5s30s -.484 at 112.367.

- Bloomberg US$ index lower: BBDXY +.26 at 1203.39

MNI: US 27 DEC INITIAL JOBLESS CLAIMS 199K (215K 20 DEC)

Dec-31 13:30

- MNI: US 27 DEC INITIAL JOBLESS CLAIMS 199K (215K 20 DEC)

- US 20 DEC CONTINUING CLAIMS 1866K (1913K 13 DEC)

US TSYS: Where's the Beef? Treasuries Bid on Added China Tariff, Early NYE Close

Dec-31 11:55

- Treasuries holding firmer on light holiday volumes (TYH6 under 115k) - futures near top end of narrow range since the Asia cross-over to London trade - when yields dipped in reaction to additional tariffs on beef by China overnight: the US will have to pay 55% additional tariffs on beef exports to China, above its specified quota (164k tons a year in 2026).

- TYH6 trading 112-24 (+3.5) overnight high vs. 112-18 low, 10Y yld at 4.1083% (-.0136), curves mildly flatter with the Bonds outperforming: 2s10s -.966 at 66.183, 5s30s -.580 at 112.170.

- Trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection. Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Markets close early today for New Years eve (1300ET; 1600ET Globex), re-open/electronic trade Thursday evening for Friday's order of business. Today's shortened session sees Weekly Jobless Claims (0830ET). Followed by staggered US Treasury supply: 4W & 8W bills at 1000ET, 17W bills at 1130ET.