CANADA DATA: Growth Momentum Stalled Badly In Q4

Jan-30 16:06

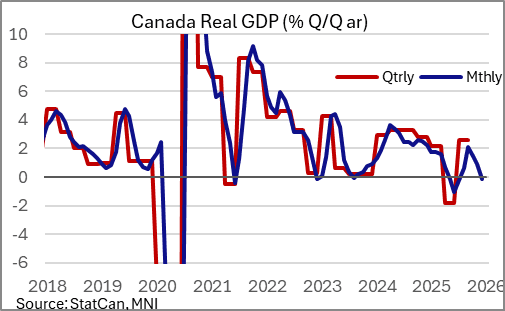

StatCan's November GDP by industry report underlined that activity in Q4 looks to have been flat at best, though likely contracted modestly.

- The 0.0% M/M November outturn was actually slightly contractionary (-0.02% unrounded) and lower than the advance estimate of 0.1% (albeit up from October's -0.3%), with goods-producing industries continuing to struggle with a 0.3% decline offset by a 0.1% rise in services.

- A 1.3% fall in manufacturing was attributed by StatCan to "supply chain bottlenecks" including a semiconductor shortage curtailing auto output but either way durable goods manufacturing is back to 2011 levels. (This is likely referring to a Honda plant in Ontario.)

- Retail trade rose 1.3%, rebounding partly due to the end of a labor disruption at liquor stores in British Columbia, with wholesale trade down 2.1%, the biggest drop since April, due in large part to auto sector difficulties.

- Elsewhere, agriculture/forestry/fishing/hunting fell 1.1%; transportation/warehousing rose 0.9%; and public sector activity rose 0.4% (again helped by the end of a work stoppage).

- December's advance estimate was little better at +0.1%, with " Increases in manufacturing and wholesale trade ... partially offset by decreases in mining, quarrying, and oil and gas extraction".

- These industry figures don't map perfectly with the overall quarterly GDP reading (which for Q4 is due out on Feb 27) but implies Q4 GDP pulled back sharply vs the 2.6% Q/Q SAAR in Q3 even though there was a very slight upward revision to October at -0.28% M/M vs -0.34% which helped offset the November miss.

- Mechanically GDP by industry points to a Q4 contraction of 0.5% Q/Q SAAR (-0.48% unrounded) which would be below the BOC's 0.0% estimate and 0.3% consensus but the actual GDP by expenditure reading can differ significantly from the industry data at times of volatile net trade (Q3 industry was +2.1% but actual was +2.6%). The latter is tracking positively for Q4 so the published contraction may not turn out to be quite as acute but clearly there has been little evident momentum in the activity data.

- That shouldn't be a game-changer for the BOC will still require some kind of shock to move off the sidelines on rates in the near future, but continued weak activity readings will reinforce markets' bias toward an easing being more likely than a tightening at least in the first half of 2025.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US EIA: CRUDE OIL STOCKS EX SPR -1.93M TO 422.9M IN DEC 26 WK

Dec-31 15:30

- US EIA: CRUDE OIL STOCKS EX SPR -1.93M TO 422.9M IN DEC 26 WK

- US EIA: DISTILLATE STOCKS +4.98M TO 123.7M IN DEC 26 WK

- US EIA: GASOLINE STOCKS +5.84M TO 234.3M IN DEC 26 WK

- US EIA: CUSHING STOCKS +0.54M TO 22.1M BARRELS IN DEC 26 WK

- US EIA: SPR +0.25M TO 413.2M BARRELS IN DEC 26 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +0.1% TO 94.7% IN DEC 26 WK

SOFR OPTIONS: Recent Midcurve Trade Leaning Bearish on Rates

Dec-31 15:11

- -10,000 0QF6 97.00/97.25 call spds, 2.25 vs. 96.885/0.22%

- +2,500 3QU6 95.50 puts, 5.0 ref 96.385

FED: US TSY 8W BILL AUCTION: HIGH 3.580%(ALLOT 64.96%)

Dec-31 15:02

- US TSY 8W BILL AUCTION: HIGH 3.580%(ALLOT 64.96%)

- US TSY 8W BILL AUCTION: DEALERS TAKE 33.66% OF COMPETITIVES

- US TSY 8W BILL AUCTION: DIRECTS TAKE 4.72% OF COMPETITIVES

- US TSY 8W BILL AUCTION: INDIRECTS TAKE 61.63% OF COMPETITIVES

- US TSY 8W BILL AUCTION: BID/CVR 2.83