BONDS: EGBs-GILTS CASH CLOSE: Week Closes On A Mixed Note Ahead Of ECB, BOE

Jan-30 18:28

EGB and Gilt yields closed Friday little change, sealing Bund outperformance of Gilts for the week.

- Most of the session's price action was dictated by movements in US Treasuries as opposed to anything Europe-centric.

- Specifically, the White House naming Kevin Warsh as the nominee to lead the Federal Reserve triggered some bear steepening, the logic appearing to be: he is seen as less dovish on short rates than some of his competitors for the role, but he has long been vocal in calling for a smaller Fed balance sheet.

- That said, European data was on the hawkish side, with slightly firmer-than-expected Eurozone Q4 GDP (0.3%) and ECB inflation expectations, as well as an upside surprise in German and Spanish flash January inflation.

- The German curve leaned bear flatter on the day with the UK's bear steepening. Periphery/semi-core EGB spreads closed mixed but little changed overall.

- For the week the German curve bull flattened (2Y -4bp, 10Y -6bp), with Gilts twist steepening lightly (2Y -1bp, 10Y +1bp).

- S&P is scheduled to review Italy's sovereign rating after the cash close; an upgrade in the outlook to Positive is seen possible. Next week's calendar is packed, with the BOE and ECB decisions and the conclusion of the Eurozone January flash inflation round.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.6bps at 2.089%, 5-Yr is down 0.1bps at 2.417%, 10-Yr is up 0.3bps at 2.843%, and 30-Yr is up 0.5bps at 3.494%.

- UK: The 2-Yr yield is up 0.4bps at 3.718%, 5-Yr is up 0.4bps at 3.95%, 10-Yr is up 1.1bps at 4.522%, and 30-Yr is up 1.5bps at 5.285%.

- Italian BTP spread up 0.4bps at 61.3bps / French OAT down 0.3bps at 58.5bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

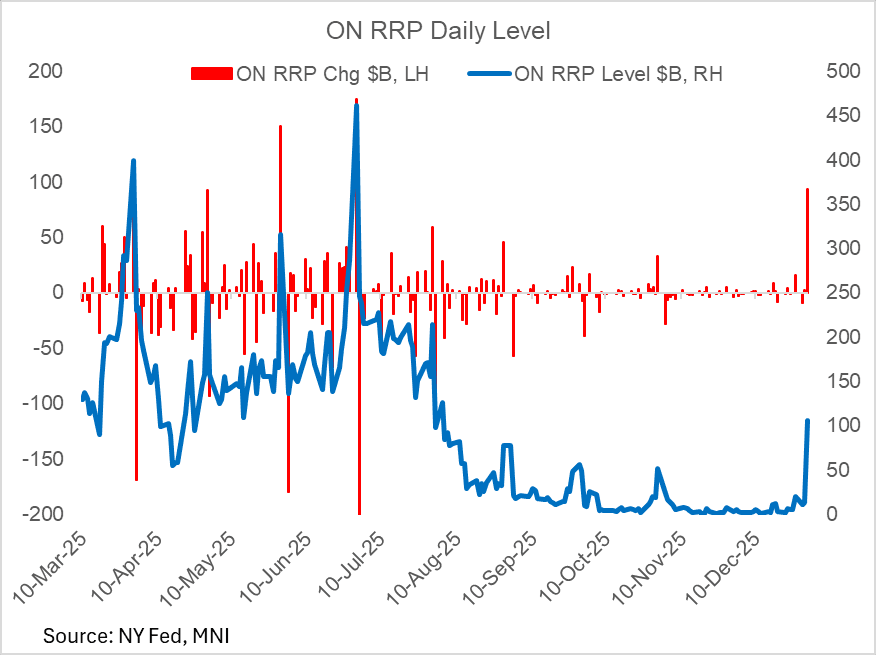

US TSYS/OVERNIGHT REPO: ON RRP Soars At Year-End, Well Below Prior Year's Level

Dec-31 18:22

Month-/quarter-/year-end brings a jump in Fed reverse repo takeup, to $106.0B. The $93B jump from the prior session is the biggest since May's $150B; the level is the highest since August.

- Of course, this is due to reverse sharply in coming sessions, and the takeup level is far below the $473B seen at year-end 2024.

US TSYS: Volume Jumps Into Year End

Dec-31 18:14

A 6+ tick dip in TYH6 accompanies the CME floor close for the New Year's holiday, to a session-low 112-10+ (a level last seen on Dec 24).

- After light volumes throughout the morning, a burst of around 400k contracts trade into the month end to a daily volume of 1.13M.

- Prices are stabilizing (last 112-12+), though as we noted earlier, from a technical perspective 111-29 would confirm a resumption of the bear cycle.

- SIFMA recommends a cash close at 2pm ET; Globex is open until 4pm ET.

US TSYS: Wrapping Up 2025

Dec-31 17:48

- Treasuries reversed early support after the final weekly claims data for 2025 came out lower than expected Wednesday, rather a decent range on moderate volumes ahead of the early close for the New Year's Eve holiday (1300ET; 1600ET Globex), re-open/electronic trade Thursday evening for Friday's order of business.

- TYH6 currently trades 112-17 (-3.5) vs. 112-14 low, curves mixed: 2s10s +.738 at 67.887, 5s30s -.890 at 111.961.

- The technical trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection. Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Treasury yields slipped overnight in reaction to additional tariffs on beef by China: the US will have to pay 55% additional tariffs on beef exports to China, above its specified quota (164k tons a year in 2026). 10Y yield tapped a low of 4.1024% before climbing to 4.1513% high following the jobless claims data.

- Initial jobless claims for the Dec 27 week were much lower than expected at 199k, vs the 218k consensus (215k prior rev from 214k). This marked the lowest level of seasonally-adjusted initial claims since the Nov 29 week, though it is for that reason that we suggest caution: both are holiday weeks (the other is Thanksgiving) which typically translates into volatility in claims.

- Meanwhile continuing claims for the Dec 20 week came in at 1,866k (1,902k consensus, 1,913k prior rev from 1,923k), marking a 3-week low but still in the recent ranges. NSA claims dropped 103k to 1,881k, and like initial, we would expect a large pickup the following week.