FED: Gov Miran: A Lot Of Warsh's Views Are Really Right

Fed Gov Miran - who dissented against this week's rate hold in favor of a 25bp cut (smaller than the 50bp he called for at the prior 3 meetings) - continued to argue for easier policy in a CNBC appearance Friday. The post-blackout period Fedpseak has of course been overshadowed by the White House's nomination of Kevin Warsh as the next Fed Chair, and one of the big questions was whether Warsh would take Miran's seat on the Board. Miran tells CNBC that "I would assume" that Warsh will take his seat since it's "the only one available". "I guess we'll see when the President formally sends the nomination over to the Senate" but at present he expects to remain in the seat at least through the March FOMC meeting.

- Miran praised the Warsh nomination and suggested that they were aligned on some monetary policy issues, saying "He's had a long history of convincing people about his arguments and so I think as a result, he's going to be treated with a lot of respect, and you know, I think people are going to find him very persuasive, because at the end of the day I think a lot of his views are really right."

- For example Miran says that he agrees with Warsh's view that the Fed balance sheet should be smaller, but "we've got to right size the regulations first" in order to lower the level of system reserves.

- Asked about whether he thinks Warsh will change the Fed's communications strategy, Miran says that the Fed should get rid of the projected policy rate dot in the Summary of Economic Projections. (Warsh has been critical of the Fed's current communications strategies.)

- In explaining his dovish dissent this week, Gov Miran repeats many of the same arguments he's made for several months, including that the PCE metric overestimates inflation ("Once you make these adjustments, you look at market based core ex-housing, it's running at 2.2% that's within noise of our target. So there is no inflation problem").

- He says that the gradual cooling trend in the labor market should be taken more seriously than the December unemployment rate downtick ("I don't understand why we'd be so quick to change our mind on the back of one data release... I think the unemployment rate is half a point too high or so, right? That's almost a million people who don't have jobs"), though he says he isn't as downbeat on the labor outlook as Miran's co-dissenter Gov Waller who said earlier that the jobs market "does not remotely look...healthy).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W BILL AUCTION: HIGH 3.540%(ALLOT 87.12%)

- US TSY 17W BILL AUCTION: HIGH 3.540%(ALLOT 87.12%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 30.92% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 4.63% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 64.46% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.11

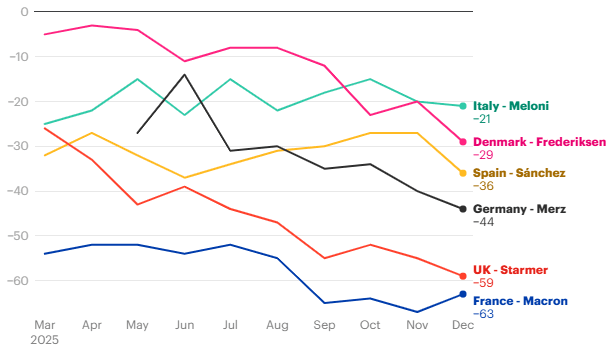

POLITICAL RISK: Meloni's Favourability On The Rise As Starmer & Merz Plummet

End-of-year favourability ratings from YouGov shows most major European heads of gov't/state struggling with negative public perceptions, although some have seen a more significant deterioration in the past year than others.

- Italian PM Giorgia Meloni's net favourability is the only leader to have seen her favourability improve over the year, finishing at -21 in December (the best among her peers), a marginal increase on the -25 recorded in March. The next general election is not due until December 2027 at the latest, but Meloni's relatively strong favourability at the midpoint of her term lends credence to the prospect of her being the first post-war Italian PM to serve out a full parliamentary term.

- At the other end of the scale are French President Emmanuel Macron and British PM Sir Keir Starmer, with net ratings of -63 and -59, respectively. While Macron, approaching the final full year of his second term, has recorded low favourability ratings all year, Starmer has seen his plummet from -26 in March amid rising public concerns about the state of the economy, prices, and immigration.

- Danish PM Mette Frederiksen's -29 net favourability is still strong by regional standards, but the decline from -3 in April could be a cause for concern with the next general election having to be held by 31 Oct at the latest.

- German Chancellor Friedrich Merz does not face any direct electoral challenge in 2026, but the decline in his favourability from -14 shortly after taking office in June, to -44 in Dec comes with parties of his governing 'grand coalition' facing challenges from the far-right Alternative for Germany in various state elections in 2026.

- Spanish PM Pedro Sanchez holds a net favourability of -36, a relatively robust rating as he enters his ninth year in office amid sexual misconduct and corruption scandals affecting his centre-left PSOE.

Chart 1. Favourability Rating: Do you have a favourable or unfavourable opinion of the following? [Leader of respondent country] Net favourability

Source: YouGov. Latest fieldwork 1-16 Dec.

US STOCKS: Weaker on Last Day of 2025 But Well Bid for the Year

Major equity indexes are weaker on the last trading day of 2025, yet not far from recent record highs: late October for SPX eminis (7,014.00) and Nasdaq (24,019.99), mid-December for the DJIA (48,886.86).

- Currently, the DJIA trades down 161.83 points (-0.33%) at 48206.14 (+13.28% YoY), S&P E-Mini Futures down 26.5 points (-0.38%) at 6917.75 (+16.84% YoY), Nasdaq down 81.4 points (-0.3%) at 23337.76 (+20.86% YoY).

- Energy and Consumer Discretionary sector shares led declines in late morning trade, oil and gas refiners weighing on the former: EQT Corp -2.31%, Valero Energy -1.84%, Expand Energy -1.66%, Coterra Energy -1.34% and Phillips 66 -1.15%.

- Underperforming Discretionary stocks included: Starbucks -1.20%, Williams-Sonoma -1.13%, Best Buy Co -1.00%, Carvana -0.86% and Domino's Pizza -0.86%.

- Limited advances were reported in Health Care and Financial sector shares, pharmaceuticals and managed care buoyed the former: Molina Healthcare +3.23%, Elevance Health +0.62%, Centene Corp +0.62% and Viatris +0.48%.

- Services related shared supported the Financials sector: Franklin Resources +0.46%, Erie Indemnity +0.28%, FactSet Research Systems +0.25% and Berkshire Hathaway +0.13%.