FED: St Louis's Musalem: "Unadvisable" To Cut Now

Jan-30 18:40

St Louis Fed's Musalem (not a 2026 FOMC voter but a hawkish-leaning member) on Friday echoed comments he made prior to the December meeting in suggesting that it would be "unadvisable" to cut rates at this time. That said, if the data were to align, then he is open to the possibility of cuts in future. Key quotes from his speech:

- He says he supported this week's decision to hold rates, and "given the current data and the balance of risks, I believe it would be unadvisable to lower the rate into accommodative territory at this time...I believe that policy is now well positioned to respond as needed to either of the Fed’s dual mandate objectives."

- But he appears to retain an easing bias: "I could support additional reductions in the policy rate if new evidence of labor market weakness or risks emerge, absent further signs of persistent above-target inflation or rising inflation expectations. I could also support lowering the nominal policy rate if expected inflation declines to target or falls below it."

- He notes that "Recent data indicate the labor market is regaining some of its footing" and his view is that "Although hiring remains soft, continued above trend economic growth should support the demand for labor while low levels of immigration limit growth in labor supply." Conversely he says inflation "has been stubborn" and , "but I expect inflation will resume a path toward 2% as tariff effects ebb later this year."

- He's upbeat on economic activity: "I expect the economy will continue to expand at or above its long-run trend rate in 2026...Reports indicate that consumer spending was especially strong in late December and into January...Supportive financial conditions are among [] tailwinds...changes in tax law and various forms of deregulation could also lift spending...Productivity growth is another potential tailwind" with his only real reservation being on the housing market which "has been weak for several quarters and poses some downside risk".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

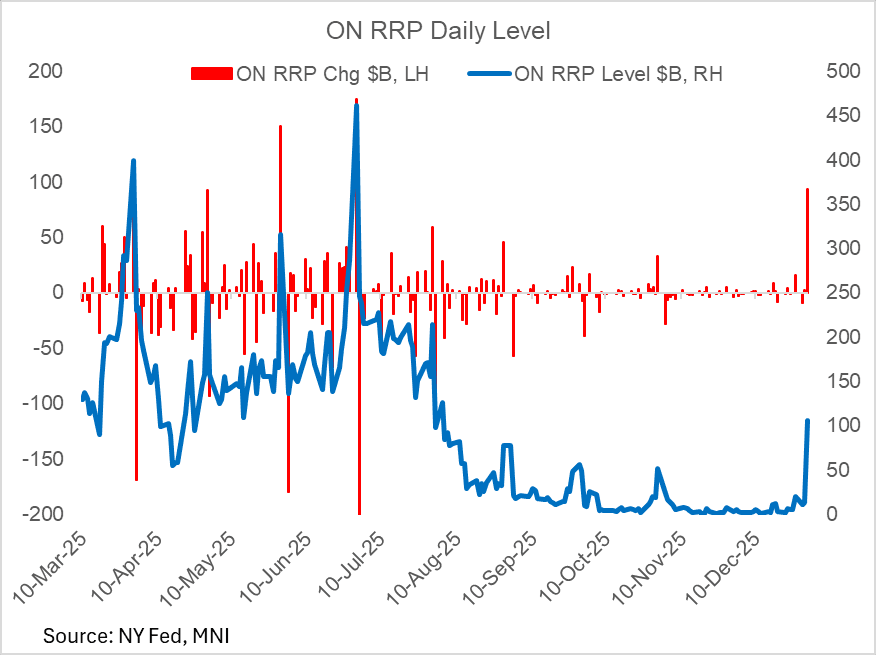

US TSYS/OVERNIGHT REPO: ON RRP Soars At Year-End, Well Below Prior Year's Level

Dec-31 18:22

Month-/quarter-/year-end brings a jump in Fed reverse repo takeup, to $106.0B. The $93B jump from the prior session is the biggest since May's $150B; the level is the highest since August.

- Of course, this is due to reverse sharply in coming sessions, and the takeup level is far below the $473B seen at year-end 2024.

US TSYS: Volume Jumps Into Year End

Dec-31 18:14

A 6+ tick dip in TYH6 accompanies the CME floor close for the New Year's holiday, to a session-low 112-10+ (a level last seen on Dec 24).

- After light volumes throughout the morning, a burst of around 400k contracts trade into the month end to a daily volume of 1.13M.

- Prices are stabilizing (last 112-12+), though as we noted earlier, from a technical perspective 111-29 would confirm a resumption of the bear cycle.

- SIFMA recommends a cash close at 2pm ET; Globex is open until 4pm ET.

US TSYS: Wrapping Up 2025

Dec-31 17:48

- Treasuries reversed early support after the final weekly claims data for 2025 came out lower than expected Wednesday, rather a decent range on moderate volumes ahead of the early close for the New Year's Eve holiday (1300ET; 1600ET Globex), re-open/electronic trade Thursday evening for Friday's order of business.

- TYH6 currently trades 112-17 (-3.5) vs. 112-14 low, curves mixed: 2s10s +.738 at 67.887, 5s30s -.890 at 111.961.

- The technical trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection. Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Treasury yields slipped overnight in reaction to additional tariffs on beef by China: the US will have to pay 55% additional tariffs on beef exports to China, above its specified quota (164k tons a year in 2026). 10Y yield tapped a low of 4.1024% before climbing to 4.1513% high following the jobless claims data.

- Initial jobless claims for the Dec 27 week were much lower than expected at 199k, vs the 218k consensus (215k prior rev from 214k). This marked the lowest level of seasonally-adjusted initial claims since the Nov 29 week, though it is for that reason that we suggest caution: both are holiday weeks (the other is Thanksgiving) which typically translates into volatility in claims.

- Meanwhile continuing claims for the Dec 20 week came in at 1,866k (1,902k consensus, 1,913k prior rev from 1,923k), marking a 3-week low but still in the recent ranges. NSA claims dropped 103k to 1,881k, and like initial, we would expect a large pickup the following week.