MNI ASIA OPEN: Tariff Uncertainty Enters The Courtroom

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- Trump Wins Tariff Reprieve as Trade Agenda Faces Court Rollback (BBG)

- FED: Trump Tells Powell He Is Making A "Mistake" Not Cutting Rates

- MNI POLICY: Fed Cut Impetus Fades Alongside Recession Fears

- MNI INTERVIEW: Banxico To Cut 50BP If Inflation Allows -Guzman

- US DATA: Consumption Downward Revision In Q1 GDP Offset By Inventories

NEWS

TARIFFS (BLOOMBERG): Trump Wins Tariff Reprieve as Trade Agenda Faces Court Rollback (BBG)

A federal appeals court offered President Donald Trump a temporary reprieve from a ruling threatening to throw out the bulk of his sweeping tariff agenda, offering at least some hope to a White House now facing substantial new restrictions on its effort to rewrite the global trading order. The administration celebrated the order from the US Court of Appeals for the Federal Circuit as validating its vow to aggressively challenge a ruling issued Wednesday night by the Court of International Trade blocking sweeping parts of Trump’s tariffs over his use of the International Emergency Economic Powers Act, or IEEPA.

FED: MNI BRIEF: Powell Tells Trump Rate Decisions To Be Data-Based

Federal Reserve Chair Jerome Powell told U.S. President Donald Trump in a meeting Wednesday that monetary policy decisions will be based on "non-political analysis," the central bank said in a statement. “At the President’s invitation, Chair Powell met with the President today at the White House to discuss economic developments including for growth, employment, and inflation,” the statement said. “Chair Powell did not discuss his expectations for monetary policy, except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook.”

FED (MNI): 2025 Rate Cut Pricing At Session Highs After Trump Eyes Powell "Mistake"

White House Press Secretary Leavitt said that in today's meeting with Fed Chair Powell, President Trump said that he believes Powell is making a "mistake" in policy: "The president did say that he believes the Fed Chair is making a mistake by not lowering interest rates, which is putting us at an economic disadvantage to China and other countries. And the president's been very vocal about that, both publicly and now I can reveal privately as well."

FED: MNI POLICY: Fed Cut Impetus Fades Alongside Recession Fears

Worries that the worst-case scenario for tariffs would lead to a sudden stop in U.S. economic growth are gradually fading, further reducing the case for the Federal Reserve to cut interest rates this year as uncertainty about the inflationary effects of volatile trade policies remains high. FOMC members have said repeatedly that monetary policy is well-positioned to react to risks of either more persistent inflation or slower-than-expected growth. Their wait-and-see attitude is being reinforced by the on-again off-again nature of President Donald Trump's tariffs strategy, evidenced by the major blow Wednesday when the U.S. Court of International Trade blocked Trump's actions to impose reciprocal and fentanyl-related tariffs using the International Emergency Economic Powers Act.

MEXICO: MNI INTERVIEW: Banxico To Cut 50BP If Inflation Allows -Guzman

The Central Bank of Mexico intends to cut its interest rate by 50 basis points to 8.00% in June, though this will depend on inflation developments as its forward guidance does not represent a firm commitment, former Banxico Deputy Governor Javier Guzman told MNI. "The message they’re sending is that they intend to cut by the same magnitude, by 50 basis points. In terms of their current intention, there’s no doubt," Guzman said in an interview.

MEXICO: MNI BRIEF - All Banxico Members Highlighted US Risks - Minutes

All members of the Central Bank of Mexico’s board highlighted economic perils linked to deepening uncertainty surrounding U.S. trade policy, according to the minutes of the latest policy meeting released Thursday. Most members mentioned that the interest rate differential with the U.S. has remained high. The board reiterated that it may continue to calibrate the monetary policy stance and consider adjusting borrowing costs “in similar magnitudes.”

EUROZONE: MNI Eurozone May HICP Preview: Unwinding of Easter Effect Key

Tariff developments remain the centre of market attention, but the Eurozone May flash inflation round will still be in focus to determine to what extent the April acceleration in services inflation was temporary. The details of the April reading pointed to a substantial “Easter effect” for travel-sensitive services such as airfares, and already released French and Belgian data point to an unwind of these dynamics.

US TSYS: Belly Outperforms Amid Legal Wrangling Over Tariffs

Treasuries reversed early weakness to finish stronger Thursday, with the belly outperforming on the curve.

- Treasuries were on the back foot early as risk assets gained following late Wednesday's court ruling that blocked implementation of most of the White House's tariffs.

- But the initial reaction faded as markets assessed whether the legal decision would have a lasting effect, and indeed, in late afternoon trade an appeals court allowed the tariffs to remain in effect at least temporarily.

- Equities faded from their highs, with Treasuries getting a boost from soft data in the form of downward revisions to Q1 consumption in GDP, and surprisingly weak jobless claims data. Month-end dynamics may have played a factor as well.

- There was a small but notable downtick in short-end rates after the White House said President Trump told Powell in a private meeting today that the Fed Chair was making a "mistake" by not cutting rates.

- The bond rally extended in the afternoon after the third strong Treasury auction of the week, with 7Y Note seeing the joint-highest trade-through since August 2022 (2.9bp), and record-low primary dealer takedown.

- Partly as a result, the curve belly outperformed on the day (7Y yields dropped 5.8bp). Latest levels: The 2-Yr yield is down 4.7bps at 3.9427%, 5-Yr is down 5.7bps at 4.0052%, 10-Yr is down 4.9bps at 4.4279%, and 30-Yr is down 5.1bps at 4.9244%.

- Sep US 10Y futures (TY) up 12.5/32 at 110-20.5 (L: 109-26 / H: 110-23.5), briefly testing key near-term resistance at 110-23, the May 16 high.

- Friday's calendar is busy data-wise: we get the April PCE report, April trade data, MNI Chicago PMI, and May's final UMichigan consumer survey.

OVERNIGHT DATA

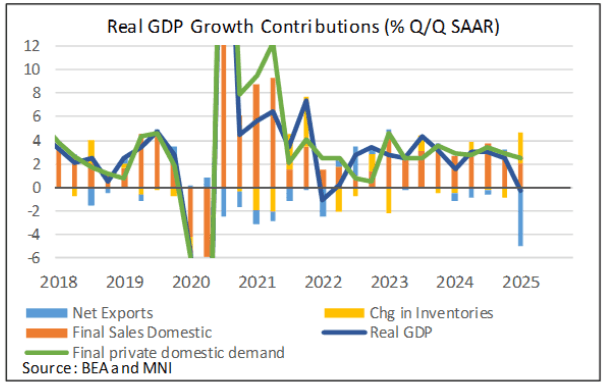

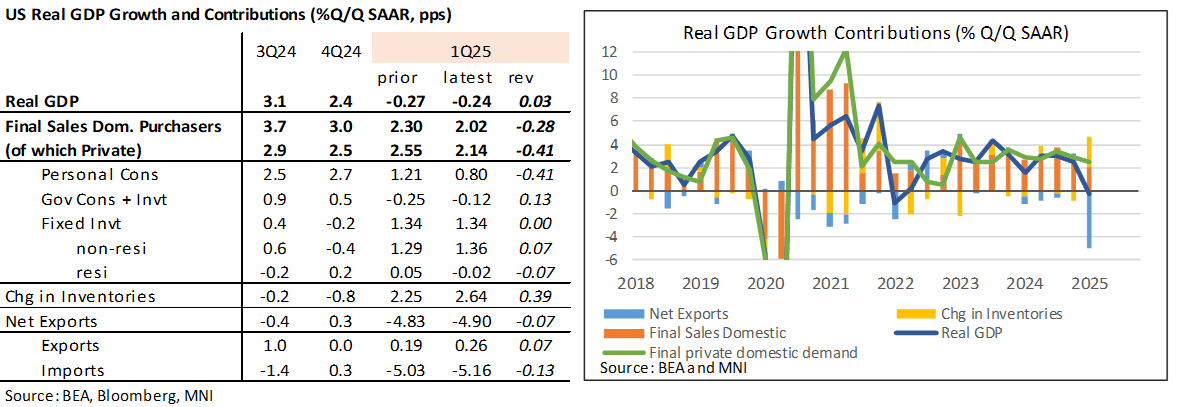

US DATA: Consumption Downward Revision In Q1 Offset By Inventories

• Real GDP growth was revised up fractionally to -0.24% annualized in the second Q1 release (cons -0.3) from the -0.27% in last month’s advance.

• The softer consumption figure was most notable, lowered to 1.2 % annualized (cons 1.7, advance 1.8).

• It dragged 0.4pp from GDP growth, offset by an even stronger boost from changes in inventories.

• See the contribution changes in the table below.

• Core PCE inflation meanwhile was revised lower from 3.46% to 3.41% (cons 3.5).

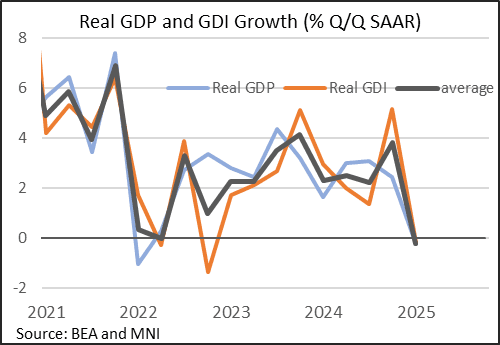

US DATA: GDI Contracts In Tandem With GDP As Corporate Profits Pull Back

Real Gross Domestic Income contracted 0.2% Q/Q SAAR in Q1, per data made available in the 2nd national accounts release for the quarter. That's the weakest in 9 quarters, and a sharp reversal from Q4's 12-quarter best 5.2%.

- This was - unusually - exactly in line with the GDP reading of -0.2%, meaning the average of the two was likewise -0.2% - with the exception of the start of the Covid pandemic in 2020, this was the first negative reading since June 2016, and was a sharp reversal from +3.8% in Q4 (4-quarter high).

- As such it appears to suggest broader economic weakness in Q1 that can't just be attributed to weaker net exports.

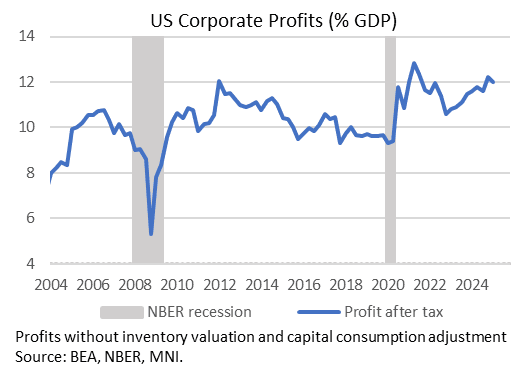

- Nominal corporate profits (with inventory valuation and capital consumption adjustments) fell 2.95% Q/Q SAAR, vs +5.4% prior, meaning that while profits are still higher than in Q3 2024, the Q4 gains were pared sharply.

- Overall though they are still very elevated (up 5.5% Y/Y and at 13% of GDP, vs 13.5% in Q4), with only modest profit margin compression in the quarter.

- Whether that remains the case going forward with tariffs will be worth watching, for the degree to which firms absorb tariff costs.

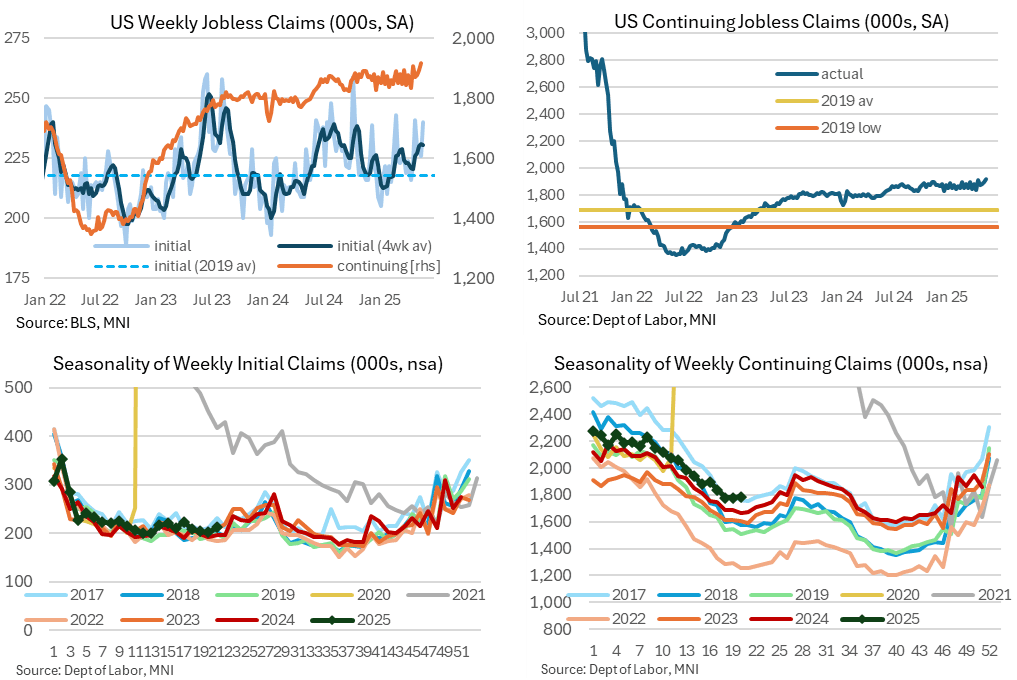

US DATA: A Fresh 3+ Year High For Continuing Claims

Latest weekly jobless claims data extend last week’s first signs of a renewed deterioration in the labor market, and with little sign of a particular distortion. The more notable finding in our view was a push higher in continuing claims to a fresh high since late 2021, suggesting rehiring conditions have recently become harder, but increases are still on the measured side for now.

- Initial jobless claims were higher than expected at 240k (sa, cons 230k) in the week to May 24 after a downward revised 226k (initial 227k).

- The four-week moving average was unchanged at 231k, as the latest print only offset the 241k spike in the last full week of April owing to the later timing of Easter this year. It remains at its highest since late October, a little above the 218k averaged in 2019 for context.

- The non-seasonally adjusted data for the time of year are higher than 2024 and 2022 but still within recent ranges for ‘normal’ years – see below charts.

- We can’t see much of note within the non-seasonally adjusted state details - Michigan led the increase with a 3.3k rise to 8.6k but that’s not unprecedented.

- Continuing claims surprisingly increased to 1919k (sa, cons 1893k) in the week to May 17, capturing a payrolls reference period, after a downward revised 1893k (initial 1903k).

- It marks a new high since late 2021, back above the 1900k mark that was first pierced in the week to Apr 19.

- It will be revised again next week but for now, the 1919k is a marked increase from the 1833k in last month’s payrolls reference period along with two months at 1847k before that.

- The below NSA charts show a continued upward drift relative to recent non-pandemic years, putting claims above recent ranges – see charts.

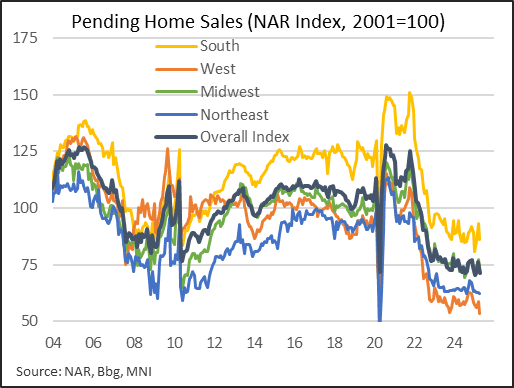

US DATA: Rebound In Mortgage Rates Crushes Pending Home Sales

Pending home sales fell sharply in April, with the National Association of Realtors' index at 71.3 (vs 76.1 prior). The 6.3% M/M drop was the biggest in 31 months to a 3-month low, reversing a jump in March and weaker than expectations for a -1.0% fall.

- This was the 2nd lowest reading in series history back to 2001 (only Jan 2025 was lower).

- Contractions were seen across each of the 4 major regions, with pending sales in the West at an all-time low (in series history).

- Only the Midwest region saw higher Y/Y pending sales, which the NAR report noted is suggestive of the fact that national housing affordability is so poor that the relatively low-priced real estate there makes the Midwest attractive.

- In turn, it's clear that the spike back up in mortgage rates in April amid tariff and market turmoil triggered buyer retrenchment. 30Y fixed rates jumped to 6.9% in April, from 6.7% (4-month low) in March.

- From the release: "At this critical stage of the housing market, it is all about mortgage rates," said NAR Chief Economist Lawrence Yun. "Despite an increase in housing inventory, we are not seeing higher home sales. Lower mortgage rates are essential to bring home buyers back into the housing market."

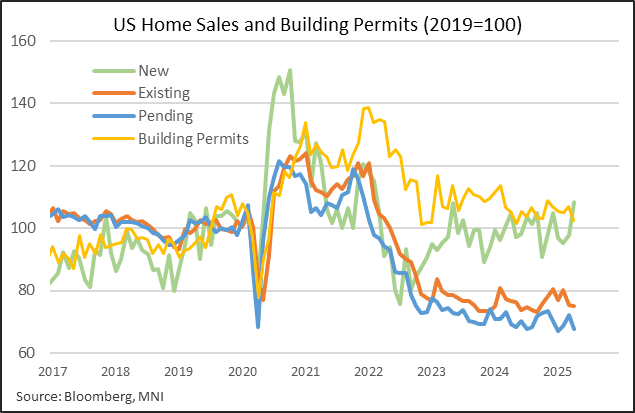

- This does not bode well for future existing home sales (for which pending sales are a leading indicator). However new home sales and building permits have held up, suggesting that there is greater mobility in new homes, particularly as they do not require an existing homeowner - who is locked into a low mortgage rate - to move.

- As such while the residential real estate market is in deepening stasis, new construction doesn't look like it is necessarily going to weaken sharply.

CANADA DATA: March Payroll Employment Declines For 2nd Straight Month

- March payroll employment -54.1K or -0.3% after -40.2K in Feb.

- Ten sectors recorded declines, seven were little changed and three posted gains. The headline drop in jobs was led by educational services, healthcare and finance while mining and oil gains partially offset the decrease.

- Payroll jobs in retail trade continued its downward trend which began in Feb 2023 while wholesale trade fell for the fourth consecutive month.

- Previously released and more timely labour force survey data showed employment -33K in March and +7.4K in April.

- YOY employment +32.8K or +0.2% in March, StatsCan said Thursday.

- Average weekly earnings +4.3% YOY in March, significantly higher than BOC's 2% inflation target, but less than prior 5.1%.

CANADA DATA: Canada Has 11th Consecutive Current Account Deficit

- Canada's current account deficit narrowed to CAD2.1B in Q1 after CAD3.6B in Q4. Deficit has narrowed from CAD5.3b in Q2 2024.

- Tariff threats drove up imports and exports of goods, but the overall balance was little changed at -CAD0.5b, StatsCan said Thurs. Services deficit was also little changed at -CAD0.9b.

- That meant the deficit narrowed on the income account. StatsCan said that was led by transfers, followed by higher profits on Canada's foreign direct investments abroad.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

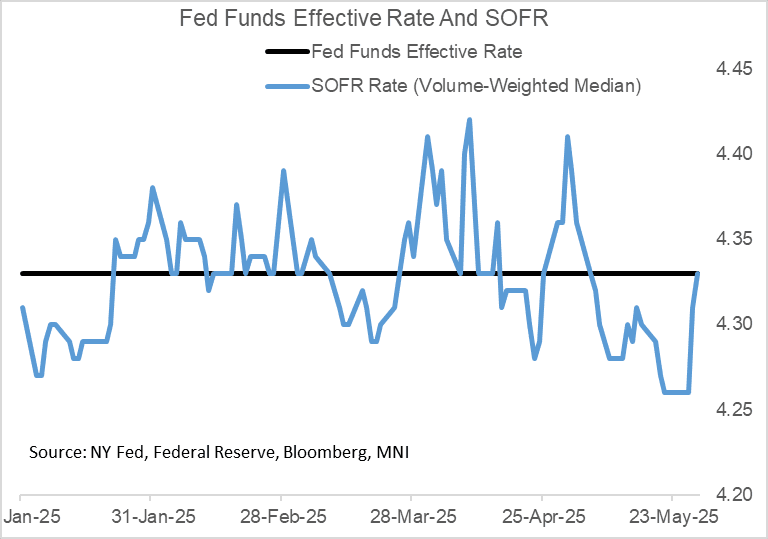

US TSYS/OVERNIGHT REPO: Secured Rates Continue To Tick Up With Month-End Ahead

Secured rates rose for a 2nd consecutive session Wednesday, with SOFR up 2bp to 4.33%, adding to the 5bp rise prior.

- That brings SOFR back up to the level of effective Fed funds for the first time since May 5.

- Secured rates rates could be temporarily subdued today by $29B in net Treasury bill paydowns. However, upside pressures are likely to persist toward week-end exacerbated by Friday's month-end dynamics and $46B in Treasury net new cash raised via coupon auction settlements.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.33%, 0.02%, $2605B

* Broad General Collateral Rate (BGCR): 4.32%, 0.02%, $1049B

* Tri-Party General Collateral Rate (TGCR): 4.32%, 0.02%, $1020B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $108B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $282B

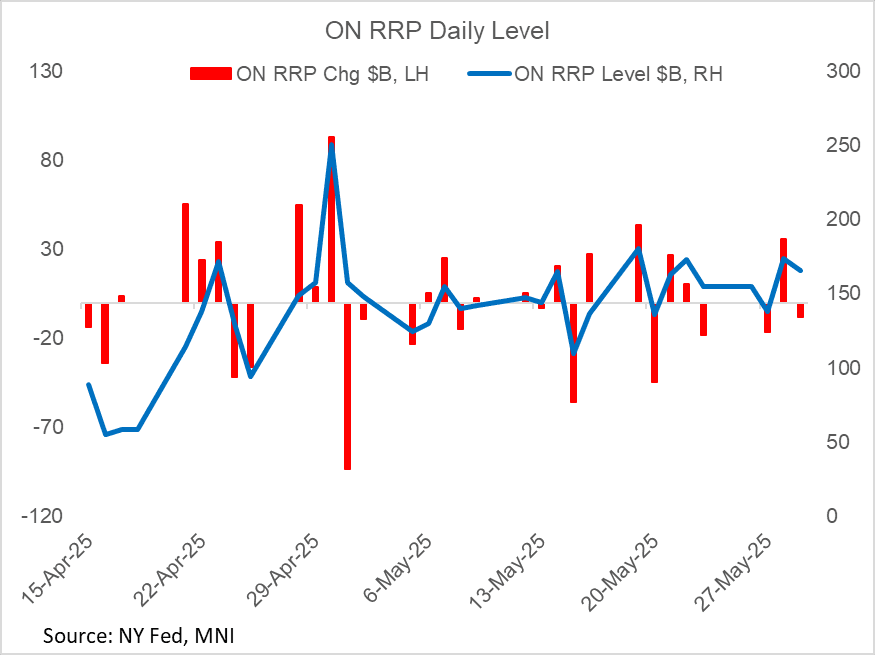

US TSYS/OVERNIGHT REPO: Overnight Reverse Repo Takeup Pared, May Rebound Friday

Overnight reverse repo (ON RRP) takeup dipped $8.0B to $165.7B Thursday. Even so, it remains elevated, with Wednesday's total having been the 2nd highest total of the month.

- As we noted following yesterday's $36B jump, ON RRP takeup isn't expected to rise much more (ie remaining below $200B), with the likely exception of month-end dynamics Friday.

EGBs-GILTS CASH CLOSE: Rallying Into Month-End

European core FI recovered from early weakness to close stronger Thursday.

- Core instruments were under some pressure in an early risk-on move, after a surprise US court decision overnight striking down (at least temporarily) the bulk of the White House's previously-announced tariffs.

- But Bunds and Gilts rallied almost continuously throughout the rest of the session.

- Multiple factors drove the rally: softer-than-expected US GDP and jobless claims data in the early European afternoon; softening equities as the impact of the US tariff court order was reconsidered; and, potentially, month-end dynamics helping boost core instruments led by Treasuries.

- UK yields fell around 8bp across the curve, outperforming bull flattening German instruments.

- Periphery / semi-core EGBs traded mixed but basically flat on the day vs Bunds; OATs outperformed.

- Friday brings flash May inflation data from Spain, Italy and Germany - MNI’s preview is here. We also hear from ECB's Muller, Panetta and Vujcic.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.8bps at 1.769%, 5-Yr is down 3.9bps at 2.068%, 10-Yr is down 4.6bps at 2.508%, and 30-Yr is down 4.4bps at 2.987%.

- UK: The 2-Yr yield is down 8bps at 3.995%, 5-Yr is down 7.8bps at 4.128%, 10-Yr is down 7.9bps at 4.648%, and 30-Yr is down 8.4bps at 5.396%.

- Italian BTP spread unchanged at 98.1bps /French down 0.6bps at 66.7bps

FOREX: US Dollar Reverses Steadily Lower, EURUSD Re-Approaches 1.14

- Following the greenback’s powerful gap higher on the overnight news that the US trade court ruling against Trump’s tariffs, the dollar has since reversed steadily lower across Thursday’s trading session, and the USD index is currently 0.6% lower as we approach the APAC crossover.

- Outperforming in G10 has been the Euro, with EURUSD hugging the day’s highs at typing and re-approaching the 1.14 handle, despite registering earlier lows at 1.1210. On the upside, a break of 1.1419, the May 26 high, would be a bullish development and bolster the underlying trend for the pair.

- EURGBP prices reversed higher Thursday, bouncing sharply off a fresh pullback low. Despite the phase of strength, the cross is still yet to meaningfully challenge the next resistance: the 50-day EMA at 0.8444. Clearance here opens potential for a stronger reversal toward 0.8541.

- USDJPY has been grinding lower, with the reversal lower for major equity benchmarks adding specific weight to the pair. Spot has slipped back below 144.00 in late US trade, having reversed ~230 pips from the APAC highs at 146.28. The initial rally resulted in a breach of the 50-day EMA, at 145.64, however the failure to close above opens scope for near-term weakness. Support to watch is 142.12, the May 27 low. A break would resume the recent bear leg.

- In emerging markets, the South African rand has traded to a fresh 5-month high, as a 25bp rate cut from the SARB was easily shrugged off. SARB Governor Kganyago said a lower inflation target would lead to structurally lower interest rates as the economy recalibrates to a lower-inflation, higher-growth environment. Support is seen at 17.6191, the December low.

- Focus Friday turns to the US Core PCE Report for April. Elsewhere, German & Spanish CPI and Canada GDP are also scheduled.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/05/2025 | 0600/0800 | *** | GDP | |

| 30/05/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/05/2025 | 0600/0800 | ** | Retail Sales | |

| 30/05/2025 | 0630/0730 | DMO to release FQ2 (Jul-Sep) issuance ops calendar | ||

| 30/05/2025 | 0700/0900 | *** | HICP (p) | |

| 30/05/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/05/2025 | 0800/1000 | ** | M3 | |

| 30/05/2025 | 0800/1000 | *** | GDP (f) | |

| 30/05/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/05/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/05/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/05/2025 | 0900/1100 | *** | HICP (p) | |

| 30/05/2025 | 1000/1200 | ** | PPI | |

| 30/05/2025 | 1200/1400 | *** | HICP (p) | |

| 30/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/05/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 30/05/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 30/05/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 30/05/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/05/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 30/05/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 30/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 30/05/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 2045/1645 | San Francisco Fed's Mary Daly | ||

| 31/05/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/05/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI |