US DATA: A Fresh 3+ Year High For Continuing Claims

May-29 12:57

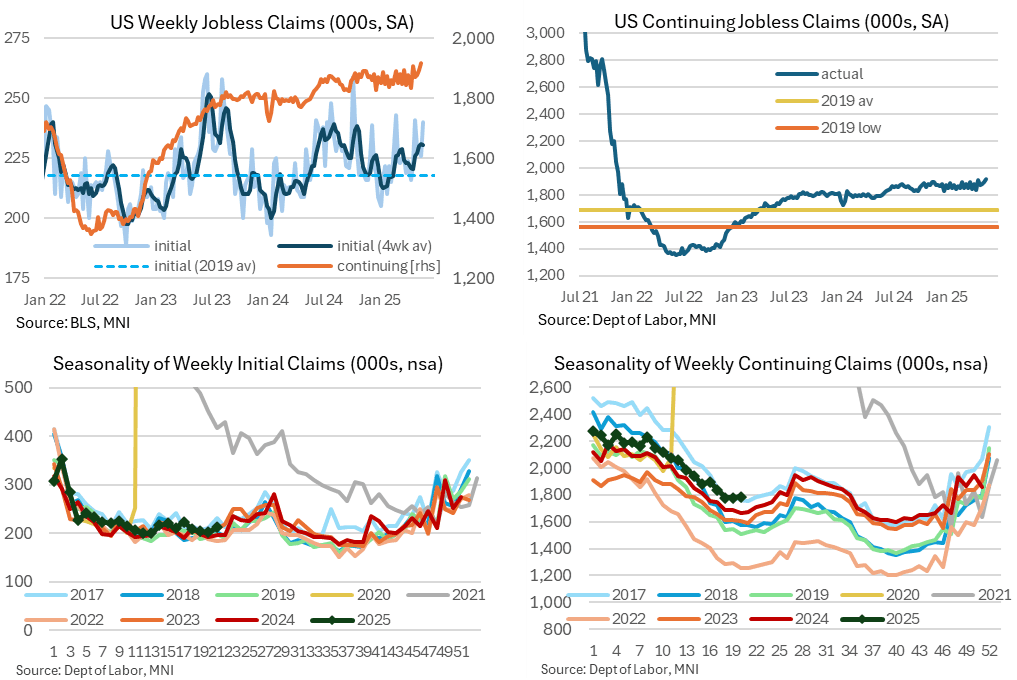

Latest weekly jobless claims data extend last week’s first signs of a renewed deterioration in the labor market, and with little sign of a particular distortion. The more notable finding in our view was a push higher in continuing claims to a fresh high since late 2021, suggesting rehiring conditions have recently become harder, but increases are still on the measured side for now.

- Initial jobless claims were higher than expected at 240k (sa, cons 230k) in the week to May 24 after a downward revised 226k (initial 227k).

- The four-week moving average was unchanged at 231k, as the latest print only offset the 241k spike in the last full week of April owing to the later timing of Easter this year. It remains at its highest since late October, a little above the 218k averaged in 2019 for context.

- The non-seasonally adjusted data for the time of year are higher than 2024 and 2022 but still within recent ranges for ‘normal’ years – see below charts.

- We can’t see much of note within the non-seasonally adjusted state details - Michigan led the increase with a 3.3k rise to 8.6k but that’s not unprecedented.

- Continuing claims surprisingly increased to 1919k (sa, cons 1893k) in the week to May 17, capturing a payrolls reference period, after a downward revised 1893k (initial 1903k).

- It marks a new high since late 2021, back above the 1900k mark that was first pierced in the week to Apr 19.

- It will be revised again next week but for now, the 1919k is a marked increase from the 1833k in last month’s payrolls reference period along with two months at 1847k before that.

- The below NSA charts show a continued upward drift relative to recent non-pandemic years, putting claims above recent ranges – see charts.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: APR STORE SALES +6.7% V YR AGO MO

Apr-29 12:55

- MNI: US REDBOOK: APR STORE SALES +6.7% V YR AGO MO

- US REDBOOK: STORE SALES +6.1% WK ENDED APR 26 V YR AGO WK

EGB SYNDICATION: Finland 10-year: Priced

Apr-29 12:44

- Reoffer: 99.870 to yield 3.016%

- Spread set earlier at MS+52bps (guidance was MS +54bps area)

- Benchmarket: 2.50% Feb-35 Bund +51bp. Spot ref 99.935, HR 102%

- Size: E4bln (in line with MNI expectation)

- Books closed in excess of E23.5bln (inc E750mln JLM interest)

- Coupon: 3.0%, annual, act/act ICMA, short first

- Settlement: 7 May 2025 (T+5)

- Maturity: 15 September 2035

- ISIN: FI4000587415

- Bookrunners: BNPP (DM/B&D) / Citi / CACIB / GSBE SE / Nordea

- Timing: TOE 13:27BST / 14:27CET. FTT immediately.

From market source / Bloomberg

EGB SYNDICATION: Finland 10-year: Priced

Apr-29 12:38

- Reoffer: 99.87 to yield 3.016%

- Spread set earlier at MS+52bps (guidance was MS +54bps area)

- Size: E4bln (in line with MNI expectation)

- Books closed in excess of E23.5bln (inc E750mln JLM interest)

- Coupon: 3.0%, annual, act/act ICMA, short first

- Settlement: 7 May 2025 (T+5)

- Maturity: 15 September 2035

- ISIN: FI4000587415

- Bookrunners: BNPP (DM/B&D) / Citi / CACIB / GSBE SE / Nordea

- Timing: Books to close at 10:15BST / 11:15CET

From market source / Bloomberg