US DATA: GDI Contracts In Tandem With GDP As Corporate Profits Pull Back

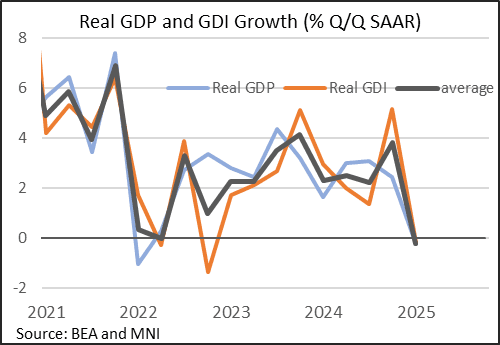

Real Gross Domestic Income contracted 0.2% Q/Q SAAR in Q1, per data made available in the 2nd national accounts release for the quarter. That's the weakest in 9 quarters, and a sharp reversal from Q4's 12-quarter best 5.2%.

- This was - unusually - exactly in line with the GDP reading of -0.2%, meaning the average of the two was likewise -0.2% - with the exception of the start of the Covid pandemic in 2020, this was the first negative reading since June 2016, and was a sharp reversal from +3.8% in Q4 (4-quarter high).

- As such it appears to suggest broader economic weakness in Q1 that can't just be attributed to weaker net exports.

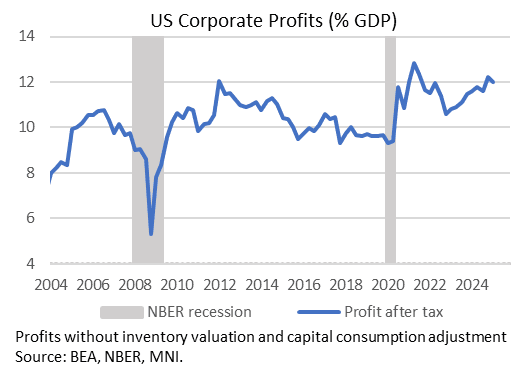

- Nominal corporate profits (with inventory valuation and capital consumption adjustments) fell 2.95% Q/Q SAAR, vs +5.4% prior, meaning that while profits are still higher than in Q3 2024, the Q4 gains were pared sharply.

- Overall though they are still very elevated (up 5.5% Y/Y and at 13% of GDP, vs 13.5% in Q4), with only modest profit margin compression in the quarter.

- Whether that remains the case going forward with tariffs will be worth watching, for the degree to which firms absorb tariff costs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Monitoring Support

- RES 4: 165.43 High Nov 8

- RES 3: 164.90 High Dec 30 ‘24 and a key medium-term resistance

- RES 2: 164.55 High Jan 7

- RES 1: 163.76/164.19 High Apr 25 / High Mar 18 and the bull trigger

- PRICE: 162.07 @ 16:24 GMT Apr 29

- SUP 1: 161.41/159.48 50-day EMA / Low Apr 9

- SUP 2: 158.30 Low Apr 7 and key support

- SUP 3: 157.02 76.4% retracement of the Feb 28 - Mar 18 bull cycle

- SUP 4: 155.60 Low Low Mar 4

Short-term weakness in EURJPY appears corrective and the trend condition remains bullish. Last week’s gains reinforce a bullish theme. Key S/T support lies at 158.30, the Apr 7 low. A break of it is required to signal scope for a deeper retracement. This would open 157.02, a Fibonacci retracement. First support to watch is 161.41, the 50-day EMA. Attention is on 164.19, the Mar 18 high and a bull trigger. Clearance of this hurdle would resume the uptrend.

US TSYS: Late SOFR/Treasury Option Roundup: Better Calls on Net

Option desks reported better upside call volume on net underlying futures see-saw near midday highs (TYM5 +7.5 at 112-04.5 vs. -07.5 high). Curves mildly steeper (2s10s +.412 at 51.346). Projected rate cut pricing rising in the second half of the year compared to this morning's levels (*) as follows: May'25 at -2.6bp (-2.3bp), Jun'25 at -16.9bp (-16.9bp), Jul'25 at -39.1bp (-37.6bp), Sep'25 -61.0bp (-57.4bp).

SOFR Options:

+20,000 SFRU5 96.00 puts, 10.0 vs. 96.315 to -.32/0.25%

-15,000 SFRN5/0QN5 96.12/96.25 call spd spd, 5.25 midcurve over, steepener

+10,000 SFRZ5 96.75/97.25 call spds, 14.25 ref 96.645

-8,000 0QM5 96.87/97.00/97.25/97.3 call condors, 2.87 ref 96.98

+2,500 0QM5 97.50/98.00/1000 2x3x1 call flys 7.0 vs. 96.365/0.14%

+3,500 0QK5 96.75 puts, 6.5

+5,000 SFRZ5 96.00/96.25/96.50 put trees, 2 ref 96.585

-4,000 0QM5/2QM5 95.87/96.12 put spd strip w/2QM5 96.00/96.25 put spd, 2.5 total

21,000 SFRM5 95.87/96.00/96.25/96.37 call condors

15,400 SFRM5 95.75/95.81 put spds ref 95.895

11,400 SFRM5 95.68 puts, 0.5 last

over 5,900 SFRZ5 95.62 puts, 3.5 last

12,580 SFRZ 95.56/95.68/95.81 put flys ref 96.575

2,500 0QZ5 97.00/97.50 call spds ref 96.935

1,850 SFRK5 95.81/96.18 1x2 call spds ref 95.885

Treasury Options:

+15,000 wk2 TY 112.75 calls, 21

2,500 TYM5 112 straddles,

+5,000 TYM5 109/113 strangles, 35-36

-6,000 TYM5 111.75 straddles, 142 (imp vol 7.22%)

+12,000 TYM5 110/113 strangles, 38-39 vs. 111-25/0.25% (imp vol 7.36%)

20,000 wk1 5Y (exp Fri)/Mon wkly 5Y (exp Mon) 110 call spds ref 108-26.75

6,300 TYM5 113/116 call spds ref 111-27.5

over 4,300 TYM5 114 calls

STIR FUTURES: BLOCK: Large SOFR White Pack

- Total of 8,000 SOFR White packs (SFRM5-SFRH6) Blocked at +0.030, most likely swap related with spreads running tighter in the vicinity.