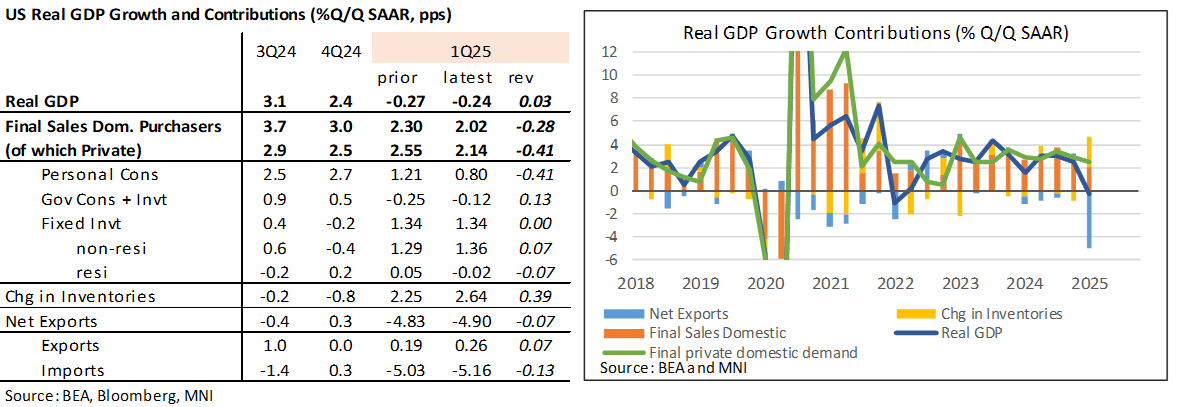

US DATA: Consumption Downward Revision In Q1 Offset By Inventories

• Real GDP growth was revised up fractionally to -0.24% annualized in the second Q1 release (cons -0.3) from the -0.27% in last month’s advance.

• The softer consumption figure was most notable, lowered to 1.2 % annualized (cons 1.7, advance 1.8).

• It dragged 0.4pp from GDP growth, offset by an even stronger boost from changes in inventories.

• See the contribution changes in the table below.

• Core PCE inflation meanwhile was revised lower from 3.46% to 3.41% (cons 3.5).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-Trade Balance, Inventories Data React

- Treasury futures holding lower levels, off lows after US trade deficit comes out larger than estimated, wholesale inventories rise but lower than estimated, retail inventories declines.

- Jun'25 10Y currently -5.5 at 111-23.5, well above initial technical support at 111-04+ (20-day EMA).

- Cross asset: BBG US$ index firmer at 1222.46 (+2.64); stocks mildly weaker: S&P eminis -4.5 at 5548.50.

CNY: Commerzbank Forecast USD/CNY at 7.50 by End-June

Commerzbank note that although they forecast USD/CNY at 7.50 by end-June, it represents their view that such level is “the line on the sand” that the PBOC may likely accept. The risk of the currency pair weakening to such a level in the near term has receded, they say. Meanwhile, the PBOC will unlikely allow CNY to weaken too much.

They say the PBOC is fighting a dilemma between monetary easing and supporting the yuan. However, it should not alter the stance on further monetary easing this year. Commerzbank still expect the PBoC to cut interest rates and reserve requirement ratios in the coming months. In the longer term, Commerzbank forecast a modest strengthening in the yuan in H2 2026, with USD/CNY a bit lower at 7.40.

Domestically, their baseline is that growth will remain slow, but downside risks will likely be reduced amid the efforts by the Chinese authorities. Externally, there could be positive news on trade deals by then.

GILTS: Initial Resistance In Futures Holds For A Second Day

Gilt futures continue to respect initial resistance at Friday’s high (93.34), topping out at 93.33 for a second consecutive session.

- Still, the bullish technical phase in the contract remains intact, with pullbacks remaining relatively shallow at this stage.

- If the move does develop further, through a break of Friday’s high, focus would quickly shift to the nearby 76.4% retracement of the April 7-9 sell off (93.44).

- Yields are 1-3bp lower on the day, with 10s outperforming and 50s lagging.

- Gilt bulls eye 4.460% in 10-Year yields.

- 2s10s continue to trade around 16bp below cycle closing highs, although the spread has failed to close back below 60bp since the break above in early April, last ~62.8bp.

- 5s30s is ~10bp below cycle closing highs, last 128bp.

- As we have previously noted, while fundamentals (the potential for a more activist BoE easing cycle, tepid economic growth and ongoing fiscal fragility) point to further curve steepening, already crowded steeper plays and apparent increased activism from public agencies (Treasury, DMO & the BoE) when it comes to limiting long end yield spikes presents risks/limitations to such moves, at least in the short-term.