MNI ASIA OPEN: Soft Jobs Report & Average Hourly Earnings

EXECUTIVE SUMMARY

MNI FED: Chicago's Goolsbee Still Undecided On September Cut, Watching Services CPI

MNI US: Schumer Says Democrats Will Force Votes On Trump Tariffs

MNI US DATA: AHE On The Soft Side, Especially Considering Lower Hours

MNI US DATA: Household Survey Shows Slacker Conditions, But Participation Rising

MNI US DATA: Another Tepid Month Of Job Creation Although June Remains The Low

MNI US DATA: An All Around Soft Payrolls Report

US

MNI FED: Chicago's Goolsbee Still Undecided On September Cut, Watching Services CPI

Chicago Fed President Goolsbee, a 2025 FOMC voter, tells Bloomberg TV that he is "undecided" on a rate cut at the September FOMC, saying he wants "to get more information". He plays down the signal from the recent nonfarm payrolls slowdown, due to a potentially softer labor force growth dynamics. He suggests one of the things he will be looking at in the meantime is the August inflation report out next week - and in particular, whether services inflation looks tame.

- On inflation: "In the last inflation reports we also had this uptick in inflation coming from services. We want to make sure that is more of a blip and not a more ominous indicator...if the inflation numbers come in and they give some indication that the inflation from tariffs is not looking to be an uptick in inflation on services, it does not look to be persistent. It looks to be more like a temporary blip in the arena. That would provide comfort to me that we are still on what I was calling the golden path."

NEWS

MNI US: Schumer Says Democrats Will Force Votes On Trump Tariffs

Senate Minority Leader Chuck Schumer (D-NY) says Democrats will 'force' votes in the coming weeks to reverse President Donald Trump's tariffs, citing today's soft jobs reports. Schumer: “Today’s jobs report was worse than the already low expectations. This is a blaring red light warning to the entire country that Donald Trump is squeezing the life out of our economy…In the coming weeks, Senate Democrats will force votes to reverse Donald Trump’s damaging tariffs and we will see whose side Republicans are on. I hope Republicans will choose wisely.”

MNI SECURITY: Trump Deploys F-35s To Puerto Rico, Esclatates Standoff w/Venezuela

The Trump administration has ordered the deployment of 10 F-35 stealth fighter planes to Puerto Rico to conduct operations against drug cartels, in an escalation of tensions with Venezuela, per Reuters. According to the report, the planes are expected to arrive in the area next week to supplement a flotilla of naval assets. The deployment follows Tuesday’s lethal military strike on a boat alleged by the Trump administration to be transporting narcotics to the United States.

MNI SECURITY: Second Trump-Putin Meeting Could Be 'Quickly Organised' - Kremlin

Kremlin Spokesperson Dmitri Peskov told Russian outlet Argumenty i Fakty that a second meeting between Russian President Vladimir Putin and US President Donald Trump could take place in the near future, with “working contacts" taking place "all the time.” Peskov: "I have no doubt that if the presidents consider it necessary, their meeting can be organized very quickly. Just as the meeting in Alaska was quickly organized."

US TSYS

MNI US TSYS: Projected Rate Cut Pricing Near -75bp by Year End After Soft Jobs Data

- Treasuries look to finish broadly higher after key employ data showed less job gains than expected for August. The Fed enters communication blackout tonight.

- Payrolls surprised lower in August (22k vs BBG cons 75k) and the u/e rate was on the dovish side at a new recent high of 4.324% (cons 4.3% but with a skew to a 4.2% print) after 4.25%. The downward revisions were concentrated in May (-27k vs +6k in June), offering no offset to last month’s huge downward revisions.

- Rate have gradually pared gains in the second half (TYZ5 +16.5 at 113-11.5 vs. 113-21.5 high) as markets continued to digest the labor data. Projected rate cuts remained well off pre-data (*) levels: Sep'25 at -28bp (-24.7bp), Oct'25 at -47.3bp (-38.6bp), Dec'25 at -69.7bp (-59bp), Jan'26 at -83.5bp (-71.1bp).

- Chicago Fed President Goolsbee, a 2025 FOMC voter, tells Bloomberg TV that he is "undecided" on a rate cut at the Sep 17 FOMC, saying he wants "to get more information", playing down the signal from the recent nonfarm payrolls slowdown, due to a potentially softer labor force growth dynamics. He suggests one of the things he will be looking at in the meantime is the August inflation report out next week - and in particular, whether services inflation looks tame.

- The USD fell sharply in tandem with yields, putting the USD Index to new September lows and within range of first support into the late July lows of 97.109 and the bear trigger into the July 1st print at 96.377.

- Generally slow start to next week - focus on PPI and CPI net Wed-Thu respectively.

OVERNIGHT DATA

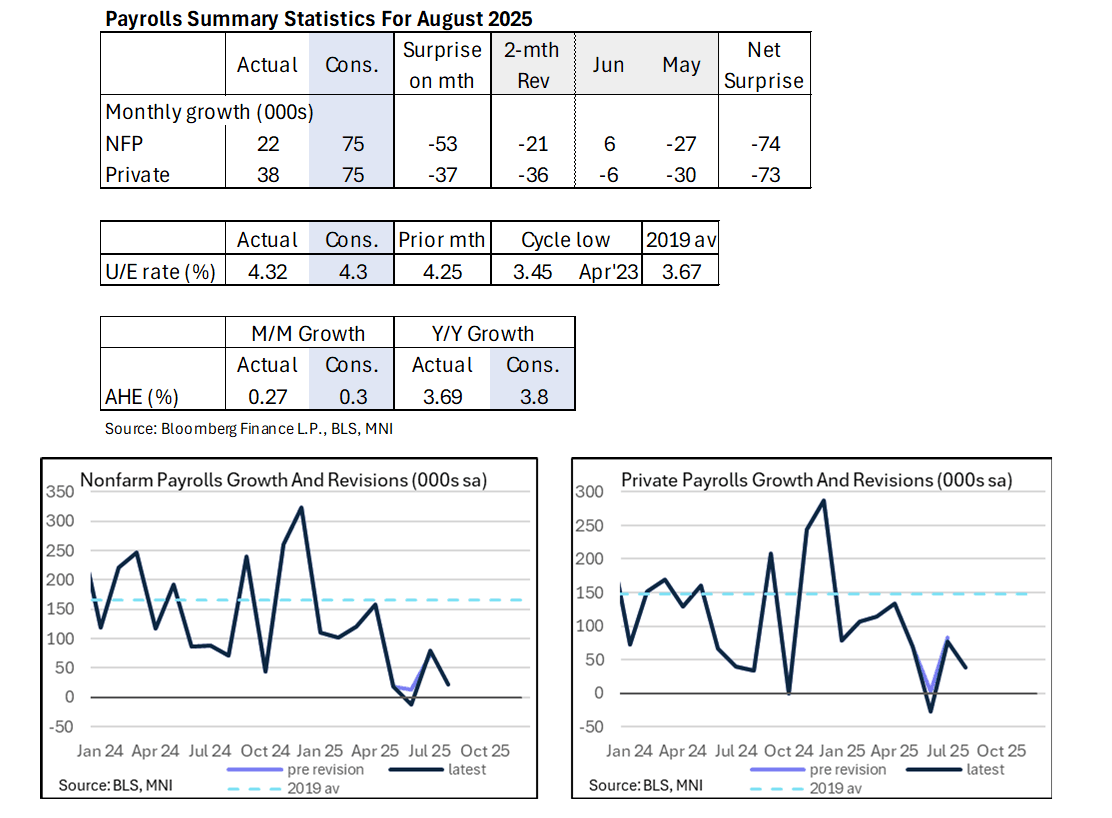

MNI US DATA: An All Around Soft Payrolls Report

- Payrolls surprised lower in August (22k vs BBG cons 75k) and the u/e rate was on the dovish side at a new recent high of 4.324% (cons 4.3% but with a skew to a 4.2% print) after 4.25%.

- The downward revisions were concentrated in May (-27k vs +6k in June), offering no offset to last month’s huge downward revisions.

- Similar story in private payrolls with 22k vs cons 75k and two-month revisions of -36k.

- 3-month average: 29k NFP, 29k private.

MNI US DATA: Another Tepid Month Of Job Creation Although June Remains The Low

We’re simultaneously writing on the household survey, an area of increased focused with its unemployment rate giving a better gauge of labor market balance amidst a material pullback in labor supply, but the below digs into the payrolls side of the report. The figures should be viewed against recent payrolls breakeven estimates roughly in a range of 50-100k but some seeing scope for lower estimates.

- Nonfarm payrolls growth was softer than expected in August at 22k (sa, cons 75k) along with a two-month downward revision of -21k coming entirely in June.

- The private sector saw a similar story on balance, with a slightly smaller miss with 38k (sa, cons 75k) but a larger downward revision of -36k.

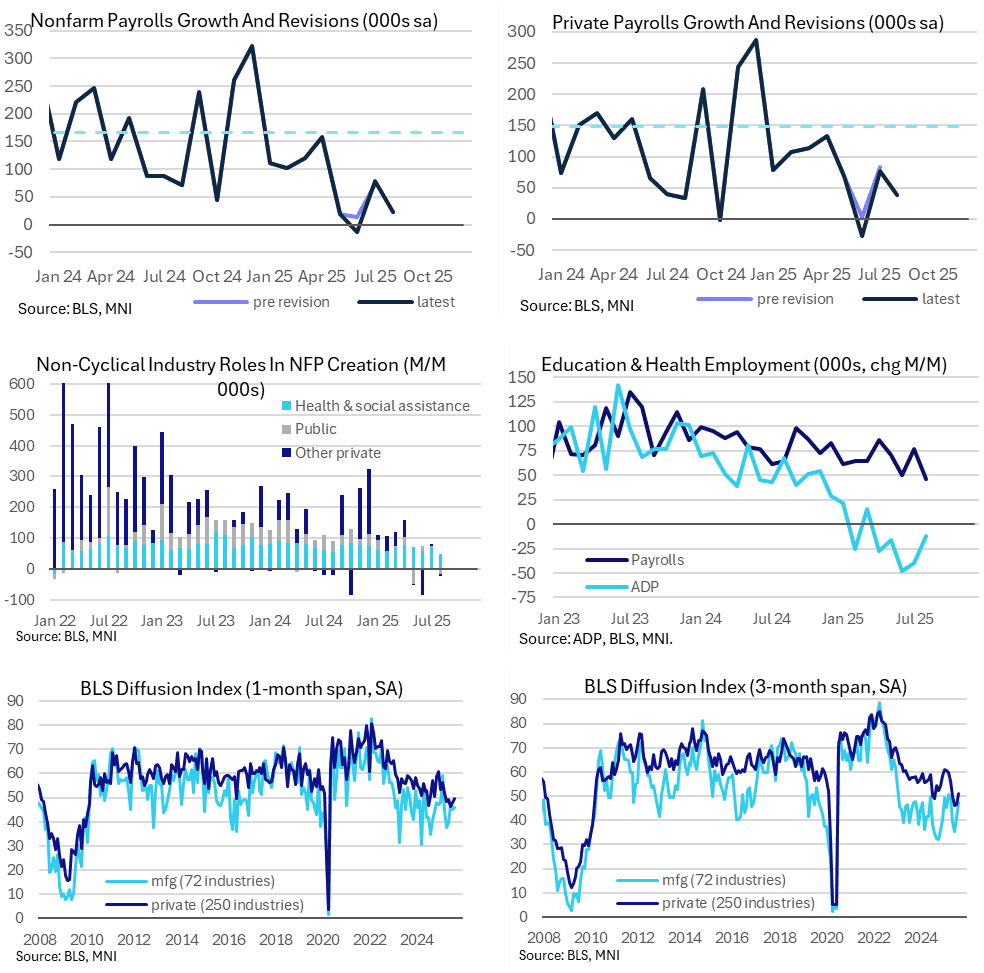

- However, this private sector payrolls growth continues to be dominated by the cyclically incentive health & social assistance category, which despite rising by its least since Jan 2022 still added 47k jobs. Private payrolls ex health & social assistance fell -9k.

- That leaves latest three-month averages of 29k for nonfarm, 29k for private and -30k for private ex health & social assistance. The latter is down from 97k in December.

- The one-month diffusion index for 250 private industries broadly echoes this weak private sector job creation trend, marking a fifth consecutive month sub-50, i.e. with more industries declining on the month than increasing. Admittedly, the 49.6 in August was the highest of these five sub-50 readings, having improved from a particularly low 46.2 in June, but it’s still a subdued trend.

- Coincidentally, that June weakness coincides with a particularly weak overall payrolls reading, with -13k for NFP (in the latest data vintage the first contraction since Dec 2020), -27k for private and -83k for private ex-health & social assistance.

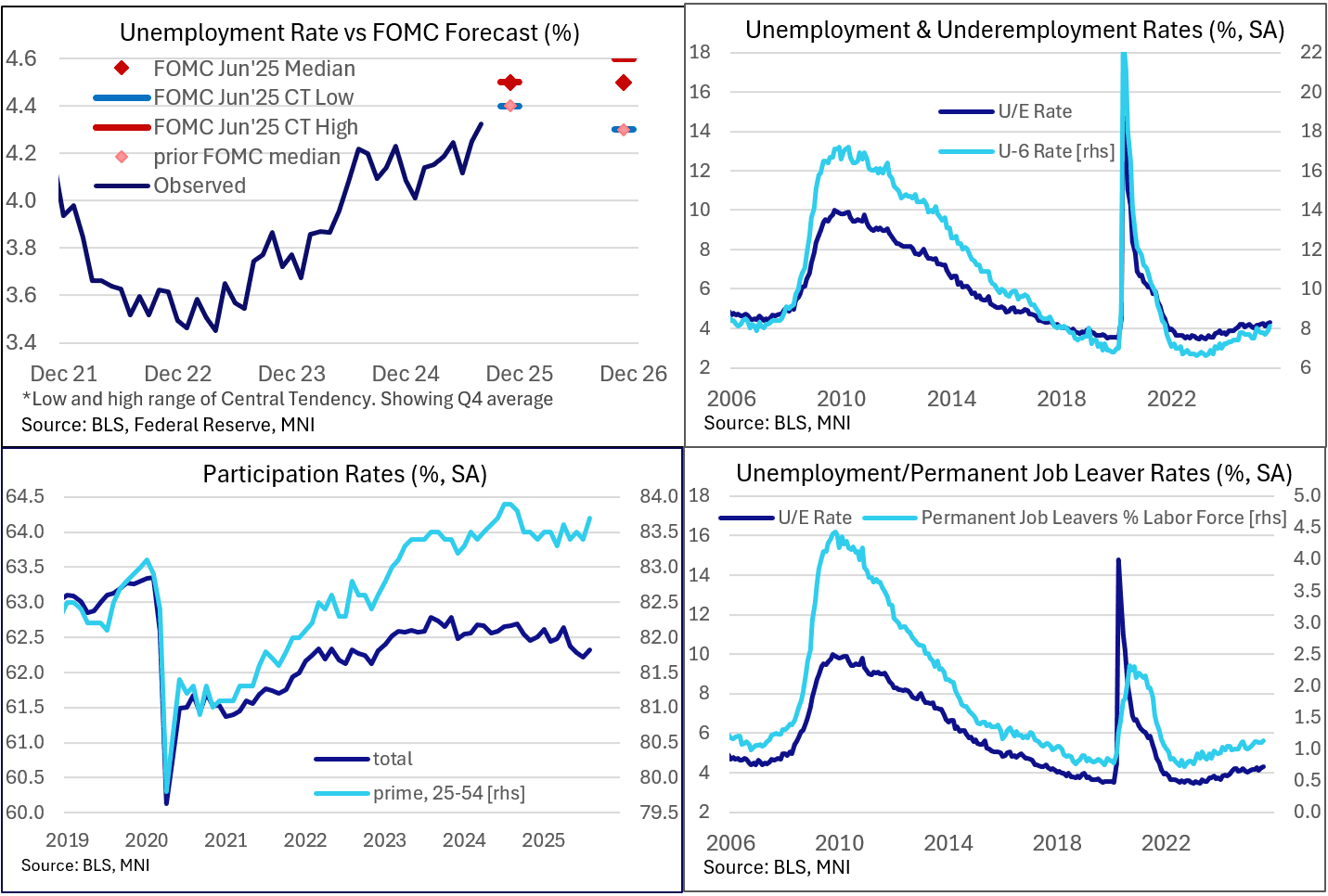

MNI US DATA: Household Survey Shows Slacker Conditions, But Participation Rising

The Household Survey showed an uptick in its main measures of labor market slack. That said, there weren't a lot of major new warning signals in the various Household metrics were mixed aside with continued slow deterioration in some areas, though exceptions included noticeable weakness in some demographic categories (more on which shortly) but surprising strength in prime-age participation.

- The unrounded unemployment rate rose to 4.324% from 4.248% prior, marking the highest (and first above 4.30%) since October 2021. And the U-6 "underemployment" rate rose to 8.1% from 7.9%, likewise a post-October 2021 high.

- Household employment rose 288k, basically reversing July's 260k drop but keeping the level of employment 501k below January's level. The number of unemployed rose 148k after 221k, the highest 2-month rise since Jun-Jul 2024, and up 535k since January.

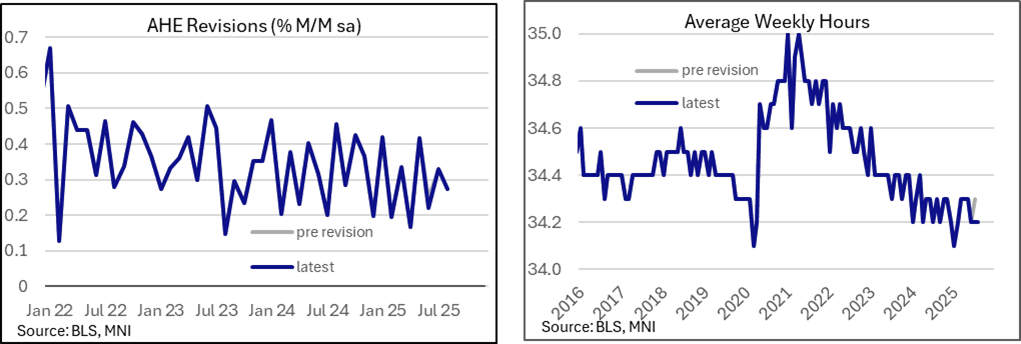

MNI US DATA: AHE On The Soft Side, Especially Considering Lower Hours

For completeness, AHE on the soft side of 0.3% M/M rounding (cons 0.3) although the non-supervisory category was strong.

- Total AHE:

- M/M (SA): 0.274% in Aug from 0.33% in Jul (initial 0.33%)

- Y/Y (SA): 3.69% in Aug from 3.878% in Jul

- AHE Non-Supervisory:

- M/M (SA): 0.383% in Aug from 0.256% in Jul (initial 0.256%)

- Y/Y (SA): 3.931% in Aug from 3.878% in Jul

Source: Bloomberg Finance L.P., MNI

Note also the weak hours worked at 34.2 after a downward revision. Whilst not unprecedented, it adds to the softer readings from the report - see charts:

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 206.62 points (-0.45%) at 45412.47

S&P E-Mini Future down 23 points (-0.35%) at 6487

Nasdaq down 24.7 points (-0.1%) at 21681.16

US 10-Yr yield is down 7.3 bps at 4.0876%

US Dec 10-Yr futures are up 16/32 at 113-11

EURUSD up 0.0067 (0.58%) at 1.1716

USDJPY down 1.01 (-0.68%) at 147.47

WTI Crude Oil (front-month) down $1.52 (-2.39%) at $61.96

Gold is up $47.92 (1.35%) at $3593.67

European bourses closing levels:

EuroStoxx 50 down 28.56 points (-0.53%) at 5318.15

FTSE 100 down 8.66 points (-0.09%) at 9208.21

German DAX down 173.35 points (-0.73%) at 23596.98

French CAC 40 down 24.14 points (-0.31%) at 7674.78

US TREAURY FUTURES CLOSE

2Y10Y -0.07, 57.019 (L: 56.143 / H: 60.774)

2Y30Y -0.843, 125.504 (L: 125.346 / H: 133.123)

5Y30Y -2.375, 118.219 (L: 118.219 / H: 126.261)

Current futures levels:

Dec 2-Yr futures up 4.375/32 at 104-14.875 (L: 104-10.125 / H: 104-18.25)

Dec 5-Yr futures up 8.25/32 at 109-28.5 (L: 109-20.25 / H: 110-05)

Dec 10-Yr futures up 16/32 at 113-11 (L: 112-28 / H: 113-21.5)

Dec 30-Yr futures up 1-18/32 at 116-14 (L: 115-02 / H: 116-18)

Dec Ultra futures up 2-0/32 at 119-13 (L: 117-21 / H: 119-17)

MNI US 10YR FUTURE TECHS: (Z5) Contract Highs

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ Intraday High & 2.618 proj of the Jul 15 - 22 - 28 price swing

- PRICE: 113-14+ @ 16:56 BST Sep 5

- SUP 1: 112-28+/112-04 Intraday low / 20-day EMA

- SUP 2: 111-22 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

The trend outlook in Treasury futures firmed further Friday, bringing in new contract highs for the Z5 contract. The move higher also highlights an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next, a Fibonacci projection that was challenged at today’s high. Initial firm support to watch is 112-04, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Sep 25-Jun 26):

Sep 25 +0.058 at 95.988

Dec 25 +0.10 at 96.365

Mar 26 +0.110 at 96.625

Jun 26 +0.095 at 96.875

Red Pack (Sep 26-Jun 27) +0.040 to +0.075

Green Pack (Sep 27-Jun 28) +0.035 to +0.035

Blue Pack (Sep 28-Jun 29) +0.040 to +0.050

Gold Pack (Sep 29-Jun 30) +0.055 to +0.070

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.41% (+0.02), volume: $2.834T

- Broad General Collateral Rate (BGCR): 4.38% (+0.02), volume: $1.131T

- Tri-Party General Collateral Rate (TCR): 4.38% (+0.02), volume: $1.108T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $231B

FED Reverse Repo Operation

RRP usage inches up to $20.997B with 15 counterparties this afternoon from $20.128B yesterday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occured on June 30.

MNI PIPELINE: Corporate Bond Roundup: Near $100B Debt Issued Since Tuesday

$15.9B Priced Thursday, $98.95B total since Tuesday - most since the first week of January ($135.55B):

- Date $MM Issuer (Priced *, Launch #)

- 09/04 $6.5B *Citigroup $3B 6NC5 +85, $500M 6NC5 SOFR, $3B 11NC10 +100

- 09/04 $1.9B *Sunoco $1B 5.5NC2 5.625%, $900M 8.5NC3 5.%

- 09/04 $1.5B *Sunoco PerpNC5

- 09/04 $1.25B *Avalon Holdings 7Y +120

- 09/04 $1.2B *SK Hynix $600M 3Y +73, $600M 5Y +80

- 09/04 $1B *Swedish Export Credit 5Y SOFR+48

- 09/04 $750M *Brookfield Asset Management 30Y +120a

- 09/04 $700M *Kallpa Gerneracion 10Y +140

- 09/04 $1.1B *HPS Corporate Lending Fund $600m 3Y +155, $500m 5Y +183

MNI BONDS: EGBs-GILTS CASH CLOSE: Weak US Jobs Data Helps Bull Flattening Continue

European curves bull flattened again Friday, with a downside surprise in US employment driving the rally.

- This was the third consecutive day of gains led by the long-end. While the session started constructively, ranges were relatively narrow, with weaker-than-expected German factory orders helping set a bullish tone for Bunds.

- In the UK, retail sales data were firmer-than-expected (but only due to downward revisions, which made for a marginally dovish report overall), but the big news was the resignation of deputy PM Rayner and a broader cabinet reshuffle, raising further uncertainty over the fiscal policy outlook.

- The main event of the day - the US employment report for August - showed weaker-than-expected job gains along with downward revisions and a slightly higher-than-anticipated unemployment rate, boosting Fed cut pricing and extending gains across global core curves.

- Gilts outperformed Bunds on the day. That's also true for the week: UK 2Y yield -3.3bp, 10Y -6.6bp; German 2Y yield -1.1bp, Germany -6.2bp.

- Periphery/semi-core EGB spreads were mixed on the day, with earlier tightening reversing toward the close as equities pulled back.

- Next week's highlights include Monday's expected confidence vote in the French government, and the ECB decision on Thursday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.5bps at 1.929%, 5-Yr is down 5.1bps at 2.219%, 10-Yr is down 5.7bps at 2.662%, and 30-Yr is down 4bps at 3.297%.

- UK: The 2-Yr yield is down 3.9bps at 3.91%, 5-Yr is down 6.2bps at 4.048%, 10-Yr is down 7.4bps at 4.646%, and 30-Yr is down 7bps at 5.504%.

- Italian BTP spread down 0.8bps at 84.2bps / French OAT up 1bps at 78.6bps

MNI FOREX: CAD Outdoes USD on Twin Jobs Market Weakness

- Both the US and Canada printed weaker-than-expected jobs reports Friday, sending both the USD and CAD lower against all others in G10. The US reported job gains of just 22k across August, resulting in both a higher unemployment rate as well as slower average hourly earnings. Compounding the bad news, the two-month net revision came in negative, pointing to persistent economic weakness into Q3.

- Resultantly, Fed rate cut pricing into year-end firmed aggressively. Markets added close to half a 25bps rate cut by for the December 2025 meeting, making 3x25bps rate cuts more likely than not. The USD fell sharply in tandem, putting the USD Index to new September lows and within range of first support into the late July lows of 97.109 and the bear trigger into the July 1st print at 96.377.

- We noted earlier Friday that the deterioration of the USD net position had stalled over Summer (potentially triggered by fragile European, UK politics), but today's payrolls number may provide the impetus for fresh shorts - a lacking driver since the post-tariffs downleg.

- CAD/JPY broke to new September lows and is now testing the 200-dma of 106.12 on the poor Canadian jobs numbers. The net change in employment dropped 65k, led by part-time employment and making for a new post-COVID high unemployment rate. Markets saw little reprieve in Carney detailing an extension of loan programmes for companies hit by US tariffs.

- Focus for the coming week shifts to the LDP meeting in Japan, at which party members will determine whether to trigger an early leadership election against PM Ishiba, which may introduce further political uncertainty. USD/JPY traded through the 50-dma into the Friday close, as the JPY benefited from a return lower for US stock markets.

- A busy week for US data next week, as both CPI and PPI prints are set to further inform the Fed's views on policy. CPI is expected to re-accelerate to 2.9% from 2.7% - complicating the policy mix as the central bank come under further scrutiny from the White House. Treasury Secretary Bessent called for an independent review into the Bank, which he sees as having lost public trust and credibility.

- The ECB rate decision is also due, at which markets expect little change on headline policy. EUR/GBP remains inside a nascent short-term uptrend, with 0.8713 representing the first upside trigger.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/09/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/09/2025 | 0600/0800 | ** | Trade Balance | |

| 08/09/2025 | 0600/0800 | ** | Industrial Production | |

| 08/09/2025 | - | *** | Trade | |

| 08/09/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/09/2025 | 1900/1500 | * | Consumer Credit | |

| 09/09/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor |