PIPELINE: Corporate Bond Roundup: Near $100B Debt Issued Since Tuesday

$15.9B Priced Thursday, $98.95B total since Tuesday - most since the first week of January ($135.55B):

- Date $MM Issuer (Priced *, Launch #)

- 09/04 $6.5B *Citigroup $3B 6NC5 +85, $500M 6NC5 SOFR, $3B 11NC10 +100

- 09/04 $1.9B *Sunoco $1B 5.5NC2 5.625%, $900M 8.5NC3 5.%

- 09/04 $1.5B *Sunoco PerpNC5

- 09/04 $1.25B *Avalon Holdings 7Y +120

- 09/04 $1.2B *SK Hynix $600M 3Y +73, $600M 5Y +80

- 09/04 $1B *Swedish Export Credit 5Y SOFR+48

- 09/04 $750M *Brookfield Asset Management 30Y +120a

- 09/04 $700M *Kallpa Gerneracion 10Y +140

- 09/04 $1.1B *HPS Corporate Lending Fund $600m 3Y +155, $500m 5Y +183

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

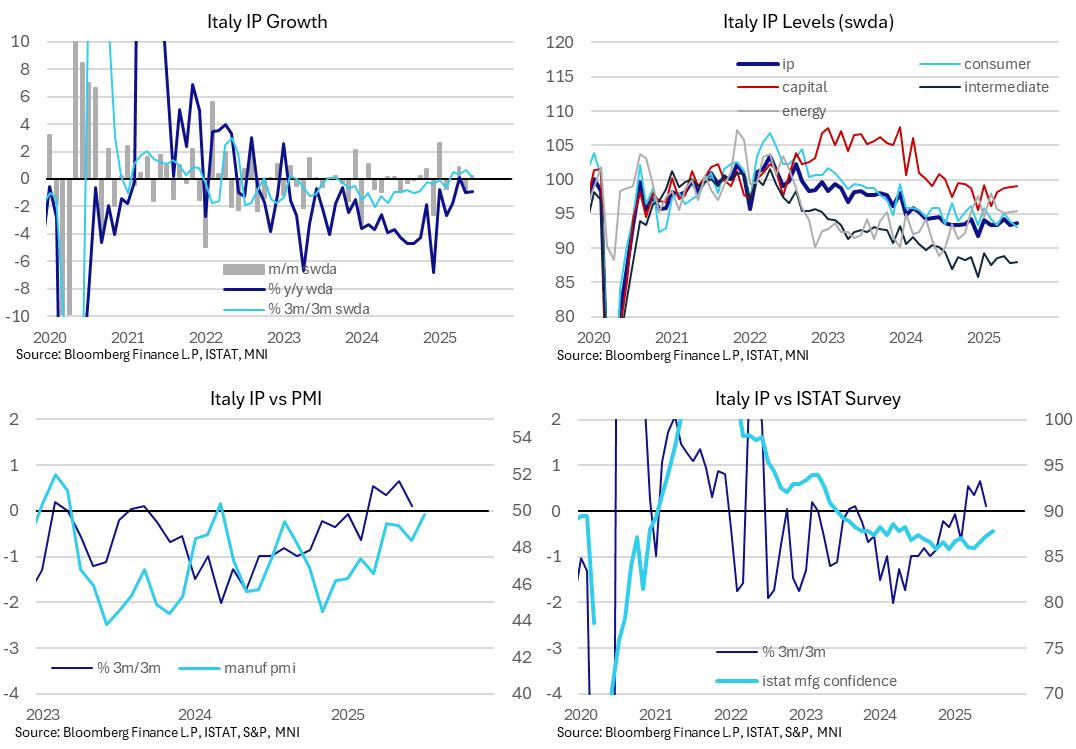

ITALY DATA: Another Stronger-than-expected June IP Report

Italian industrial production was stronger-than-expected in June at 0.2% M/M (vs -0.2% cons, a one tenth downwardly revised -0.8 prior). The Italian print follows stronger-than-expected readings in France and Spain yesterday. Germany will release its June IP figures tomorrow morning.

- Italian manufacturing sentiment data for July points to a continuation of this year’s gradual recovery, with the manufacturing PMI at its highest since March 2024 at 49.8 (vs 48.4 in June) and ISTAT’s manufacturing sentiment series at 87.8 (vs 87.3 in June).

- On a 3m/3m basis, IP rose just 0.1% in June, down from 0.6% in May. ISTAT noted that industry made a negative contribution to total gross value added in Q2, according to flash data released last month.

- Across components, there was slight growth in energy (0.1% M/M), intermediate goods (0.2% M/M) and capital goods (0.1% M/M) production in June. Meanwhile, consumer goods production fell 0.9% M/M (vs -1.3% in May).

US TSYS: Goldman Note Risk Of Further Curve Steepening

Goldman Sachs write “the shift in Fed cut pricing has compressed the gap between the market and our economists' expected Fed path. Despite the abruptness of last Friday's rally, we think risk/reward favours remaining long the front end in the U.S.. The timing and pace of any policy adjustment are key to dictating the curve shape, with the sustained outperformance of 5s at risk in the event of more rapid cuts”.

- They go on to note that “while the long end of the curve is somewhat cheap versus fundamentals, we nonetheless expect that evidence of further economic weakness would justify stronger front-end outperformance and sharper curve steepening”.

- Goldman’s “year-end forecasts of 3.45% 2-Year and 4.20% 10-Year yields imply steepening of the spot curve and relatively stable longer term rates”.

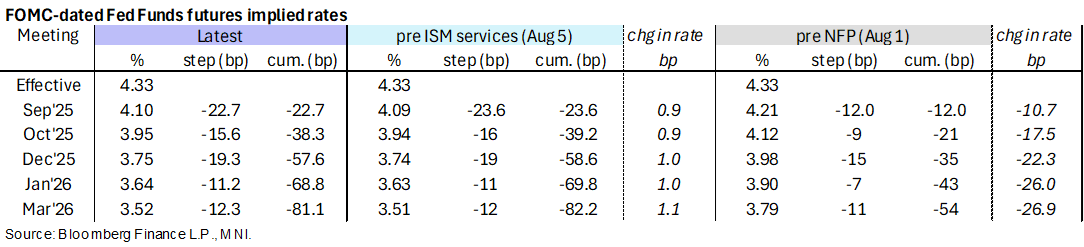

STIR: Slightly Less Dovish, More Post-FOMC (and NFP) Fedspeak Later

- Fed Funds implied rates are up to 1.5bp higher for meetings out to Mar 2026, hovering close to their highest since the Friday’s NFP and ISM mfg reports had been digested but still holding a strong dovish shift on net.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 38.5bp Oct, 57.5bp Dec, 69bp Jan and 81bp Mar.

- The SOFR implied terminal yield of 3.055% (SFRH7, +2.5bp) continues its slow rise off Monday’s lowest close since late April, but still broadly prices five cuts from current levels.

- Today sees a particularly thin data docket although there is a continuation of post-FOMC and NFP Fedspeak later on. Bostic and Hammack took a measured tone on Friday, Daly a little more dovish on Monday.

- 1400ET – Gov. Cook (permanent voter) and Collins (’25 voter) in a panel event (no text). We last heard from Cook back in early June when she warned the Fed must be open to all possibilities regarding rates including explicit mention of rate hikes. Collins pushed an “actively patient” approach to monetary policy as remaining appropriate when last speaking in mid-July.

- 1610ET – Daly (non-voter) speaks at Anchorage Economic Summit (text + Q&A). She told Reuters late Monday that she still sees two rate cuts this year as “an appropriate amount of recalibration”. “We of course could do fewer than two if inflation picks up and spills over or if the labor market springs back”. However, “I think the more likely thing is that we might have to do more than two...we also should be prepared in my judgment to do more if the labor market looks to be entering that period of weakness and we still haven’t seen spillovers to inflation”

- Trump yesterday on deliberations over Gov. Kugler’s board position: “I’ll be making that decision before the end of the week. We’ll either decide on one for permanence or the four-month period — the term. You know, there’s a term of about a number of months.”