MNI ASIA OPEN: SF Fed Daily - Can't Wait Forever to Cut Rates

EXECUTIVE SUMMARY

- MNI FED: Can’t Wait Forever To Cut Rates - Daly

- MNI US DATA: Subdued Import Prices In June Despite A Rare Increase From China

- MNI US DATA: June Retail Sales Surge Led By Ex-Control Group Categories

- MNI US: Senate Passes Trump's Rescissions Package, Raises Risk Of Govt Shutdown

- MNI US DATA: Jobless Claims Surprise Lower, Including Payrolls Ref Week For Initial

US

MNI FED: Can’t Wait Forever To Cut Rates - Daly

San Francisco Fed’s Daly (non-voter), speaking on Bloomberg TV, reiterates that she sees two rate cuts this year. She says it’s important to not lower rates pre-emptively but at the same time, the Fed can’t wait forever on rates.

- Recall that talking at an MNI event on Jul 10, she thought the Fed should start thinking about cutting interest rates, potentially twice this year, and it's possible that a large tariffs-driven increase in inflation does not materialize. To support a September rate cut, Daly said she's looking for "a continuation of what we've been seeing, which is modest" disinflation. Back to today’s comments:

- “I wouldn’t want to see more weakness in the labor market, I really wouldn’t want to see that. Which is why you can’t wait for ever, thinking that inflation is just around the corner so you have to wait until you know. Clarity in central bank is overrated. We want some clarity, but we can’t wait for clarity” otherwise will be backwards looking and by then it’s too late.

NEWS

MNI US: Senate Passes Trump's Rescissions Package, Raises Risk Of Govt Shutdown

The Senate has voted 51-48 to pass President Donald Trump's USD$9 billion request to cut Congressionally authorised funding for the State Department's foreign aid budget and public broadcasters. Two Republican Senators, Susan Collins (R-ME) and Lisa Murkowski (R-AK), voted against the measure. While the bill claws back a relatively small portion of federal government spending, Democrats view the request as part of a broader plan by the Trump administration to co-opt spending powers from Congress.

MNI US: Trump Unlikely To Fire Powell But Has "Substantial Concerns" - Vought

OMB Director, Russell Vought, told reporters that President Donald Trump “was pretty clear” he isn’t likely to fire Fed Chair Jerome Powell, but reiterated the White House has issues with Powell’s handling of a Fed renovation project in Washington DC, seen as a potential ‘for cause’ to dismiss Powell. Vought: “I think the president was pretty clear yesterday that he is unlikely to fire the chairman, but he has substantial concerns with regard to how he has managed the Fed. Not just on interest rate policy but [also] cost overrun [at the Fed D.C. office renovation] we’re trying to get a visit right now…”

US TSYS

MNI US TSYS: Near Midrange After Early Post-Data Volatility

- Treasuries look to finish near opening levels after whipsawing lower/higher following this morning's data. Less headline driven volatility on the day as threats of Pres Trump threats to fire Fed Chair Powell ahead of his May 2026 term end cooled.

- Treasury futures extend lows after lower than expected weekly and continuing jobless claims, retail sales higher than expected (modest up-revisions to prior), import prices lower/export higher than expected. little react to latest in-line Business Inventories & Housing Markets index data.

- Trading desks at a loss to explain the rebound off this morning's lows, no particular headline or flow drivers as Tsys climb past yesterdays highs - back to early Tuesday levels.

- The latest weekly jobless claims report was better than expected for both initial and continuing claims, extending improvements in initial claims (and this time for a payrolls reference period) whilst continuing claims stabilize rather than extend what had been a sharp rise back in June.

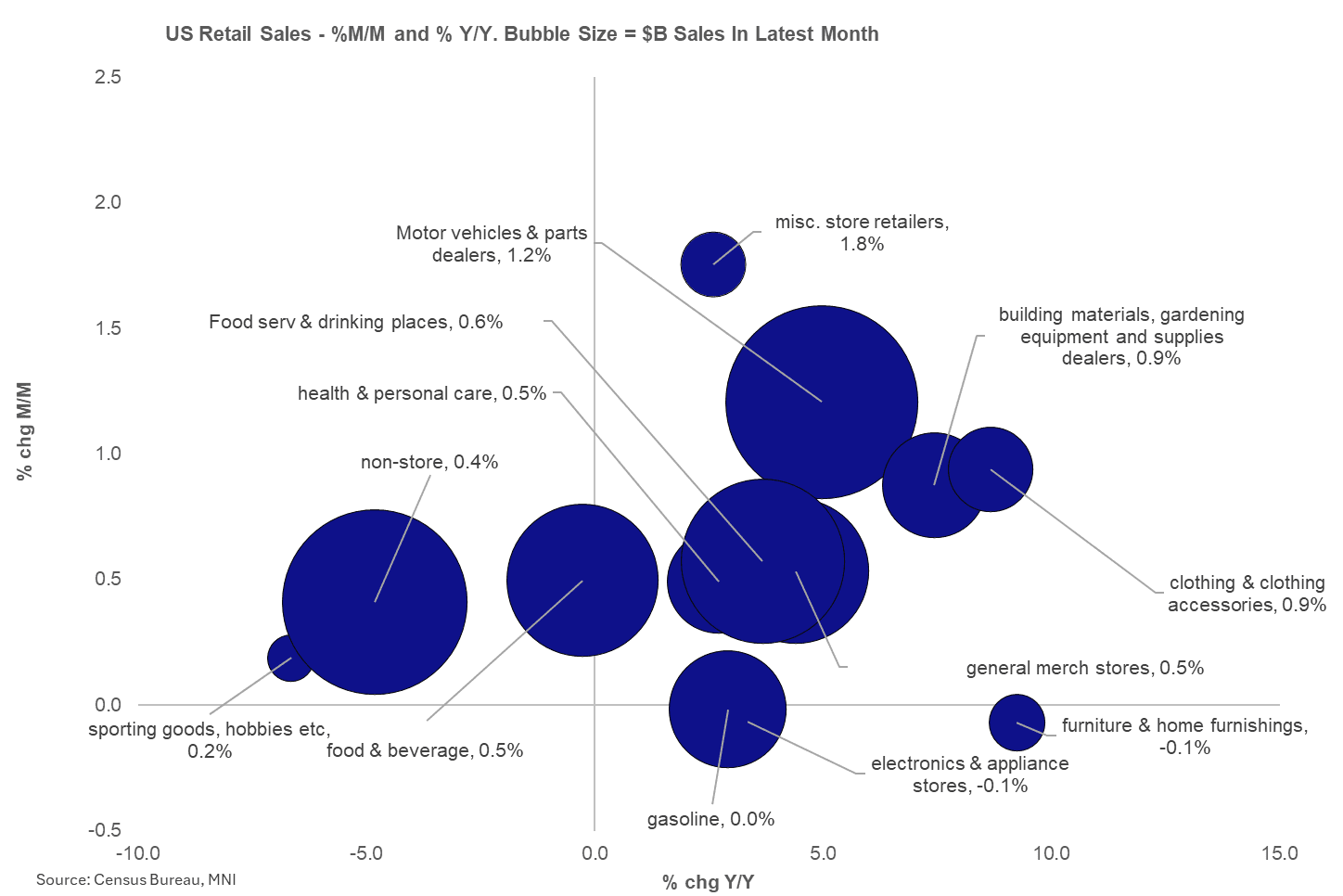

- Retail sales were more solid than expected in June. It was expected that the GDP-input Control Group category would come in stronger than the other main aggregates, due in large part to anticipated weakness in auto sales, but this did not play out: Control was actually one of the weaker parts of this report relatively speaking, rising 0.5% M/M - above expectations of 0.3%, but this was offset by a 0.2pp downward rev to 0.2% in May.

- Currently, Sep'25 10Y futures -2.5 at 110-17.5 vs. 110-25 high, 10Y yld +.0020 at 4.4573%, curves remain flatter after basis hit highest levels since October 2021 late Wednesday: 2s10s currently -2.219 at 53.722, 5s30s -1.098 at 100.548.

- Cross asset: stocks firmer/new highs (SPX eminis +39.5 at 6342.75); Bbg US$ index firmer/off highs (BBDXY +3.45 at 1207.56); Gold weaker/off lows (-6.73 at 3340.40); crude firmer (WTI +1.19 at 67.57).

OVERNIGHT DATA

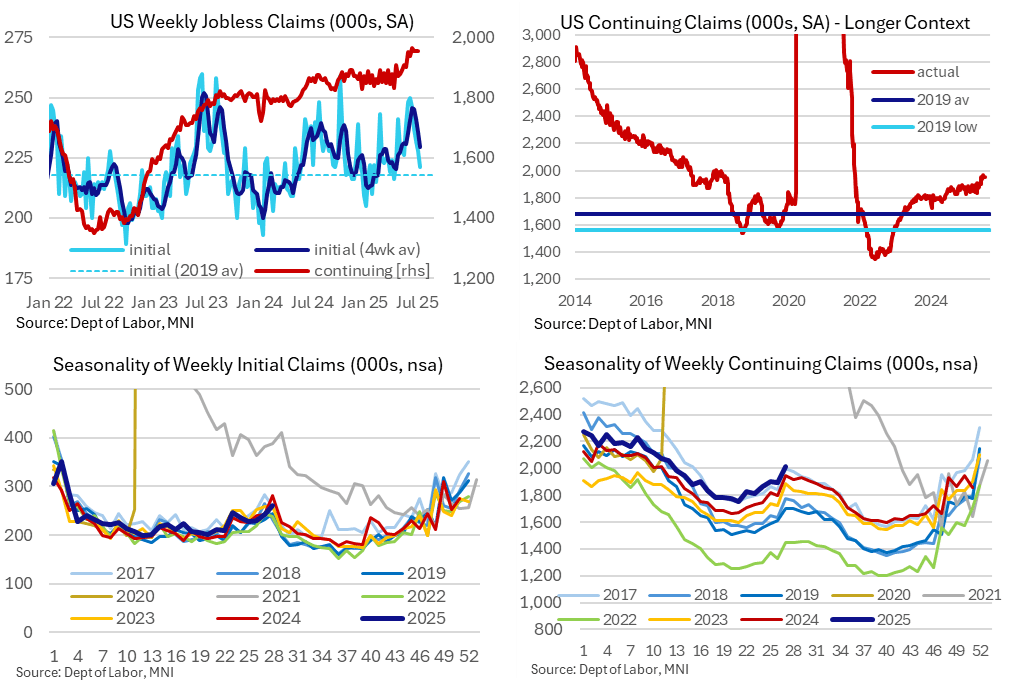

MNI US DATA: Jobless Claims Surprise Lower, Including Payrolls Ref Week For Initial

The latest weekly jobless claims report was better than expected for both initial and continuing claims, extending improvements in initial claims (and this time for a payrolls reference period) whilst continuing claims stabilize rather than extend what had been a sharp rise back in June. It broadly continues to chime with a 'low firing, low hiring' labor market.

- Initial jobless claims: 221k (sa, cons 233k) in the week to Jul 12 – a payrolls reference period – after a marginally upward revised 228k (initial 227k). It sets up a more favorable comparison with last month’s payrolls report, with the 221k vs 246k a month ago for back more in keeping with the 226k in May and 216k in April.

- Continuing claims: 1956k (sa, cons 1965k) in the week to Jul 5 after a downward revised 1954k (initial 1965k). It extends some stabilization in continuing claims after what had been a swift climb to a new 3+ year high of 1964k in mid-June.

MNI US DATA: June Retail Sales Surge Led By Ex-Control Group Categories

Retail sales were more solid than expected in June. It was expected that the GDP-input Control Group category would come in stronger than the other main aggregates, due in large part to anticipated weakness in auto sales, but this did not play out: Control was actually one of the weaker parts of this report relatively speaking, rising 0.5% M/M - above expectations of 0.3%, but this was offset by a 0.2pp downward rev to 0.2% in May.

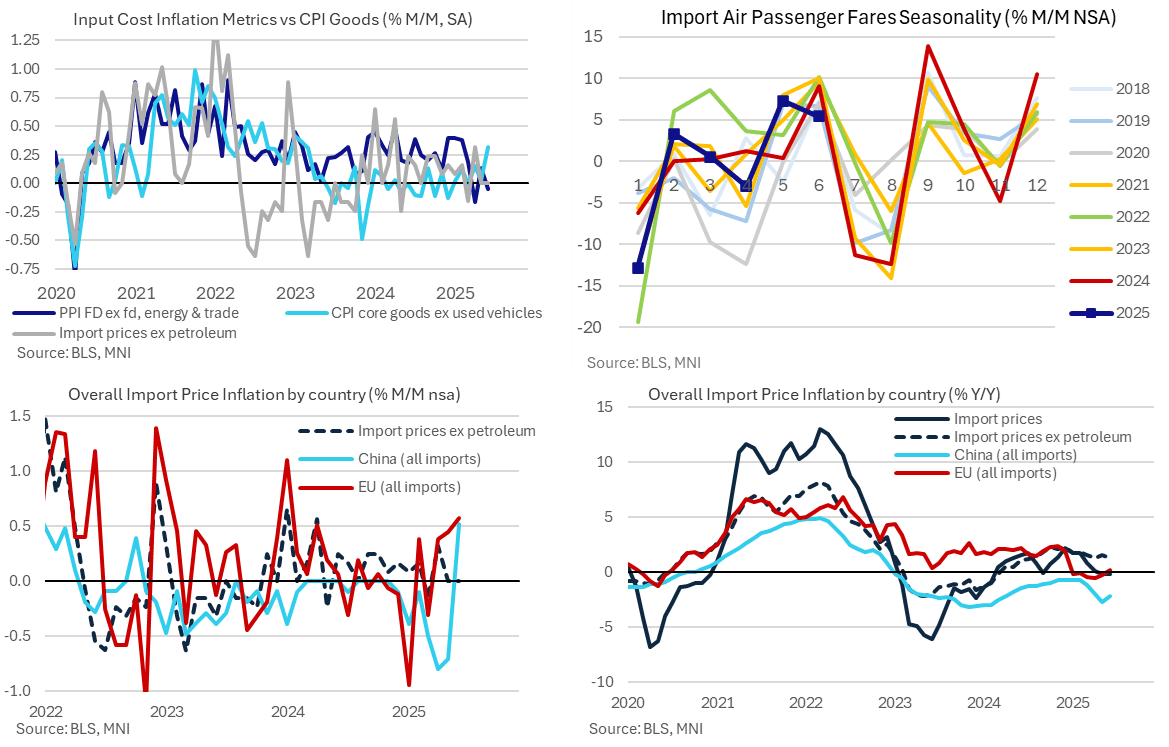

MNI US DATA: Subdued Import Prices In June Despite A Rare Increase From China

The US terms of trade saw a sizeable improvement in June from a combination of stronger than expected export prices and weaker than expected import prices. The latter came despite stronger China import prices in a partial correction after what had looked like some implicit taking of a tariff hit in April and May. Looking specifically at M/M pressures in June, the relative strength in consumer goods prices look at odds with both yesterday’s core PPI figures and today’s import prices.

- Import price inflation was softer than expected in June at 0.1% M/M (cons 0.3) after a downward revised -0.4% (initial 0.0%) in May. Combined with surprisingly firm export prices, at 0.5% M/M (cons 0.0) in June after -0.6% (initial -0.9%), and there was strong improvement in the terms of trade.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 235.43 points (0.53%) at 44489.85

S&P E-Mini Future up 36.75 points (0.58%) at 6339.5

Nasdaq up 169.4 points (0.8%) at 20898.78

US 10-Yr yield is unchanged 0 bps at 4.4553%

US Sep 10-Yr futures are down 2/32 at 110-18

EURUSD down 0.0042 (-0.36%) at 1.1598

USDJPY up 0.7 (0.47%) at 148.59

WTI Crude Oil (front-month) up $1.23 (1.85%) at $67.61

Gold is down $6.52 (-0.19%) at $3340.50

European bourses closing levels:

EuroStoxx 50 up 79.08 points (1.49%) at 5377.15

FTSE 100 up 46.09 points (0.52%) at 8972.64

German DAX up 361.55 points (1.51%) at 24370.93

French CAC 40 up 99.91 points (1.29%) at 7822

US TREASURY FUTURES CLOSE

3M10Y -0.003, 11.24 (L: 8.244 / H: 14.503)

2Y10Y -1.914, 54.027 (L: 52.692 / H: 57.071)

2Y30Y -2.326, 109.121 (L: 107.565 / H: 113.425)

5Y30Y -0.916, 100.73 (L: 99.493 / H: 103.312)

Current futures levels:

Sep 2-Yr futures down 2/32 at 103-19.125 (L: 103-17.625 / H: 103-21.125)

Sep 5-Yr futures down 2.75/32 at 108-1.5 (L: 107-28.25 / H: 108-06.25)

Sep 10-Yr futures down 2.5/32 at 110-17.5 (L: 110-09.5 / H: 110-25)

Sep 30-Yr futures up 1/32 at 112-6 (L: 111-21 / H: 112-19)

Sep Ultra futures up 2/32 at 114-27 (L: 114-06 / H: 115-13)

MNI US 10YR FUTURE TECHS: (U5) Maintains A Softer Tone

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-13+/111-28 High Jul 10 / High Jul 3

- RES 1: 111-00 20-day EMA

- PRICE: 110-20 @ 1200 ET Jul 17

- SUP 1: 110-08+ Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures maintain a softer tone and the contract is trading closer to its recent lows. An important support at 110-17, 61.8% of the May 22 - Jul 1 bull leg, has been breached. Note that price has also traded through a trendline support at 110-24+. The line is drawn from the May 22 low. A continuation would open 110-03, the 76.4% retracement. Initial resistance is at 111-00, the 20-day EMA.

SOFR FUTURES CLOSE

Sep 25 -0.020 at 95.815

Dec 25 -0.045 at 96.075

Mar 26 -0.055 at 96.325

Jun 26 -0.055 at 96.560

Red Pack (Sep 26-Jun 27) -0.05 to -0.03

Green Pack (Sep 27-Jun 28) -0.025 to -0.015

Blue Pack (Sep 28-Jun 29) -0.015 to -0.01

Gold Pack (Sep 29-Jun 30) -0.01 to -0.005

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.03), volume: $2.771T

- Broad General Collateral Rate (BGCR): 4.33% (-0.03), volume: $1.141T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.03), volume: $1.108T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

FED Reverse Repo Operation

RRP usage slips to $193.660B this afternoon from $197.086B yesterday, total number of counterparties at 35. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

MNI PIPELINE: $2.8B PNC 3Pt Launched Recently

$10.3B to price Thursday

- Date $MM Issuer (Priced *, Launch #)

- 07/17 $6B #Morgan Stanley $2B 3NC2 +57, $1B 3NC2 SOFR+77, $3B 6NC5 +75

- 07/17 $2.8B #PNC $1B 3NC2 +52, $300M 3NC2 SOFR+73, $1.5B 11NC10 +92

- 07/17 $1B *Qatar National Bank 5Y Reg S +70

- 07/17 $500M #Symetra Life WNG 30Y +157

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform On Data...Again

Gilts underperformed Bunds for a second day Thursday, with UK data again coming in firmer than expected.

- For the second consecutive session, Gilt yields gapped higher at the open, with UK labour market data a little firmer than expected on net, including an upward revision to May payrolls and solid private regular AWE but a slightly above-expected LFS unemployment rate.

- This reducing the implied probability of remaining 2025 cuts, in turn seeing the UK short-end underperform on the day.

- Spanish and French supply helped weigh on EGBs early as well.

- However, Gilts and Bunds regained ground over the course of the session, boosted in mid-afternoon trade by a spillover rally in US Treasuries as import price data came in on the soft side. With the long-end leading the rally, curves extended a flattening move going into the cash close.

- On the day, the German curve twist flattened, with the UK's bear flattening.

- Periphery / semi-core EGB spreads closed modestly wider.

- Friday's calendar is on the lighter side, with German producer prices and Eurozone current account / construction data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.2bps at 1.862%, 5-Yr is down 0.1bps at 2.229%, 10-Yr is down 1.2bps at 2.675%, and 30-Yr is down 1.6bps at 3.198%.

- UK: The 2-Yr yield is up 5bps at 3.905%, 5-Yr is up 4.6bps at 4.088%, 10-Yr is up 1.6bps at 4.655%, and 30-Yr is up 1.3bps at 5.482%.

- Italian BTP spread up 0.3bps at 85.9bps / Spanish up 0.7bps at 61.6bps

MNI FOREX: DXY Consolidates Advance After Dipping From Fresh Recovery Highs

- The US dollar traded with a constructive tone on Thursday as markets stabilised following late volatility induced by the Trump-Powell headlines yesterday. The USD index spiked higher following the stronger set of US retail sales data, lower initial jobless claims and a much firmer-than-expected Philly Fed business outlook, allowing the DXY to reach fresh recovery highs. However, lower-than-expected import prices did immediately offset this sentiment and prompted a quick reversal of the post-data greenback advance.

- After this, currencies traded with a subdued tone - reflective of the markets taking a breather following the Trump-induced volatility – which allowed the markets to digest the last scheduled appearances for FOMC speakers before the media blackout starts this weekend. There is also a lack of meaningful data on Friday’s calendar.

- AUD (-0.65%) remains an underperformer following the weaker-than-expected jobs report overnight and the notable uptick in the unemployment rate, which have bolstered RBA easing expectations. For AUDUSD, today’s move below the 50-day EMA (intersects at 0.6490) appears meaningful, and a daily close below this average would be the first in over three months, highlighting a stronger reversal. The initial target for the move would be 0.6435 (Fib retracement) before 0.6373, the Jun 23 low and technical bear trigger.

- Greenback strength has notably weighed on the Japanese yen Thursday, with USDJPY bouncing over 200 pips from yesterday’s low to briefly trade back above 149.00. Yesterday’s highs at 149.18 capped gains and will be the short-term reference point above as markets eagerly await trade discussions between US/Japan officials and this weekend’s upper house election. Above here, attention will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high.

- GBP has moderately outperformed on Thursday, following this morning’s UK labour market data which was a little firmer-than-expected. This has allowed EURGBP to further unwind a small portion of the punchy move higher across June and July, trading back below 0.8650. It is worth noting that moving average studies are in a bull-mode position, highlighting a dominant uptrend, and initial support to watch lies at 0.8606, the 20-day EMA.

- Japan National Core CPI will print overnight before US housing starts and UMich sentiment and inflation expectations highlight the US calendar.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/07/2025 | 0600/0800 | ** | PPI | |

| 18/07/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/07/2025 | 0900/1100 | ** | Construction Production | |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 18/07/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |