US TSYS: Near Midrange After Early Post-Data Volatility

- Treasuries look to finish near opening levels after whipsawing lower/higher following this morning's data. Less headline driven volatility on the day as threats of Pres Trump threats to fire Fed Chair Powell ahead of his May 2026 term end cooled.

- Treasury futures extend lows after lower than expected weekly and continuing jobless claims, retail sales higher than expected (modest up-revisions to prior), import prices lower/export higher than expected. little react to latest in-line Business Inventories & Housing Markets index data.

- Trading desks at a loss to explain the rebound off this morning's lows, no particular headline or flow drivers as Tsys climb past yesterdays highs - back to early Tuesday levels.

- The latest weekly jobless claims report was better than expected for both initial and continuing claims, extending improvements in initial claims (and this time for a payrolls reference period) whilst continuing claims stabilize rather than extend what had been a sharp rise back in June.

- Retail sales were more solid than expected in June. It was expected that the GDP-input Control Group category would come in stronger than the other main aggregates, due in large part to anticipated weakness in auto sales, but this did not play out: Control was actually one of the weaker parts of this report relatively speaking, rising 0.5% M/M - above expectations of 0.3%, but this was offset by a 0.2pp downward rev to 0.2% in May.

- Currently, Sep'25 10Y futures -2.5 at 110-17.5 vs. 110-25 high, 10Y yld +.0020 at 4.4573%, curves remain flatter after basis hit highest levels since October 2021 late Wednesday: 2s10s currently -2.219 at 53.722, 5s30s -1.098 at 100.548.

- Cross asset: stocks firmer/new highs (SPX eminis +39.5 at 6342.75); Bbg US$ index firmer/off highs (BBDXY +3.45 at 1207.56); Gold weaker/off lows (-6.73 at 3340.40); crude firmer (WTI +1.19 at 67.57).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Safe Haven Raises Rates in Lead-Up to FOMC Policy Annc

- Rising Middle East tensions included chances the US will join the war lent to the second half risk-off support for Treasuries Tuesday. Otherwise, markets await Wednesday's FOMC policy announcement including a Summary of Economic Projections (Dots).

- Pres Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there - We are not going to take him out (kill!), at least not for now. But we don’t want missiles shot at civilians, or American soldiers. Our patience is wearing thin. Thank you for your attention to this matter!"

- We expect that the June FOMC meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections.

- Cross asset update: stocks ebbed in the second half (SPX eminis -44.75 at 6045.0), West Texas crude climbed to early July 2024 highs (WTI +3.39 at 75.16), while Bbg US$ index climbed to June 11 highs (BBDXY +6.43 at 1209.02).

- Tsy Sep'25 10Y futures trades +12.5 at 110-28 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves flatter, 2s10s -4.250 at 43.309, 5s30s -1.837 at 90.209. 10Y yield at 4.3849% vs. 4.3770% low.

FED: Statement: Uncertainty Still Elevated (4/4)

Going paragraph by paragraph through the previous (May) statement opening paragraphs in italics:

- The opening paragraph of the Statement may as usual be marked-to-market, but the previous edition’s description of the economy largely still stands. We would be surprised if the Fed described labor market conditions as anything but “solid”, or inflation as anything but “somewhat elevated”.

- A change to either would almost certainly lean to the dovish side, with recent inflation data surprising to the downside and broad labor market indicators cooling, but it’s unlikely the FOMC would want to send such a signal this month.

- There probably hasn’t been enough evidence in the “hard” data to refer to economic activity as running at anything but a “solid” pace, though a tweak here to something like “moderate” is possible and probably not impactful. There may also be an adjustment of the language on “swings in net exports”, though this continues to be useful given the inventory/net export swings between Q1 and Q2.

- With a tentative US-China trade deal in place, it’s likely that the second paragraph will remove references to uncertainty and risks having risen, merely saying perhaps that they are/remain elevated.

- The Fed could at some point alter its assessment of the balance of risks to suggest that they are concerned that one of the dual mandate goals needs to be addressed at the potential expense of the other, but that would require much clearer evidence in the data.

- For an FOMC that is waiting to see the impact of tariffs and other policy shifts, even as it maintains its overall easing bias, a shift in forward rate guidance (“in considering the extent and timing of additional adjustments…”) looks unlikely at this juncture.

- No dissents are expected. In the Implementation Note, no changes to the administered rates are expected.

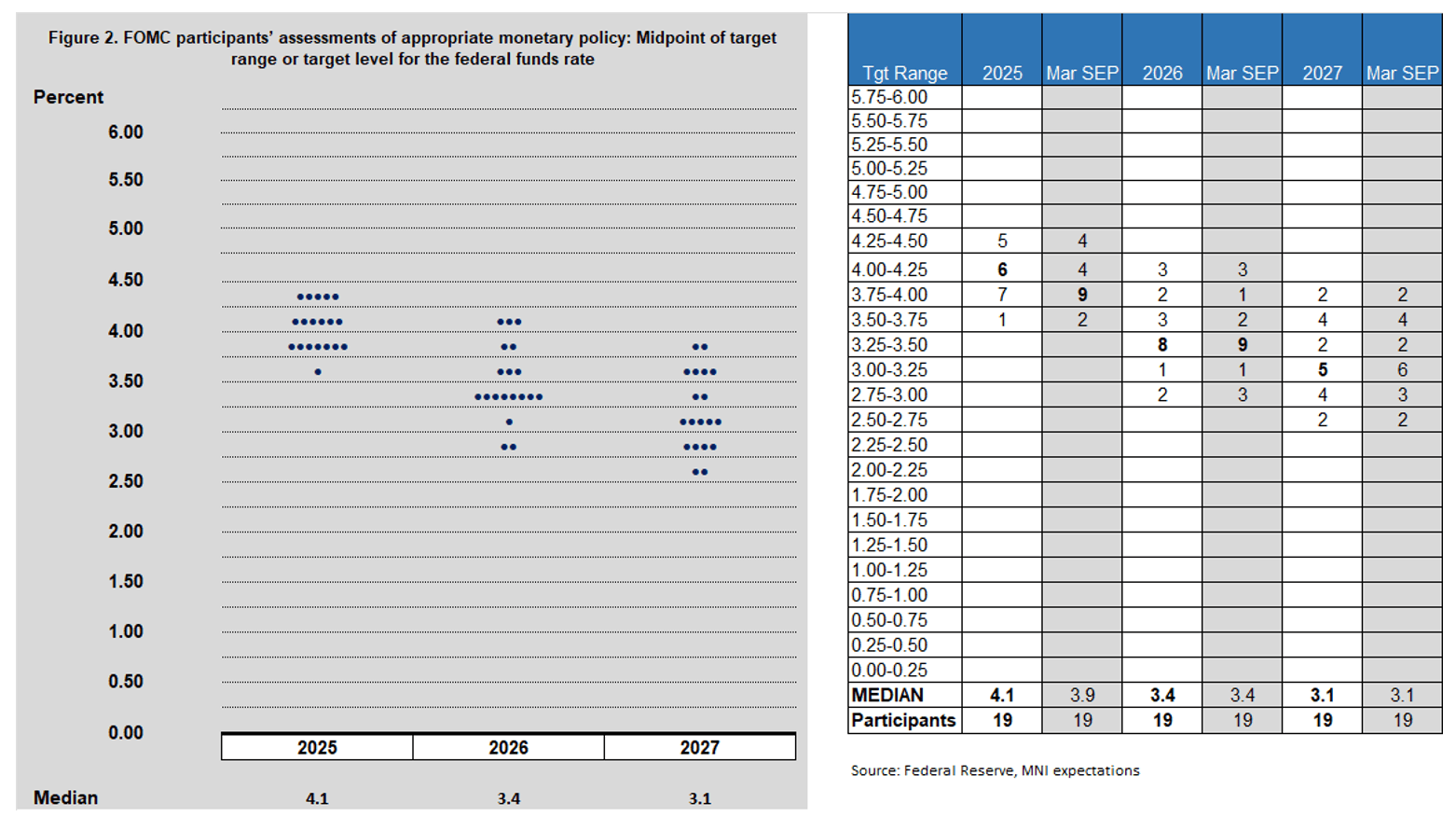

FED: Summary Of Economic Projections: Slightly More Patient Rate Path (3/4)

2025: Developments since the March projections point to a slight drift higher in the 2025 Fed funds rate projection, which are likely to push up the median to 4.125% (one 25bp cut) from 3.875% (two 25bp cuts). There is a basically 50/50 split among analysts about whether or not the dot will shift up.

- The split in March was fairly close: 8 of 19 participants saw rates ending the year at 4.125% or 4.375%, with 9 at 3.875% and 2 at 3.625%. This means that only 2 of the 11 lower-rate participants have to shift up their dots to 4.175% or above, and we think that threshold will be met, if only barely. We know that a few participants haven’t changed their minds since March (SF’s Daly still sees 2 cuts, Atlanta’s Bostic still sees 1), but overall FOMC participants have sounded increasingly cautious on the outlook due largely to April’s larger-than-expected tariff announcements, and certainly, none have sounded more dovish as a result.

- We think that the top 8 dots will stay more or less where they are, possibly with some upward drift toward a full-year “hold”, while June’s bottom dot may prove lonesome at 3.625% (possibly Waller if he still sees potential for three cuts this year).

- Our Instant Answers will be watching the distribution of the dots, while also eyeing the somewhat remote possibility that a hawkish FOMC participant pencils in a 2025 rate hike.

2026-27: A higher 2025 median doesn’t necessarily mean the 2026-2027 dots will shift higher in tandem.

- The 3.375% 2027 median in the March projections was quite solid: 13 of 19 members were there or below. A few dots may drift up, but it’s likely that the core of the Committee still has an easing bias, and that the decision to be more patient on cuts in 2025 doesn’t mean that the longer-run path needs to change dramatically. If combined with a 25bp rise in the 2025 median, an unchanged 2026 median would imply 75bp of cuts next year, and probably perceived dovishly as it would suggest that the Committee still sees the near-term inflation impact of tariff inflation as being “transitory”.

- Regardless of the 2025-26 dots, we would expect the 2027 median to near the longer-run dot as usual for an outer-year projection. As such, 3.1% is likely to be the median again.

Longer-Run: We don’t expect an upward shift in the longer-run dot at this meeting. This median shifted up in each quarterly projection between the start of 2024 and end of 2025, but was on hold in March at 3.00%.

- It would take 3 of 11 participants to shift their dots higher, hardly an insurmountable bar: there are currently 3 dots on 3.00%, with 4 just below that at 2.875% and a further 4 at 2.50-2.625%. However given broader uncertainty it’s likely that participants will wait for another quarterly meeting to move this higher again. The next increase would bring the longer-run rate back above 3.00% for the first time since March 2016, and would be up from the trough of 2.40% in 2022.