US DATA: Jobless Claims Surprise Lower, Including Payrolls Ref Week For Initial

Jul-17 12:45

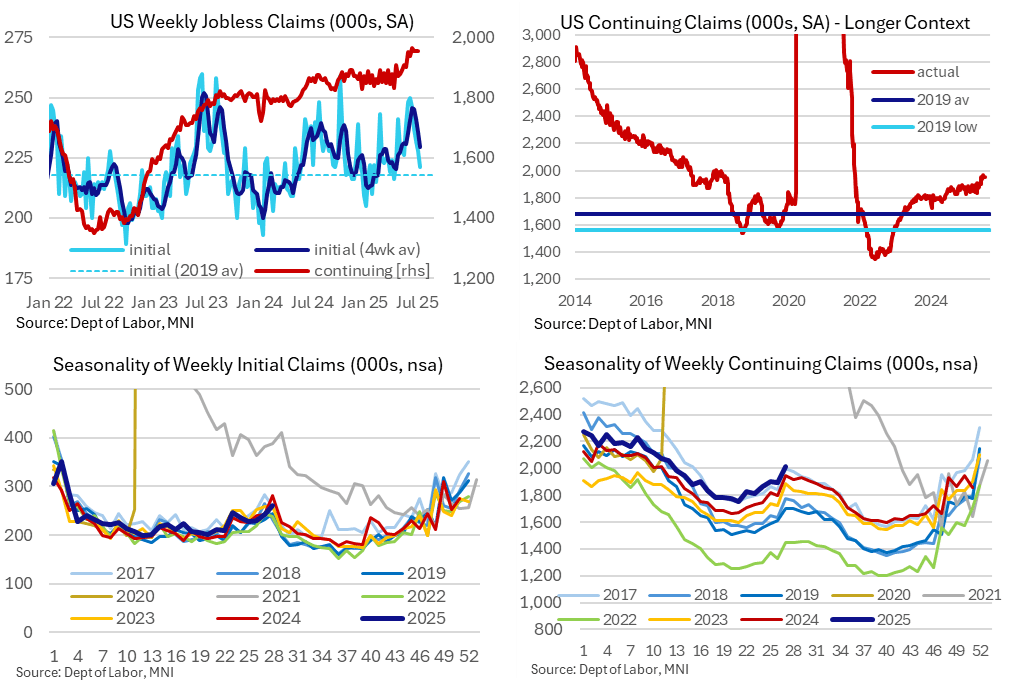

The latest weekly jobless claims report was better than expected for both initial and continuing claims, extending improvements in initial claims (and this time for a payrolls reference period) whilst continuing claims stabilize rather than extend what had been a sharp rise back in June. It broadly continues to chime with a 'low firing, low hiring' labor market.

- Initial jobless claims: 221k (sa, cons 233k) in the week to Jul 12 – a payrolls reference period – after a marginally upward revised 228k (initial 227k).

- It sets up a more favorable comparison with last month’s payrolls report, with the 221k vs 246k a month ago for back more in keeping with the 226k in May and 216k in April.

- It’s a fifth consecutive weekly decline for the weekly rate whilst the four-week average also continues to trend lower with 230k after 236k the week prior and 246k a month ago at what was its highest since Aug 2023.

- Continuing claims: 1956k (sa, cons 1965k) in the week to Jul 5 after a downward revised 1954k (initial 1965k).

- It extends some stabilization in continuing claims after what had been a swift climb to a new 3+ year high of 1964k in mid-June.

- The claims rate remains at a well-centered 1.3%, with 1.28% for three weeks now, having tipped into 1.3% territory back in mid-May for the first time since Dec 2021.

- Non-seasonally adjusted levels tell a familiar story: initial claims are within non-pandemic ranges for the time of year, and of some note now a little below the 2024 level, whilst continuing claims are right at the top of the ‘normal’ ranges.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Updated Roll Pace

Jun-17 12:41

Sept is front for the US, for now June is still the most active contract on this side of the Pond. Spreads of both Sides of the Atlantic dominates ahead of Triple Witching Friday.

US:

- SPX: 59%.

- NDX: 52%.

- DOW: 51%.

EU:

- VGA: 50%.

- DAX: 41% (below Pace).

- FTSE: 67%.

US TSYS: Post-Retail Sales, Import/Export Data React

Jun-17 12:34

- Treasuries extend gains then quickly revert after latest Retail Sales come out lower than estimated, priors down-revised, import/export prices steady to lower.

- Tsy Sep'25 10Y futures trades +10.5 at 110-26 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves mixed, 2s10s -1.014 at 46.545, 5s30s +.285 at 92.228. 10Y yield slips to 4.3770% low.

- Cross asset: Stocks remain weaker (SPX eminis -26.75 at 6063.0), Gold mildly higher at 3388.00, Bbg US$ index little changed at 1202.44 -0.15.

EURIBOR OPTIONS: Call Spread vs Put

Jun-17 12:34

ERZ5 98.25/98.50cs vs 98.00p, bought the cs for 2.25 in 5k.

Trending Top

Apr-24 20:29