US DATA: June Retail Sales Surge Led By Ex-Control Group Categories

Jul-17 12:51

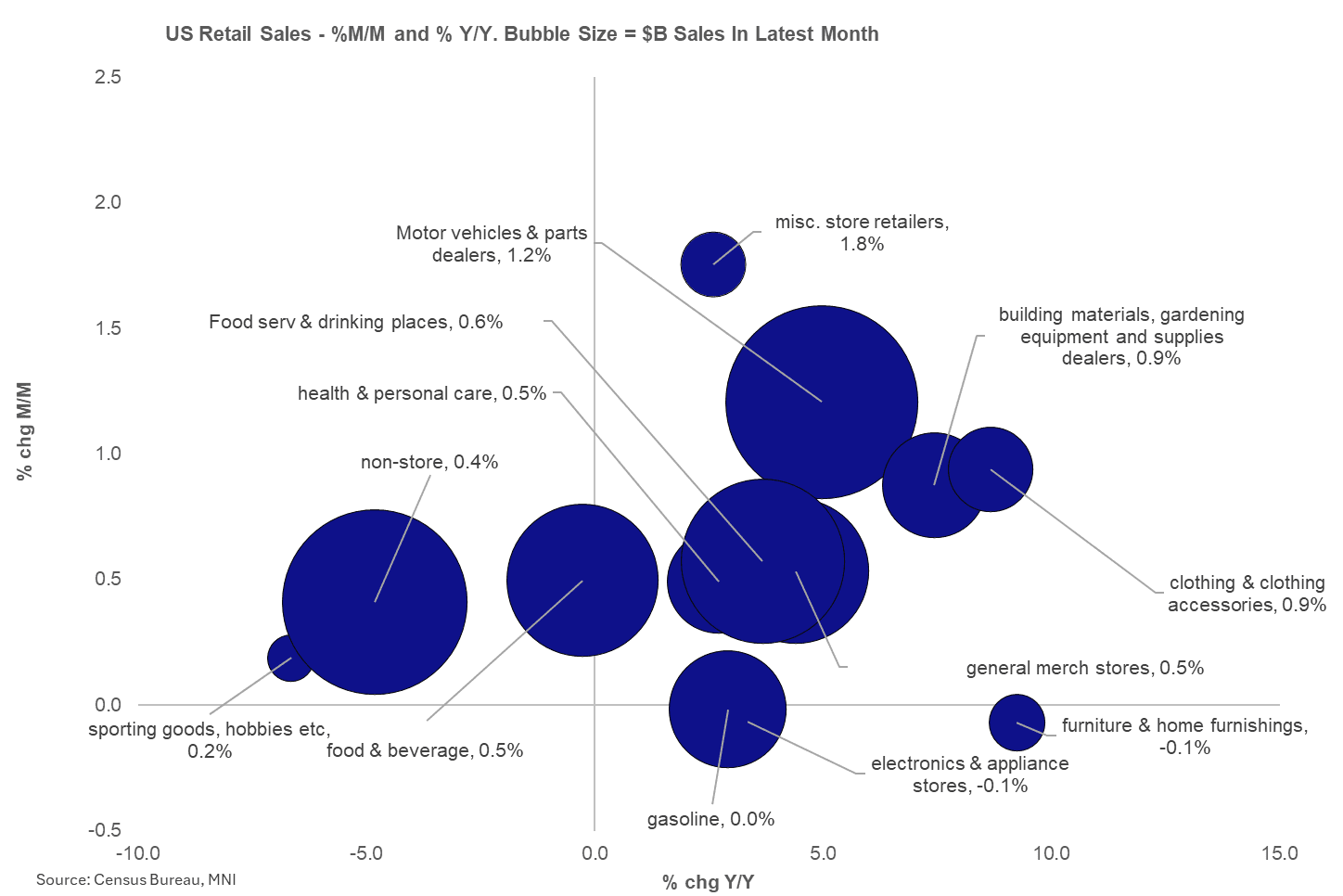

Retail sales were more solid than expected in June.

- It was expected that the GDP-input Control Group category would come in stronger than the other main aggregates, due in large part to anticipated weakness in auto sales, but this did not play out: Control was actually one of the weaker parts of this report relatively speaking, rising 0.5% M/M - above expectations of 0.3%, but this was offset by a 0.2pp downward rev to 0.2% in May.

- And - surprisingly - each of the ex-control group retail sales categories: motor vehicles (1.4% M/M after -4.2%; most had expected flat/negative, with the broader motor vehicles/parts learers rising 1.2%), building/gardening materials (0.9% after -2.7%), gasoline (0.0% after -1.3%) and food services/drinking places (0.6% after -0.1%) - all recovered after May contractions (albeit gasoline may have been a little on the low side of expectations).

- That meant headline sales came in well above-expected at 0.6% M/M (0.1% consensus), with May unrevised at -0.9%. But ex-auto/gas impressed at 0.6% (0.3% expected, 0.1pp upward revision to May to 0.0%) and ex-auto 0.5% (0.3% expected, 0.1pp upward revision to May to -0.2%).

- In notable major categories, non-store retail grew robustly once more at 0.4% M/M (0.4% prior; has risen for 5 consecutive months), with clothing stores, miscellaneous store retailers (1.8%) and general merchandise stores (0.5%) seeing another month of growth, and food and beverage (0.5%) and health and personal care (0.5%) up after a contractionary May.

- Only two categories saw M/M declines: electronics and furniture stores both saw modest falls in sales (-0.1% after negative Mays).

- Overall retail sales have now recovered a significant part of the dip since March's tariff front-running surge, with Control Group and Ex-autos/gas setting new all-time highs (all in SA/nominal terms),

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA DATA: StatsCan Boosts CPI Weight Of Food, Lowers Housing

Jun-17 12:45

- StatsCan's annual re-weighting of CPI basket Tues increases share for food to 16.9% from 16.7% last year, and up from 16.2% in 2020.

- Shelter increases to 29.4% from 29.2%, but below 30% in 2020.

- Transportation unchanged at 16.9%, up from 16% in 2020.

- Overall services basket has climbed to 55.6% from 51.2% in 2020; goods declines to 44.5% from 48.8%.

- Reweighting comes at a time when BOC has been more concerned about elevated core inflation.

EQUITIES: Updated Roll Pace

Jun-17 12:41

Sept is front for the US, for now June is still the most active contract on this side of the Pond. Spreads of both Sides of the Atlantic dominates ahead of Triple Witching Friday.

US:

- SPX: 59%.

- NDX: 52%.

- DOW: 51%.

EU:

- VGA: 50%.

- DAX: 41% (below Pace).

- FTSE: 67%.

US TSYS: Post-Retail Sales, Import/Export Data React

Jun-17 12:34

- Treasuries extend gains then quickly revert after latest Retail Sales come out lower than estimated, priors down-revised, import/export prices steady to lower.

- Tsy Sep'25 10Y futures trades +10.5 at 110-26 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves mixed, 2s10s -1.014 at 46.545, 5s30s +.285 at 92.228. 10Y yield slips to 4.3770% low.

- Cross asset: Stocks remain weaker (SPX eminis -26.75 at 6063.0), Gold mildly higher at 3388.00, Bbg US$ index little changed at 1202.44 -0.15.