US DATA: Subdued Import Prices In June Despite A Rare Increase From China

The US terms of trade saw a sizeable improvement in June from a combination of stronger than expected export prices and weaker than expected import prices. The latter came despite stronger China import prices in a partial correction after what had looked like some implicit taking of a tariff hit in April and May. Looking specifically at M/M pressures in June, the relative strength in consumer goods prices look at odds with both yesterday’s core PPI figures and today’s import prices.

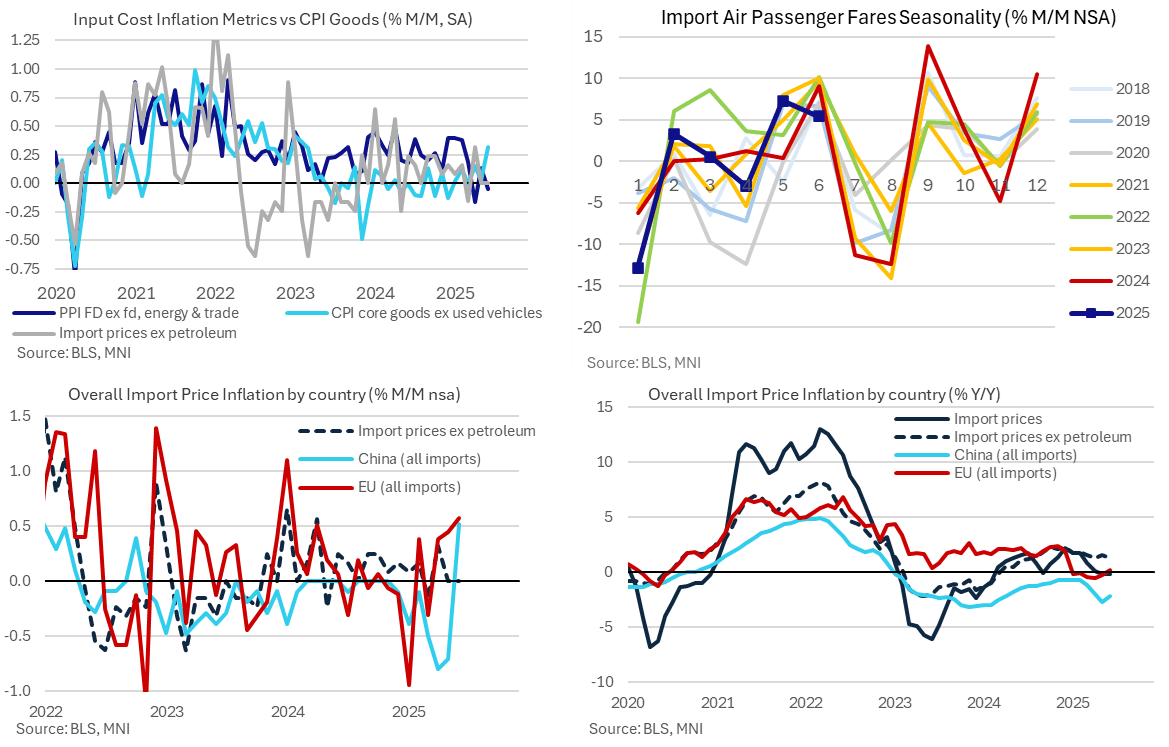

- Import price inflation was softer than expected in June at 0.1% M/M (cons 0.3) after a downward revised -0.4% (initial 0.0%) in May.

- Import prices ex petroleum also surprised lower with 0.0% M/M (cons 0.2) after a downward revised 0.0% (initial 0.2%).

- The breakdown of import prices by major country was interesting, especially for China where they increased 0.5% M/M for the strongest rise since Dec 2021 (and the first increase since Oct 2022).

- It does however follow outsized declines of -0.8% M/M in April and -0.7% M/M in May in what had been signs that Chinese exporters were implicitly taking some of the tariff hit.

- China remains a source of deflation on a trend basis though, with imports prices at -2.2% Y/Y.

- Combined with surprisingly firm export prices, at 0.5% M/M (cons 0.0) in June after -0.6% (initial -0.9%), and there was strong improvement in the terms of trade.

- As for core PCE implications, passenger fares from import prices increased a non-seasonally adjusted 5.4% M/M in June vs an average of 9.7% M/M in the previous four Junes. We very roughly guess that could see core PCE estimates trimmed perhaps 1 or 2bps from a median marginally under 0.30% M/M although it depends on what was already penciled in as there had already been signs of weakness in airfares in other inflation data. We wouldn't be surprised if the perceived impact was even smaller.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US MAY INDUSTRIAL PROD -0.2%; CAP UTIL 77.4%

- MNI: US MAY INDUSTRIAL PROD -0.2%; CAP UTIL 77.4%

- US APR IP REV TO +0.1%; CAP UTIL REV 77.7%

- US MAY MFG OUTPUT +0.1%

EURIBOR OPTIONS: Latest Call Ladders

- ERZ5 98.25/98.50/98.625c ladder, bought for 3.75 in 3.5k.

- ERZ5 98.25/98.375/98.50c ladder, bought for half in 2k.

SOFR OPTIONS: Post-Data Flow

Call spread selling, conditional curve plays while underlying futures continue to scale back from post-data highs. White pack (SFRM5-SFRH6) trades steady to -.005. Projected rate cut pricing consolidates slightly from earlier levels (*) as follows: Jun'25 at 0.0bp, Jul'25 at -3.1bp (-3.6bp), Sep'25 at -18.2bp (-19.5bp), Oct'25 at -31.1bp (-32.6bp), Dec'25 at -47.3bp (-48.8bp).

- -10,000 0QZ5 97.50/97.62 call spds, 1.75 vs. 96.73/0.05%

- +2,500 SFRZ5 96.37/96.75 call spds vs. 0QZ5 97.25/97.50 call spd, 1.5 net/steepener

- +2,500 SFRN5 95.37/95.68 put spds, .37

- -4,000 SFRU5 95.68/95.81/96.25/96.37 call condors, 5.25 ref 95.875