MNI ASIA OPEN: SCOTUS Opinion Days, FOMC Jan Minutes Focus

EXECUTIVE SUMMARY

- MNI TARIFFS: Next Slate Of SCOTUS Opinion Days Announced

- MNI US DATA: Latest CPI Trends: Core CPI Run Rates In Line With 2.5% Y/Y

- MNI US INFLATION: Sequential CPI Pressures Softer Than Expected

US

MNI TARIFFS: Next Slate Of SCOTUS Opinion Days Announced

"*SUPREME COURT SAYS FEB. 20 TO BE OPINION DAY AMID TARIFF WAIT" ... "*SUPREME COURT ALSO SETS FEB. 24 AND 25 AS DAYS FOR OPINIONS" Bloomberg. As with previous instances in January, these are simply SCOTUS opinion days. The court does not reveal in advance what opinions it will be releasing. As such, markets will have to wait for the sessions themselves to determine if a tariff ruling is on the agenda, usually from 10ET onwards.

MNI MACRO ANALYSIS: VAT Plans Raise Focus on Japanese Fiscal

Executive Summary: Financing the JPY5trn food consumption tax suspension with proceeds from the FX special account would likely open up gaps in the general budget. This leaves the Japanese finance ministry with three options: Plug the gap through increasing the efficiency of the tax base and expenditure, net liquidation of parts of the FX special account, or higher JGB issuance through the backdoor.

NEWS

MNI US: DHS Set To Shut Down At Midnight, No Clear Offramp To ICE Standoff

The Trump administration announced yesterday that it is ending its deployment of federal immigration agents in Minnesota. The move was welcomed by Democratic leaders in the state, but it does not appear to be enough to prevent a shutdown of the Department of Homeland Security at midnight tonight.

MNI US-RUSSIA: Kremlin: Next Trilateral Talks In Geneva, 17-18 Feb

Kremlin spox Dmitry Peskov confirms that the next round of Russia-Ukraine-US peace talks will take place on 17-18 February in Geneva, Switzerland. The Russian delegation will be led by Vladimir Medinsky, an aide to President Vladimir Putin. Ukrainian President Volodymyr Zelenskyy indicated on 12 Feb that talks could take place in the US, but it appears a neutral venue was preferred.

US TSYS

MNI US TSYS: Softer CPI Metrics Buoys Tsys, Rate Cut Pricing Gains Slightly

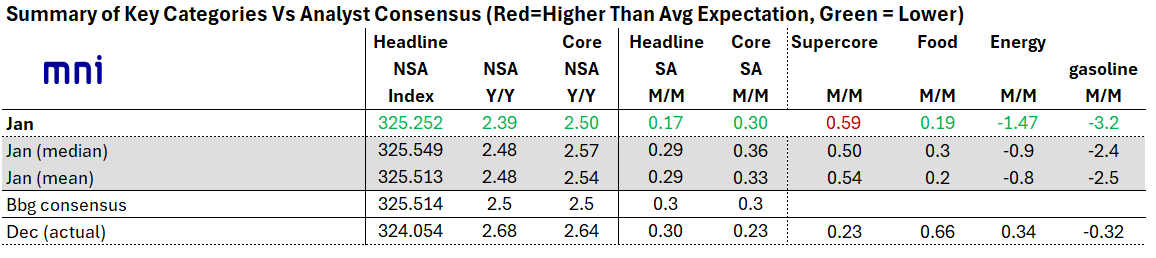

- Treasuries look to finish stronger/near highs - climbing to best levels since early December after this morning's CPI inflation measure for January came out softer than expected, though an upside beat in supercore (more on which in a moment). The Y/Y changes for headline and core CPI came in line/a little softer than expected.

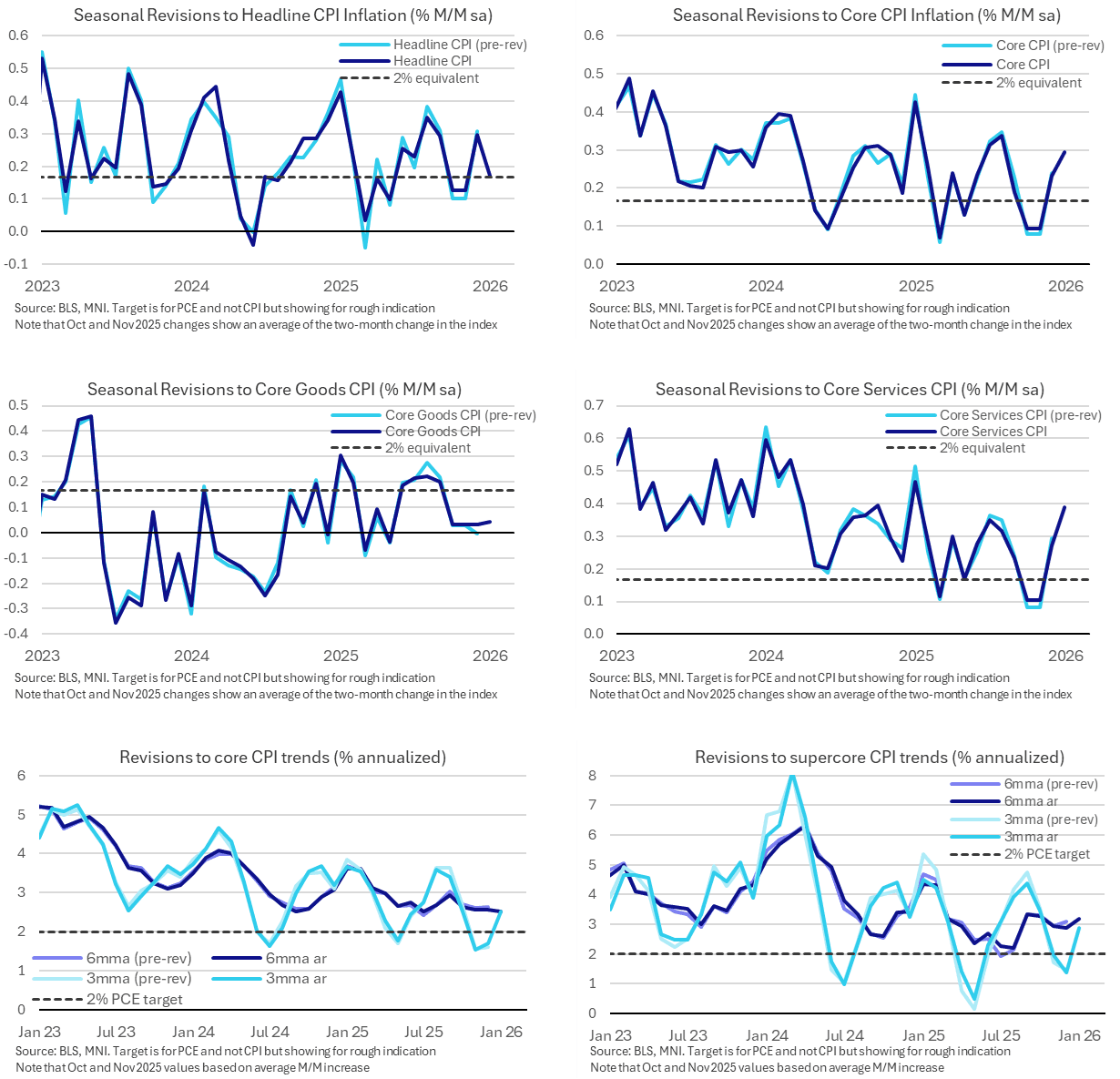

- Core CPI 3-month: 2.52% annualized over the latest three months to January, following 1.70% to December (1.61% first reported) and 3.42% to September (3.64%).

- TYH6 trades 113-06 (+12.5) vs. 113-07.5 high - breaching 113-04 (76.4% of the Nov 25 - Jan 20 bear leg) and opening up 113-11 as next resistance, the Dec 1 ‘25 high.

- Curves mildly steeper after this morning's softer than expected CPI data. In turn - projected rate cut pricing gain slightly vs. late Thursday lows (*): Mar'26 at -2.6bp (-1.6bp), Apr'26 at -7.6bp (-6.6bp), Jun'26 at -21.5bp (-19.2bp), Jul'26 at -32.1bp (-28.6bp).

- The dollar index tilts very marginally in the red Friday, allowing the DXY to have a fourth consecutive session of consolidating price action following the impressive 0.8% move south on Monday. Greenback weakness has been most notable against the Japanese yen following Japan’s election last Sunday.

- Look ahead: US markets closed Monday for Presidents' Day holiday (Globex early close at 1300ET), Tuesday sees weekly ADP NER Pulse and NAHB Housing Market Index. Supreme Court announces Feb 20, 24 and 25 as next opinion days (appr 1000ET).

OVERNIGHT DATA

MNI US INFLATION: Sequential CPI Pressures Softer Than Expected

January brought softer-than-expected CPI data across the board for the most part, though an upside beat in supercore (more on which in a moment). The Y/Y changes for headline and core CPI came in line/a little softer than expected.

- Headline % M/M was 0.17% vs 0.29% unrounded MNI median, with core at 0.30% below the 0.36% median.

- On the headline side, energy and food were each in softer-than-expected territory M/M, helping drive the downside "miss".

- Note that while the NSA series were not revised in this report (so prior Y/Y readings were unchanged), the annual revision of seasonal factors means December (prior) % M/M readings in this table have been slightly revised.

MNI US DATA: Only Modest CPI Seasonal Adjustment Revisions

- Core CPI at 0.30% M/M in January after 0.23% M/M in Dec (0.24% M/M first reported).

- Minimal revisions from the new seasonal adjustment factors, with headline and core CPI a touch weaker in Dec, slightly stronger over that two-month average across Oct-Nov and then weaker in Sep.

- Within core, services led the downward revision to Dec (-0.02pps to 0.27% M/M) whilst core goods was revised 0.03pps higher but only to 0.03% M/M.

- The new factors appear to have slightly dampened down on Jan residual seasonality patterns, with the Jan 2025 increase trimmed from 0.45% M/M to 0.43% M/M, led by core services being trimmed by 0.05pps for its most across the year.

MNI US DATA: Latest CPI Trends: Core CPI Run Rates In Line With 2.5% Y/Y

- Core CPI 3-month: 2.52% annualized over the latest three months to January, following 1.70% to December (1.61% first reported) and 3.42% to September (3.64%).

- 6-month: 2.52% annualized over the latest six months to January whilst the run rate to Dec was trimmed slightly from 2.63% to 2.56%.

- Latest run rates are in line with the 2.50% Y/Y in January, as always taken from the NSA series and so unrevised with this update. That has cooled from 2.64% in December for a fresh low since Mar 2021 but of course is still biased lower due to treatment of rent series during the government shutdown.

- Supercore CPI meanwhile stood at 2.88% annualized over the three months to Jan after 1.38% in Dec (1.46% initially) and 4.38% in Sept (vs 4.75%).

- The six-month supercore rate increased to 3.2% annualized from a downward revised 2.9% (3.1% initially) for its highest since October.

- All of the above trend rates are reliant on interpolating the October index level.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 52.04 points (-0.11%) at 49389.92

S&P E-Mini Future down 12 points (-0.18%) at 6839.75

Nasdaq down 90.6 points (-0.4%) at 22510.38

US 10-Yr yield is down 5 bps at 4.0483%

US Mar 10-Yr futures are up 13/32 at 113-6.5

EURUSD down 0.0004 (-0.03%) at 1.1866

USDJPY down 0.03 (-0.02%) at 152.73

WTI Crude Oil (front-month) down $0.13 (-0.21%) at $62.72

Gold is up $106.11 (2.16%) at $5029.23

European bourses closing levels:

EuroStoxx 50 down 26.06 points (-0.43%) at 5985.23

FTSE 100 up 43.91 points (0.42%) at 10446.35

German DAX up 62.19 points (0.25%) at 24914.88

French CAC 40 down 28.82 points (-0.35%) at 8311.74

US TREASURY FUTURES CLOSE

Curve update:

3M10Y -3.796, 36.923 (L: 36.025 / H: 43.365)

2Y10Y +0.477, 64.486 (L: 63.614 / H: 66.155)

2Y30Y +1.505, 128.991 (L: 126.588 / H: 131.422)

5Y30Y +1.967, 109.127 (L: 106.031 / H: 109.752)

Current futures levels:

Mar 2-Yr futures up 3.75/32 at 104-14.5 (L: 104-10.125 / H: 104-15)

Mar 5-Yr futures up 9/32 at 109-23 (L: 109-11.25 / H: 109-23.25)

Mar 10-Yr futures up 13.5/32 at 113-7 (L: 112-21 / H: 113-07.5)

Mar 30-Yr futures up 18/32 at 117-27 (L: 116-30 / H: 117-30)

Mar Ultra futures up 19/32 at 120-23 (L: 119-20 / H: 120-27)

MNI US 10YR FUTURE TECHS: (H6) Fresh Trend High

- RES 4: 113-29+ High Oct 17 ‘25 high and a key M/T resistance

- RES 3: 113-22+ High Nov 22 ‘25 and a key resistance

- RES 2: 113-11 High Dec 1 ‘25

- RES 1: 113-07+ High Feb 13

- PRICE: 113-07 @ 1210 ET Feb 13

- SUP 1: 112-20 High Feb 11

- SUP 2: 112-07/03 20- and 50-day EMA points

- SUP 3: 111-26 Low Feb 9

- SUP 4: 111-13+ Low Feb 3

Treasuries maintain a firm tone and have traded to a fresh cycle high today. This reinforces the current bull theme, marking an extension of the uptrend that started on Jan 20. The contract has breached 113-04, 76.4% of the Nov 25 - Jan 20 bear leg. This opens 113-11 next, the Dec 1 ‘25 high. Initial firm support to watch is 112-07, the 50-day EMA. A S/T pullback would be considered corrective and would unwind an overbought trend reading.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 +0.005 at 96.370

Jun 26 +0.030 at 96.595

Sep 26 +0.050 at 96.840

Dec 26 +0.070 at 96.965

Red Pack (Mar 27-Dec 27) +0.080 to +0.085

Green Pack (Mar 28-Dec 28) +0.070 to +0.080

Blue Pack (Mar 29-Dec 29) +0.060 to +0.065

Gold Pack (Mar 30-Dec 30) +0.050 to +0.060

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.65% (+0.00), volume: $3.205T

- Broad General Collateral Rate (BGCR): 3.63% (+0.01), volume: $1.342T

- Tri-Party General Collateral Rate (TCR): 3.63% (+0.01), volume: $1.318T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $97B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $196B

FED Reverse Repo Operation New Low

RRP usage retreats to lowest level since early 2021 at $0.377B with 3 counterparties this afternoon vs. $2.844B Thursday. Compares to prior low on December 12 low of $0.838B; last year's highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Roundup

$3.8B Priced Friday, $56.45B total on week:

- Date $MM Issuer (Priced *, Launch #)

- 02/13 $3.8B *Tract Capital 5NC2 5%875

- $4.95B Priced Thursday

- 02/12 $2.5B *Royal Caribbean $1.25B 7Y +92, $1.25B 12Y +117

- 02/12 $1.25B *Citadel Finance $750M 3Y +140, $500M 5Y +165

- 02/12 $600M *Concentrix 3Y +300

- 02/12 $600M *Akbank PerpNC5.5 7.95%

MNI BONDS: EGBs-GILTS CASH CLOSE: Rally Continues, Cementing Weekly Bull Flattening

Long-end European yields fell for a 4th consecutive session Friday, cementing a solid bull flattening move for the week.

- The key focus for the session was US inflation, and a softer-than-expected set of data triggered a rally in Treasuries that spilled over into Europe.

- Bunds underperformed Gilts overall however. German Defence Minister Klingbeil triggered a late sell-off when he did not rule out an exemption made to the debt brake rule for the country's raw material fund.

- Core EGBs gained on the day nonetheless; periphery/semi-core EGB spreads widened modestly.

- On the week, both the UK (2Y yield -3bp, 10Y -10bp) and German (2Y -5bp, 10Y -9bp) curves bull flattened.

- Ratings reviews for Austria (Moody's) and the Netherlands (also Moody's) feature after the cash close.

- UK macro takes centre stage next week, with the latest round of labour market, inflation, and retail sales data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 2.036%, 5-Yr is down 2.8bps at 2.337%, 10-Yr is down 2.4bps at 2.755%, and 30-Yr is down 1.7bps at 3.432%.

- UK: The 2-Yr yield is down 1bps at 3.593%, 5-Yr is down 3bps at 3.825%, 10-Yr is down 3.6bps at 4.416%, and 30-Yr is down 3.5bps at 5.223%.

- Italian BTP spread up 0.4bps at 60.9bps / French OAT up 1.2bps at 59.2bps

MNI FOREX: USDJPY Set to Post Near 3% Weekly Decline

- Friday’s session was an uneventful one for currencies, with the more stable risk backdrop having little impact across the G10 and the eagerly awaited US inflation data failing to spark any momentum for the major pairs. January brought softer-than-expected US CPI data across the board for the most part, though an upside beat in supercore. The Y/Y changes for headline and core CPI came in line/a little softer than expected.

- The dollar index tilts very marginally in the red Friday, allowing the DXY to have a fourth consecutive session of consolidating price action following the impressive 0.8% move south on Monday.

- Greenback weakness has been most notable against the Japanese yen following Japan’s election last Sunday. PM Takaichi’s convincing win has buoyed market hopes of both a more stable political backdrop and a more measured fiscal approach to policy. The stabilisation for JGB’s has fostered a substantial yen recovery, which has been exacerbated by positioning dynamics and thoughts that the BOJ’s March meeting could be live.

- After rallying at Monday’s open to 157.76, the aggressive selloff took us to within 17pips of the key 152.10 support and bear trigger. Despite an initial recovery Friday, spot has edged back to 152.80 ahead of the close, with the pair remaining to look vulnerable. The pre-October election close is at 147.47 and remains a significant downside target.

- AUDUSD has underperformed Friday to trade back below 0.7100, with this week’s rally falling just shy of the 2023 highs at 0.7158. Fresh cycle highs this week keep bullish conditions firmly intact, with dips remaining technically corrective at this juncture.

- Another notable mover this week has been the resilient Swiss Franc, with EURCHF printing below 0.9100 for the first time since the removal of the floor in 2015. Analyst notes have been surprisingly bullish CHF given the recent extremes and historical precedent for the SNB to comment on the strong levels of the franc, with one bank forecasting a move to 0.8700.

- Japan GDP and Eurozone industrial production data highlight a light calendar Monday, where volumes may be dampened due to China, the US and Canada out for national holidays.

MONDAY-TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/02/2026 | 0700/0800 | ** | Unemployment | |

| 16/02/2026 | 1000/1100 | ** | EZ Industrial Production | |

| 16/02/2026 | - | ECB Lagarde and Cipollone at Eurogroup meeting | ||

| 16/02/2026 | 1315/0815 | ** | CMHC Housing Starts | |

| 16/02/2026 | 1325/0825 | Fed's Michelle Bowman | ||

| 16/02/2026 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0900/1000 | Foreign Trade | ||

| 17/02/2026 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI | |

| 17/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 17/02/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/02/2026 | 1745/1245 | Fed Governor Michael Barr | ||

| 17/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 17/02/2026 | 1930/1430 | San Francisco Fed's Mary Daly | ||

| 18/02/2026 | - | Reserve Bank of New Zealand Meeting | ||

| 18/02/2026 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 18/02/2026 | 0030/1130 | *** | Quarterly wage price index | |

| 18/02/2026 | 0100/1400 | *** | RBNZ official cash rate decision |