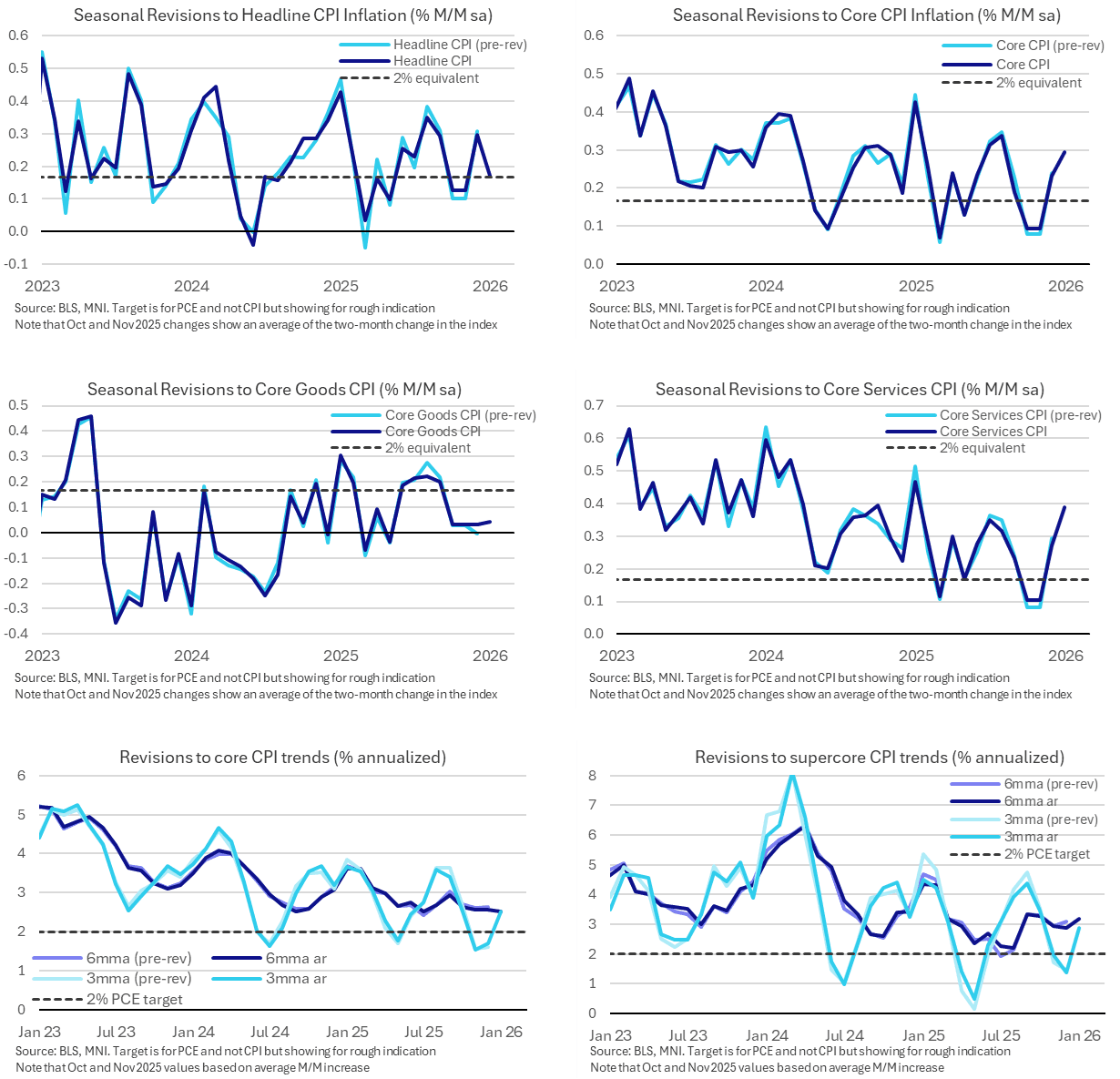

US DATA: Latest CPI Trends: Core CPI Run Rates In Line With 2.5% Y/Y

- Core CPI 3-month: 2.52% annualized over the latest three months to January, following 1.70% to December (1.61% first reported) and 3.42% to September (3.64%).

- 6-month: 2.52% annualized over the latest six months to January whilst the run rate to Dec was trimmed slightly from 2.63% to 2.56%.

- Latest run rates are in line with the 2.50% Y/Y in January, as always taken from the NSA series and so unrevised with this update. That has cooled from 2.64% in December for a fresh low since Mar 2021 but of course is still biased lower due to treatment of rent series during the government shutdown.

- Supercore CPI meanwhile stood at 2.88% annualized over the three months to Jan after 1.38% in Dec (1.46% initially) and 4.38% in Sept (vs 4.75%).

- The six-month supercore rate increased to 3.2% annualized from a downward revised 2.9% (3.1% initially) for its highest since October.

- All of the above trend rates are reliant on interpolating the October index level.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ENERGY SECURITY: US Withdrawing Personnel from Mideast Bases: Reuters

The US is withdrawing some personnel from key bases in the Middle East as a precaution given heightened regional tensions, a U.S. official told Reuters.

- The disclosure follows remarks by a senior Iranian official who told Reuters earlier on Wednesday that Tehran had warned neighbours hosting U.S. troops that it would hit American bases if Washington strikes.

- This, coupled with Trump’s comments yesterday that citizens of the US and its allies should get out of Iran and the comment that help is on its way to protesters, raise further speculation that the U.S may be planning a strike on the Islamic Republic.

- While crude prices are already carrying a geopolitical risk premium, that is set to jump if the U.S or Israel strikes Iran.

- In contrast to the symbolic response from Iran after U.S strikes on its nuclear facilities, the regime in Tehran is likely to be more aggressive in targeting US military infrastructure in the Gulf.

- These, located in oil producers such as Iraq, Kuwait, Saudi Arabia, Bahrain, Qatar, the UAE, and Oman, raise the risk that oil and gas infrastructure could be caught in the crossfire.

- It also raises the stakes for a worst-case scenario where Iran tries to block the Straits of Hormuz, a chokepoint for 20% of global oil flows. Should this happen, it would prompt a stronger response from the US fifth fleet located in Bahrain.

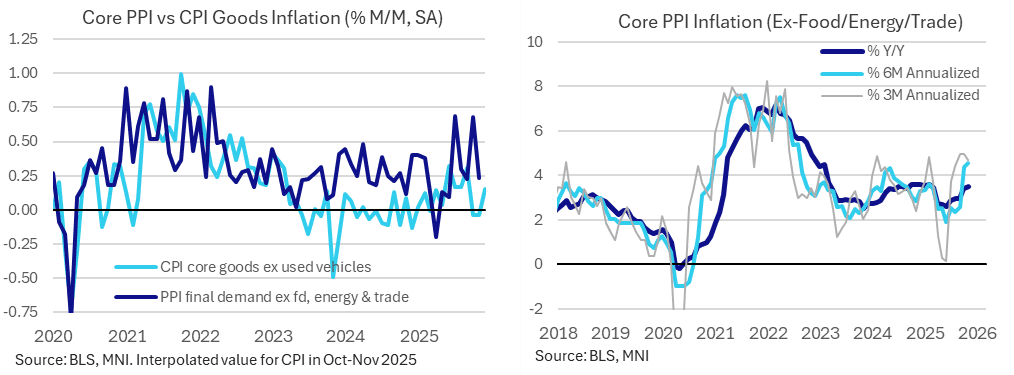

US DATA: Robust Core PPI Inflation In Two-Month Post-Shutdown Update

The two-month release for PPI inflation in Oct and Nov saw strong core inflation back in October before returning to more typical monthly rates in November. Recent run rates point to a further acceleration in the Y/Y ahead, with the six-month at its strongest since Aug 2022. The BLS notes a long lag in asking for specific pricing details, especially for the October values, which we guess could increase some volatility, but no material impact on response rates.

- PPI final demand increased 0.25% M/M (cons 0.2) in Nov after 0.12% M/M in Oct and a firmly upward revised 0.59% M/M in Sept (0.31 originally reported).

- As such, October beat expectations at 2.95% Y/Y (cons 2.7), although there is a large difference in the analyst sample with 44 estimates for the M/M vs 19 for the Y/Y.

- Core PPI (PPI ex food, energy & trade services) increased 0.23% M/M (cons 0.2) in Nov after a strong 0.68% M/M in Oct. September was also revised up slightly to 0.23% M/M (0.15% originally reported).

- It saw the core PPI Y/Y far stronger than expected in November at 3.50% Y/Y (cons 2.9) after 3.38% in Oct and 2.96% in the previously published data for September. Core PPI has previously peaked at 3.6% Y/Y in late 2024 and early 2025, and prior to that was last stronger in early 2023.

- Recent run rates are hotter at 4.7%/4.6% annualized on a three- and six-month basis. Tthe three-month rate has at least cooled from two months at 5.0% annualized but the six-month is at its strongest since Aug 2022.

- The volatile imputed trade services category explains some of the relative weakness here in the overall PPI category, at -0.8% M/M in both Nov and Oct.

- The recent strength in core PPI M/M inflation stands out against latest readings for CPI core goods – see charts below.

- BLS on the impact of the federal government shutdown on today's release: “The Federal government shutdown in October and November significantly delayed the transmission of Producer Price Index (PPI) price-update requests. October price-update requests, asking for information as of the October 14 pricing date, were sent to PPI survey respondents on November 19. Price-update requests for November data, asking for information as of the November 11 pricing date, were sent to PPI survey respondents on December 3. The response rates for the October and November data reflected in this release are within the normal range, and no modifications to PPI methodology or procedures were necessary.”

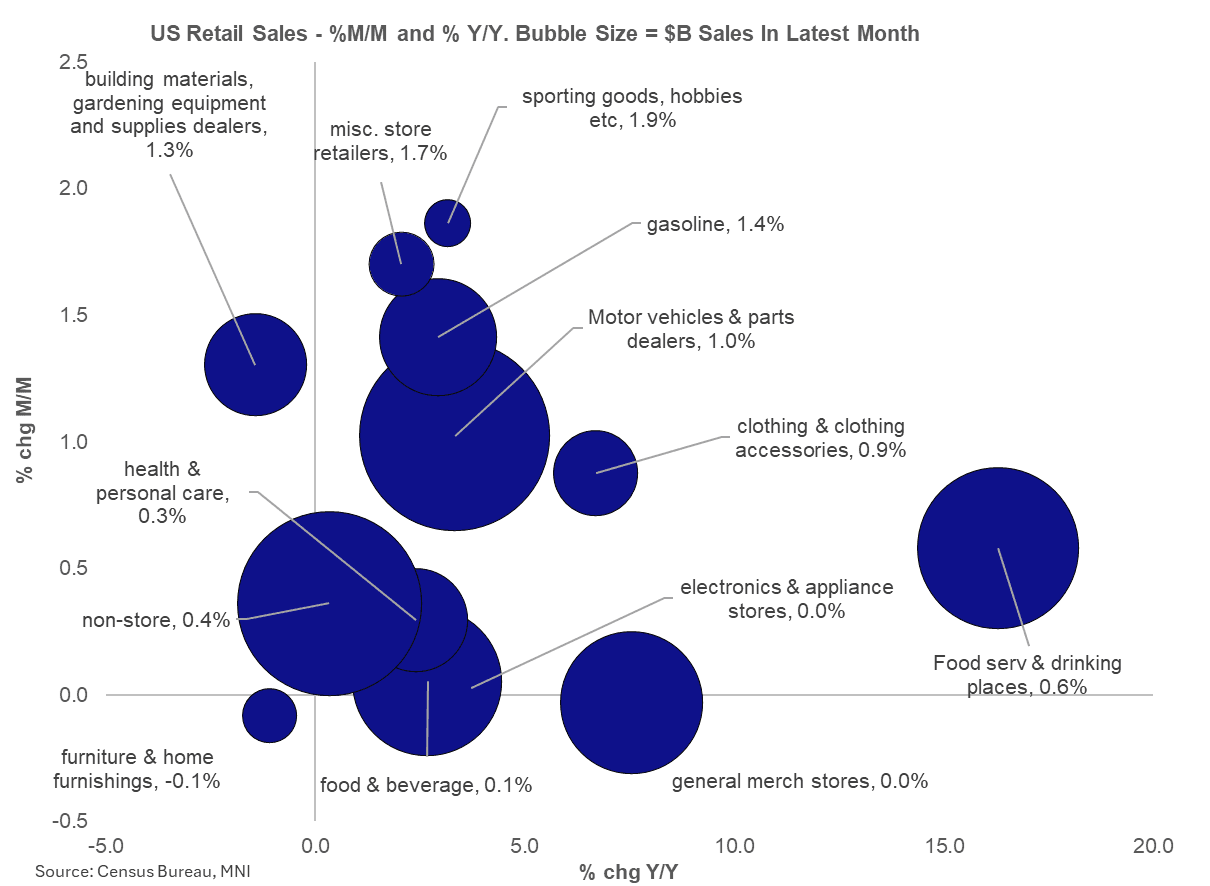

US DATA: Core Retail Sales Still Strong, But Slowdown Still Implied For Q4

November retail sales were solid on all counts, though October's very strong report was revised down to slightly less robust (but still quite strong) levels. Overall there is no sign of a retail consumption slowdown toward the end of 2025, though this report may marginally downgrade tracking estimates for Q4 private consumption (depending on one's assumptions for core sales in Nov).

- Headline sales beat expectations rising 0.6% (prior was rev down to -0.1% from 0.0%), but this was largely - as expected - due to strong motor vehicles/parts (+1.0% after -1.6%) and gasoline (+1.4% after -1.2%) sales, neither of which feed into the key GDP-input Control Group metric.

- The latter rose by 0.4% M/M, right in line with consensus but the October reading of 0.85% M/M was revised down fairly substantially to 0.61%. Ex-autos accelerated to 0.5% (0.2% prior; and above Chicago Fed CARTS' 0.3% expected) with ex-autos/gas steady at 0.4%.

- The major reason for the October downgrade to Control Group sales was non-store (ie online) retail which originally posted growth of 1.8% that has now been revised down to 1.0%. It then followed this up with 0.4% M/M in November.

- Indeed it was largely categories outside of the Control Group that had the most impressive gains: this included not just the aforementioned autos and gas, but also building materials (+1.3% after -1.3%), and key to services, food/drinking establishment sales rose to 0.6% after -0.1% (this was revised up from -0.4%).

- From a GDP tracking perspective, this report may result in a softer expectation for personal consumption in Q4 than previously expected, given that October's very strong Control Group figure was key to a strong base effect for the quarter.

- The Atlanta Fed's GDPNow metric estimates real PCE growth of 3.0% Q/Q SAAR in Q4 after 3.5% in Q3. It's unclear whether this report warrants a slight downgrade (it depends what they assumed for November) but either way a gradual slowdown estimate vs Q3 appears justified by recent tracking of retail Control Group growth.