MNI US Macro Weekly: Solid Week For The Dual Mandate

Feb-13 21:25By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- Overall, it was a solid week for the dual mandate variables. January’s nonfarm payrolls emboldened the FOMC hawks and all but eliminated the chances of a cut at the next meeting in March, but the more-moderate-than-expected January inflation data were probably enough to keep the Fed’s easing bias alive.

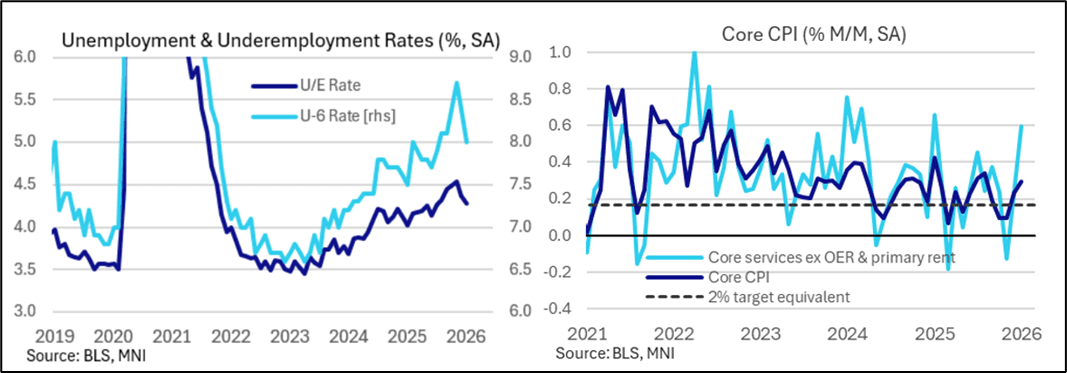

- The BLS Employment report for January was stronger than expected, rebutting various alternative indicators that either surprised lower or were outright soft in the past two weeks.

- And while the 130k payrolls gain and lowest unemployment rate since July came with some caveats, multiple analysts pushed back their expectations for the resumption of the Fed easing cycle beyond March.

- Having received some reassurance on the “full employment” side of the Fed’s dual mandate, January’s inflation report relieved some concerns on the “price stability” goal, with sequential headline and core CPI measures below-expected, though among other issues underlying the figures were a core goods pickup and an expansion of inflation breadth (and opinions vary on the ultimate PCE implications).

- December’s roundly weaker than expected retail sales data also carried a dovish tone, leading to a downward revision to Q4 personal consumption expenditures and raising new concerns about the momentum of consumption going into 2025.

- A patient approach is still expected, at least under Powell’s Fed. A next cut is still not fully priced for June and instead is seen in July, building to 62.5bp of cuts over 2026 vs 60.5bp pre-CPI and 59bp pre-NFP.

- In the upcoming holiday-shortened week, we get the minutes to the January Fed meeting which while stale after the latest data will be watched for the discussion on heightening the bar to further easing.

- The coming week’s data releases are backloaded, with the advance Q4 national accounts release and December personal income and outlays report both on Friday.

- Analysts currently eye a 2.8% annualized increase for real GDP growth in Q4 - some moderation in GDP growth is expected therefore after the 4.4% in Q3 and 3.8% in Q2, but of greater pertinence is domestic demand which is tracking at a softer 2.3% annualized according to GDPNow,

- December core PCE inflation is expected to be on the strong side, with analyst unrounded estimates on balance eyeing a slightly ‘low’ 0.4% M/M. In terms of inflation pressures when thinking about subsequent nominal numbers, they could have remained firm in January as well, with an admittedly unusually wide range of 0.19-0.49% M/M for core PCE inflation seen after the January CPI report.