FOREX: USDJPY Set to Post Near 3% Weekly Decline

Feb-13 17:52

- Friday’s session was an uneventful one for currencies, with the more stable risk backdrop having little impact across the G10 and the eagerly awaited US inflation data failing to spark any momentum for the major pairs. January brought softer-than-expected US CPI data across the board for the most part, though an upside beat in supercore. The Y/Y changes for headline and core CPI came in line/a little softer than expected.

- The dollar index tilts very marginally in the red Friday, allowing the DXY to have a fourth consecutive session of consolidating price action following the impressive 0.8% move south on Monday.

- Greenback weakness has been most notable against the Japanese yen following Japan’s election last Sunday. PM Takaichi’s convincing win has buoyed market hopes of both a more stable political backdrop and a more measured fiscal approach to policy. The stabilisation for JGB’s has fostered a substantial yen recovery, which has been exacerbated by positioning dynamics and thoughts that the BOJ’s March meeting could be live.

- After rallying at Monday’s open to 157.76, the aggressive selloff took us to within 17pips of the key 152.10 support and bear trigger. Despite an initial recovery Friday, spot has edged back to 152.80 ahead of the close, with the pair remaining to look vulnerable. The pre-October election close is at 147.47 and remains a significant downside target.

- AUDUSD has underperformed Friday to trade back below 0.7100, with this week’s rally falling just shy of the 2023 highs at 0.7158. Fresh cycle highs this week keep bullish conditions firmly intact, with dips remaining technically corrective at this juncture.

- Another notable mover this week has been the resilient Swiss Franc, with EURCHF printing below 0.9100 for the first time since the removal of the floor in 2015. Analyst notes have been surprisingly bullish CHF given the recent extremes and historical precedent for the SNB to comment on the strong levels of the franc, with one bank forecasting a move to 0.8700.

- Japan GDP and Eurozone industrial production data highlight a light calendar Monday, where volumes may be dampened due to China, the US and Canada out for national holidays.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Upside Plays Dominate Wednesday

Jan-14 17:52

Wednesday's Europe rates/bond options flow included:

- ERM6 97.93c, bought for 6 in 3.6k

- ERZ6 98.125/98.4375/98.50/98.8125 call condor, paper pays 4 in 10k

- ERZ6 98.12/98.4375/98.50/98.8125c condor vs 97.4375p, bought the condor for 1.75 in 10k. This was also bought Tuesday for 1.25 and 1.5 in 10k

- 0RG6 97.9375/97.875/97.8125 put fly, bought for 2 in 20k

- 0RH6 98.00/97.93/97.87/97.62p condor 2x1x3x2, bought for 3.75 in 8k x 4k x 12k x 8k

- SFIG6 96.40/96.35ps 1x2, bought for 1.25 in 5k

- SFIH6 96.45^, sold at 8.75 in 1.5k

- SFIM6 96.80/96.95 call spread, paper pays 1 for 11k all day

- SFIM6 96.65/96.85/97.05c fly, bought for 3.25 in 10k

- SFIM6 96.55/96.65/96.75c fly, bought for 1.5 in 4k

- SFIM6 96.80/96.95cs, bought for 1 in 5k2

US TSY OPTIONS: BLOCKs: 10Y Vol Sale, 30Y Calendar Spreads

Jan-14 17:44

- Block, +10,000 USH6 111/USJ6 109 put spds, 7 at 1234:14ET

- Block, +10,000 USH6 123/USJ6 121 call spds, 17 at 1234:07ET

- Blocks, -20,546 TYJ6 111/113.5 strangles, 46 from 1232-1233ET

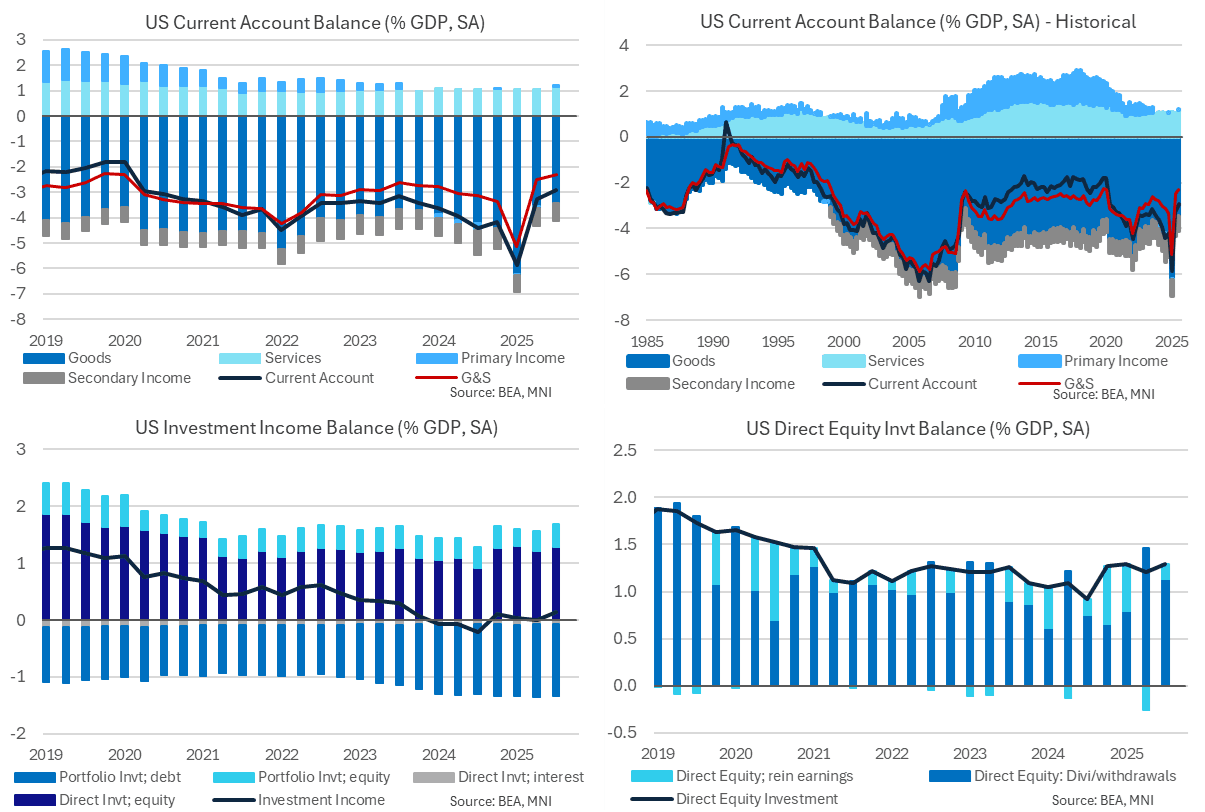

US DATA: Current Account Deficit Surprises Lower With Extra Boost From Incomes

Jan-14 17:43

Q3 current account data saw a smaller than expected deficit in Q3 at 2.9% GDP after 3.3% GDP in Q2, with the surprise coming from higher investment income. It's the smallest quarterly current account deficit since 2020 whilst the details confirmed a goods trade deficit at 3.4% GDP in Q3 for its smallest quarterly deficit since 2009 as President Trump noted ahead of the release. Add in services trade data also available for October and we’re tracking at the lowest broader trade surpluses since the late 1990s according to latest data.

- The current account deficit narrowed by more than expected in Q3 to $226.4bn (cons $238bn) from $249bn in Q2.

- The goods & services trade deficit narrowed from $189.8bn to $178.2bn as monthly data had already showed. The surprise instead came from primary income switching to its largest surplus in nominal terms since 3Q23, at $5.2bn vs a deficit of $5.8bn in Q2 (mainly on higher direct investment equity receipts but also from higher portfolio equity flows).

- It translates to a current account deficit of 2.9% GDP in Q3 (smallest since 1Q20) after 3.3% GDP in Q2, 5.9% GDP in Q1 and an average of 4.0% in 2024.

- The goods-only trade surplus saw a small narrowing on the quarter to 3.4% GDP (-0.1pp), which as Trump noted before the release was its smallest quarterly deficit since 2009.

- The broader goods & service trade surplus shows broadly similar trends, at 2.3% GDP for its joint smallest since 4Q19-1Q20 and 2Q09. It follows 2.5% GDP in Q2, 5.1% GDP in Q1 and an average 3.1% GDP in 2024.

- As part of Trump’s remarks on the deficit “going even lower”, we summarized after last week's October release, with its boost from higher gold exports and lower pharma imports, that this goods & services trade deficit has since shrunk to just 1.7% GDP on a three-month rolling basis for its smallest since the late 1990s.

- Elsewhere, the primary income surplus was worth 0.1% GDP in Q3 (+0.2pps) whilst the secondary income deficit held steady at 0.7% GDP for a third quarter.