BONDS: EGBs-GILTS CASH CLOSE: Rally Continues, Cementing Weekly Bull Flattening

Long-end European yields fell for a 4th consecutive session Friday, cementing a solid bull flattening move for the week.

- The key focus for the session was US inflation, and a softer-than-expected set of data triggered a rally in Treasuries that spilled over into Europe.

- Bunds underperformed Gilts overall however. German Defence Minister Klingbeil triggered a late sell-off when he did not rule out an exemption made to the debt brake rule for the country's raw material fund.

- Core EGBs gained on the day nonetheless; periphery/semi-core EGB spreads widened modestly.

- On the week, both the UK (2Y yield -3bp, 10Y -10bp) and German (2Y -5bp, 10Y -9bp) curves bull flattened.

- Ratings reviews for Austria (Moody's) and the Netherlands (also Moody's) feature after the cash close.

- UK macro takes centre stage next week, with the latest round of labour market, inflation, and retail sales data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 2.036%, 5-Yr is down 2.8bps at 2.337%, 10-Yr is down 2.4bps at 2.755%, and 30-Yr is down 1.7bps at 3.432%.

- UK: The 2-Yr yield is down 1bps at 3.593%, 5-Yr is down 3bps at 3.825%, 10-Yr is down 3.6bps at 4.416%, and 30-Yr is down 3.5bps at 5.223%.

- Italian BTP spread up 0.4bps at 60.9bps / French OAT up 1.2bps at 59.2bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGBs-GILTS CASH CLOSE: Gilt Rally Continues On Safe Haven Bid

European core FI benefited from a safe-haven big, with Gilts outperforming Bunds on the day.

- EGBs and Gilts saw early gains on geopolitical risk concerns (largely surrounding the ongoing Iranian situation).

- Equity markets led the tempo in the European afternoon, with financial stocks weaker after major bank earnings reports and tech struggling. This helped drive intraday downside in bond yields with curves closing bull flatter.

- Gilts benefited from a strong 10Y auction (and that tenor saw a fresh post-2024 low closing yield), while by comparison EGBs may have experienced relative headwinds given a German triple-line long-dated auction alongside French and Irish supply.

- Periphery/semi-core EGB spreads widened slightly; OATs were an underperformer - France's government survived no-confidences vote as expected, and now goes back to debating the state budget.

- BoE MPC member Taylor reaffirmed his well-known dovish stance; BOE's Ramsden appeared but did not comment on current monetary policy.

- UK monthly activity data is Thursday's scheduled highlight though we also get multiple Eurozone industrial production prints as well as the ECB's economic bulletin.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 2.075%, 5-Yr is down 3bps at 2.368%, 10-Yr is down 3.3bps at 2.814%, and 30-Yr is down 3.1bps at 3.422%.

- UK: The 2-Yr yield is down 3.3bps at 3.625%, 5-Yr is down 5.3bps at 3.804%, 10-Yr is down 5.8bps at 4.34%, and 30-Yr is down 4.7bps at 5.092%.

- Italian BTP spread up 0.4bps at 63.6bps / French OAT up 0.8bps at 68bps

EURUSD TECHS: Bear Threat Still Present

- RES 4: 1.1919 High Sep 17 and a key M/T resistance

- RES 3: 1.1848 High Sep 18

- RES 2: 1.1808 High Dec 24 and the bull trigger

- RES 1: 1.1696/1765 20-day EMA / High Jan 2

- PRICE: 1.1658 @ 15:54 GMT Jan 14

- SUP 1: 1.1618 Low Jan 9

- SUP 2: 1.1598 61.8% retracement of the Nov 5 - Dec 12 bull leg

- SUP 3: 1.1549 76.4% retracement of the Nov 5 - Dec 12 bull leg

- SUP 4: 1.1512 Low Nov 25

EURUSD continues to trade closer to its recent lows. A short-term bearish theme remains intact. Last week’s move down resulted in a breach of support at 1.1659, the Jan 5 low. The sell-off suggests a bear cycle appears likely to dominate near-term and sights are on 1.1598, a Fibonacci retracement. Initial resistance is at 1.1696, the 20-day EMA. A clear break of the average would highlight a possible reversal signal.

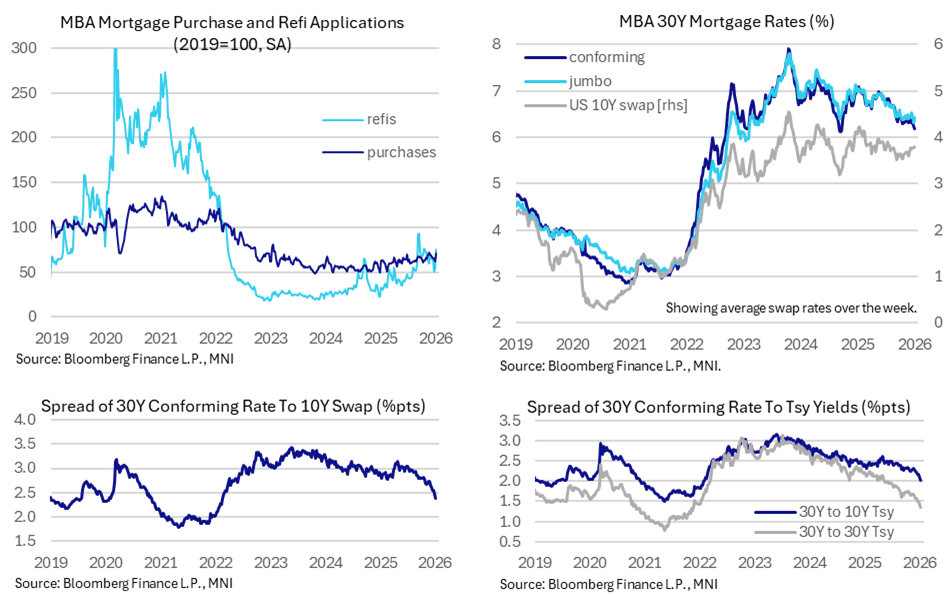

US DATA: Another Week, Another Narrowing In Mortgage Lending Spreads

- MBA composite mortgage applications jumped 28.5% (sa) last week in the first full week of the year, still in a period where the series can see heightened volatility.

- It came as refis surged 40% after 7% and -20%, whilst new purchase applications increased 16% after -6% and 0%.

- We’ll need to see further weeks of data but for now, levels relative to 2019 average: 72.5% composite, 71% new purchases and 76% refis.

- Increases are supported by what’s been a sizeable decline in mortgage rates in recent weeks, with the 30Y conforming rate of 6.18% down 7bps on the week and 20bps since mid-Dec.

- An impressive narrowing trend in spreads continued last week, with the 30Y rate spread to the average 10Y swap rate over the week falling another 8bps to 239bp. It peaked at 315bp in May in post-tariff disruption and averaged 285bp in 1Q25 or 302bp in 2024.

- Compared to August when US Tsy Sec Bessent talked on wanting to see flat or lower mortgage spreads, this swap rate spread has narrowed 55bp or 39bps to 202bps for the 10Y Treasury yield equivalent.

- Narrowing has been supported by Fannie Mae and Freddie Mac increasing their retained portfolios ahead of a potential IPO, with MBS spreads then tumbling last week after Trump ordered $200bn in MBS purchases.