US: DHS Set To Shut Down At Midnight, No Clear Offramp To ICE Standoff

The Trump administration announced yesterday that it is ending its deployment of federal immigration agents in Minnesota. The move was welcomed by Democratic leaders in the state, but it does not appear to be enough to prevent a shutdown of the Department of Homeland Security at midnight tonight.

- Yesterday, Senate Democrats blocked a House-passed funding bill for the department, saying negotiations had not delivered sufficient reforms to immigration enforcement. Lawmakers departed for a weeklong recess shortly after the vote.

- The Wall Street Journal notes, “DHS oversees Immigration and Customs Enforcement and Customs and Border Protection as well as the [FEMA], the [TSA] and the US Coast Guard. While the failed vote sets the stage for funding to lapse at DHS for at least a week, there isn’t expected to be any significant impact on border enforcement from the shutdown.” The Journal outlines DHS shutdown impacts here.

- As the political imperative to end the shutdown is limited, the lapse of appropriations is likely to extend for weeks. Democrats are expected to send a counteroffer to the White House this weekend outlining their demands, including a raft of guardrails on the operations of federal immigration agents.

- Politico notes, “despite the rhetoric, both sides are largely keeping the details private — a sign that officials are taking the talks seriously,” with a senior administration official telling reporters Thursday, “We’re sort of just waiting for the next phase from the Democrats.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Fed Pricing Looks Through PPI & Retail Sales, 53bp Cuts Priced Through Dec

Muted reaction to the PPI and retail sales data, with the USD short end effectively unchanged vs. pre-release levels. Retail sales was on the firmer side of expectations at the margin (albeit with negative revisions to the prior month evident), while PPI data was in line to firmer (lack of market reaction noted despite forward looking upside risks outlined in our recent PPI bullet).

- FOMC-dated OIS showing just under 1bp of easing for this month, 6.5bp through March, 11bp through April, 24bp through June, 32bp through July and 53bp through year-end.

- Meanwhile, SOFR futures are flat to 1.5bp higher on the day vs. flat to +1.0 heading in. SOFR-implied terminal rate pricing at 3.16% vs. Monday’s close of 3.19%, which represented the most hawkish closing level seen since the Dec FOMC.

ENERGY SECURITY: US Withdrawing Personnel from Mideast Bases: Reuters

The US is withdrawing some personnel from key bases in the Middle East as a precaution given heightened regional tensions, a U.S. official told Reuters.

- The disclosure follows remarks by a senior Iranian official who told Reuters earlier on Wednesday that Tehran had warned neighbours hosting U.S. troops that it would hit American bases if Washington strikes.

- This, coupled with Trump’s comments yesterday that citizens of the US and its allies should get out of Iran and the comment that help is on its way to protesters, raise further speculation that the U.S may be planning a strike on the Islamic Republic.

- While crude prices are already carrying a geopolitical risk premium, that is set to jump if the U.S or Israel strikes Iran.

- In contrast to the symbolic response from Iran after U.S strikes on its nuclear facilities, the regime in Tehran is likely to be more aggressive in targeting US military infrastructure in the Gulf.

- These, located in oil producers such as Iraq, Kuwait, Saudi Arabia, Bahrain, Qatar, the UAE, and Oman, raise the risk that oil and gas infrastructure could be caught in the crossfire.

- It also raises the stakes for a worst-case scenario where Iran tries to block the Straits of Hormuz, a chokepoint for 20% of global oil flows. Should this happen, it would prompt a stronger response from the US fifth fleet located in Bahrain.

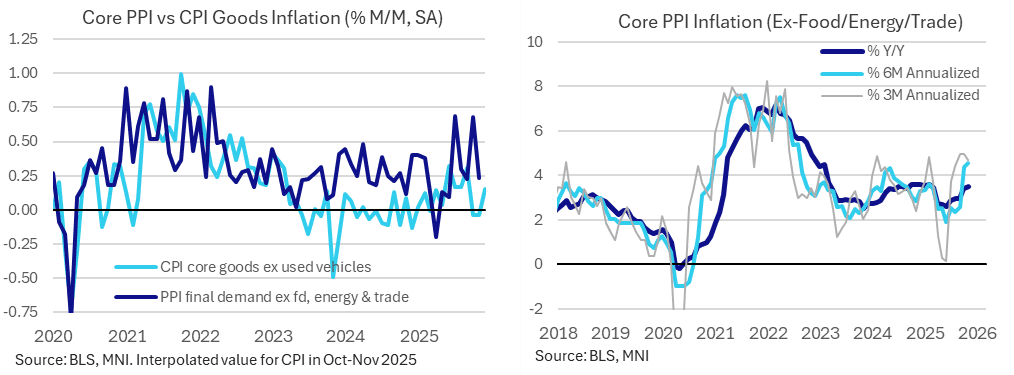

US DATA: Robust Core PPI Inflation In Two-Month Post-Shutdown Update

The two-month release for PPI inflation in Oct and Nov saw strong core inflation back in October before returning to more typical monthly rates in November. Recent run rates point to a further acceleration in the Y/Y ahead, with the six-month at its strongest since Aug 2022. The BLS notes a long lag in asking for specific pricing details, especially for the October values, which we guess could increase some volatility, but no material impact on response rates.

- PPI final demand increased 0.25% M/M (cons 0.2) in Nov after 0.12% M/M in Oct and a firmly upward revised 0.59% M/M in Sept (0.31 originally reported).

- As such, October beat expectations at 2.95% Y/Y (cons 2.7), although there is a large difference in the analyst sample with 44 estimates for the M/M vs 19 for the Y/Y.

- Core PPI (PPI ex food, energy & trade services) increased 0.23% M/M (cons 0.2) in Nov after a strong 0.68% M/M in Oct. September was also revised up slightly to 0.23% M/M (0.15% originally reported).

- It saw the core PPI Y/Y far stronger than expected in November at 3.50% Y/Y (cons 2.9) after 3.38% in Oct and 2.96% in the previously published data for September. Core PPI has previously peaked at 3.6% Y/Y in late 2024 and early 2025, and prior to that was last stronger in early 2023.

- Recent run rates are hotter at 4.7%/4.6% annualized on a three- and six-month basis. Tthe three-month rate has at least cooled from two months at 5.0% annualized but the six-month is at its strongest since Aug 2022.

- The volatile imputed trade services category explains some of the relative weakness here in the overall PPI category, at -0.8% M/M in both Nov and Oct.

- The recent strength in core PPI M/M inflation stands out against latest readings for CPI core goods – see charts below.

- BLS on the impact of the federal government shutdown on today's release: “The Federal government shutdown in October and November significantly delayed the transmission of Producer Price Index (PPI) price-update requests. October price-update requests, asking for information as of the October 14 pricing date, were sent to PPI survey respondents on November 19. Price-update requests for November data, asking for information as of the November 11 pricing date, were sent to PPI survey respondents on December 3. The response rates for the October and November data reflected in this release are within the normal range, and no modifications to PPI methodology or procedures were necessary.”