MNI ASIA OPEN: Data Interrupted - The Sequel

EXECUTIVE SUMMARY

- MNI US DATA: October CPI May Not Ever Be Released; Payrolls May Be Partial

- MNI INTERVIEW: Fed's Risk Management Cuts Not Enough - Revelio

- MNI US-CHINA: MOFCOM Touts 'Stable Supply Chains' After US Affiliate Rule Suspension

- MNI US DATA: Post-Shutdown Data Schedules Should Be Out By Early Next Week

- MNI US DATA: Redbook Retail Sales Maintain Solid Pace In Early November

- MNI US DATA: Weekly ADP Series Rolls Over

US

MNI US DATA: Post-Shutdown Data Schedules Should Be Out By Early Next Week

From our FAQs on the post-shutdown data deluge (PDF here)

What data has been postponed, and will postponements continue to be made after the shutdown?

- We assume that federal agencies will fully re-open on Thursday November 14.

- The only real historical analogue to the current situation is the 2013 shutdown which lasted from Oct 1 through Oct 16. That was only a little over 2 weeks compared with the roughly 6 weeks in the current shutdown, and even so it caused multiple data release postponements and even cancellations that reverberated through December.

When will updated data release schedules be available?

- In October 2013’s shutdown, then-President Obama signed the re-opening bill late Wednesday Oct 16. Federal employees went "back to work" Thursday Oct 17 and on that day, the Bureau of Labor Statistics released a schedule for postponed and upcoming data releases: we publish the major postponements published by the BLS in an appendix below.

- Almost every data point was postponed, even those due out in November, as the BLS attempted to work through the backlog and collect underlying data. The BLS's first post-shutdown release was Oct 21, which was the following Monday. September Nonfarm Payrolls, which were due out Oct 4, were released Oct 22.

MNI US DATA: October CPI May Not Ever Be Released; Payrolls May Be Partial

When will the monthly inflation and employment reports be released?

- Our thinking on this topic is partly based on the 2013 experience, but also largely on interviews our Policy Team conducted with two ex-BLS commissioners available here and here.

- CPI: Starting with CPI: the BLS already released September data (albeit delayed), but as of this week will have postponed the October release. It looks unlikely that the BLS will be able to release October CPI at all: most of the survey and otherwise data required was not collected in the month.

- For November’s report, it’s a close call whether the data can be released. For example, it is questionable whether BLS field agents can collect 4 weeks of data in half that time. It will be a judgment call on the part of the BLS whether to publish their best estimate of November CPI. If they do, it is possible they linearly divide the price index growth over 2 months, to fill in a number for Oct CPI and Nov CPI. This would be unprecedented so we’re not sure what the data set would look like.

- Overall, CPI data look like they will be less robust than usual until at least the December report out in Jan.

- Nonfarm Payrolls: In better news, the BLS is probably in a position to start releasing data as soon as Friday, namely the September nonfarm payrolls report which by all accounts was already in hand as the shutdown began. Indeed we wouldn’t be surprised by a Friday morning release though this could slip into early next week (per the 2013 template).

- For the October data, we could see a partial release. The establishment data are collected electronically, so the payrolls figures will be published. However, the household survey – which is used to produce variables including the unemployment and participation rates - was never fielded, and may never be.

- For November, again looking at the 2013 example, the BLS was able to publish October payrolls on Nov 8, exactly a week after its originally scheduled date. The 2025 shutdown may have concluded just in time to allow for a similarly limited delay this time (so a Dec 5 scheduled release may be pushed back to Dec 12).

NEWS

MNI INTERVIEW: Fed's Risk Management Cuts Not Enough - Revelio

The U.S. labor market will continue to soften and the Federal Reserve's 50 basis points of interest rate easing so far this year will not be enough to shore up hiring, private data provider Revelio Labs’ chief economist Lisa Simon told MNI. "It just feels like what's happening is we're sliding off a muddy hill," she said about the labor market. "I think we'll sort of see a slow sliding downwards into negative territory when it comes to job gains."

MNI US-CHINA: MOFCOM Touts 'Stable Supply Chains' After US Affiliate Rule Suspension

(MNI) London - China's Ministry of Commerce has released comments from a departmental spox talking up ties with the US. Asked by a reporter on the MOFCOM's reaction to the US suspending for a year its export control affiliates rule, the spox says, "China is willing to work with the United States, upholding the principles of mutual respect and equal consultation, to strengthen dialogue and exchanges, properly manage differences, and jointly create favorable conditions for promoting mutually beneficial cooperation between enterprises of the two countries and ensuring the security and stability of global industrial and supply chains."

MNI SECURITY: CNN-UK Suspends Some Intel Sharing w/US Concerning LatAm Boat Strikes

CNN reports that the UK has suspended its sharing of intelligence with the US in the Caribbean and eastern Pacific amid concerns about the legality of recent US strikes on vessels in the region that the US claims are involved in drug trafficking.

US TSYS

MNI US TSYS: Veterans Day Sideways Shuffle

- Treasuries hold firmer - narrow range since marking session high late morning. Currently, the Dec'25 10Y contract trades +10.5 at 113-00.5 vs. 113-01.5 high - just below resistance at 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal.

- Otherwise, a short-term bear theme in Treasuries remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02. The trendline is drawn from the May 22 low.

- USD also holding narrow range since marking session low in the first half, Bbg $ index BBDXY -1.38 at 1,217.33 vs. 1,216.52 low.

- The DJIA, however, continues to climb: +5011.60 at 47,880.23 (+1.09%), outpacing SPX eminis (+0.28%) while the Nasdaq holds mildly weaker (-0.1%).

- Look ahead: Wednesday data limited to MBA Mortgage Applications at 0700ET, Tsy auctions: $69B 17w bill and 42B 10Y Note (91282CPJ4). Focus on multiple Fed speakers through the session: Williams, Paulson, Waller, Bostic, Miran and Collins.

OVERNIGHT DATA

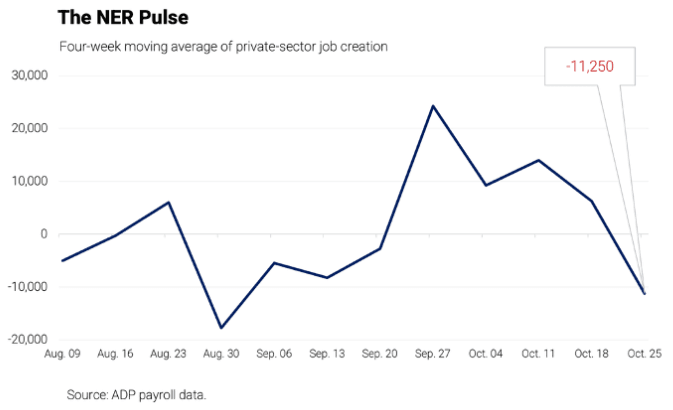

MNI US DATA: Weekly ADP Series Rolls Over

The first known-ahead-of-time release of the weekly ADP data was marred by data dissemination issues but ultimately suggested a return of private sector job losses in data up to Oct 25. On its own it points to renewed sizeable deterioration in net job creation after some stabilization in the monthly October report (with its reference week including the 12th of the month), although ADP warns that these data are preliminary and can be revised.

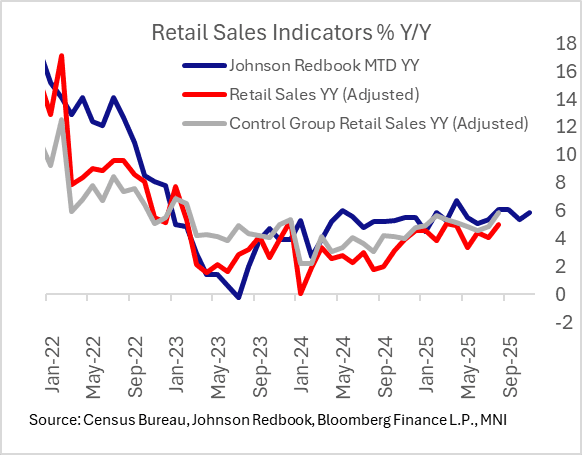

MNI US DATA: Redbook Retail Sales Maintain Solid Pace In Early November

Retail sales rose 5.9% Y/Y in the first week of November (to Nov 8), per the latest Johnson Redbook Retail Sales Index release. It's still early in the month but that's a slight uptick from 5.4% in October.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 587.89 points (1.24%) at 47958.52

S&P E-Mini Future up 19.75 points (0.29%) at 6877.5

Nasdaq down 37.5 points (-0.2%) at 23491.44

US 10-Yr yield is unchanged 0 bps at 4.116%

US Dec 10-Yr futures are up 11/32 at 113-1

EURUSD up 0.0032 (0.28%) at 1.1588

USDJPY down 0.06 (-0.04%) at 154.1

WTI Crude Oil (front-month) up $0.87 (1.45%) at $61.00

Gold is up $12.19 (0.3%) at $4127.99

European bourses closing levels:

EuroStoxx 50 up 61.24 points (1.08%) at 5725.7

FTSE 100 up 112.45 points (1.15%) at 9899.6

German DAX up 128.07 points (0.53%) at 24088.06

French CAC 40 up 100.72 points (1.25%) at 8156.23

US TREASURY FUTURES CLOSE

3M10Y +2.554, 26.422 (L: 23.868 / H: 26.422)

2Y10Y +0, 52.315 (L: 52.315 / H: 52.315)

2Y30Y +0, 111.256 (L: 111.256 / H: 111.256)

5Y30Y +0, 99.032 (L: 99.032 / H: 99.032)

Current futures levels:

Dec 2-Yr futures up 2.375/32 at 104-7 (L: 104-04.25 / H: 104-07.125)

Dec 5-Yr futures up 7.5/32 at 109-15 (L: 109-06.25 / H: 109-15)

Dec 10-Yr futures up 11/32 at 113-1 (L: 112-20 / H: 113-01.5)

Dec 30-Yr futures up 16/32 at 117-16 (L: 116-24 / H: 117-19)

Dec Ultra futures up 17/32 at 121-8 (L: 120-13 / H: 121-13)

MNI US 10YR FUTURE TECHS: (Z5) Bear Threat Remains Present

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-02 High Nov 5& 7 and a key near-term resistance

- PRICE: 113-00 @ 11:10 GMT Nov 11

- SUP 1: 112-09+ Low Nov 5

- SUP 2: 112-08+ 38.2% retracement of May - Oct Upleg

- SUP 3: 112-08/06 100-dma / Low Sep 25 and a reversal trigger

- SUP 4: 112-02 Trendline support drawn from the May 22 low

A short-term bear theme in Treasuries remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02. The trendline is drawn from the May 22 low. Resistance to watch is 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.025 at 96.250

Mar 26 +0.040 at 96.465

Jun 26 +0.050 at 96.70

Sep 26 +0.055 at 96.855

Red Pack (Dec 26-Sep 27) +0.050 to +0.055

Green Pack (Dec 27-Sep 28) +0.050 to +0.055

Blue Pack (Dec 28-Sep 29) +0.050 to +0.050

Gold Pack (Dec 29-Sep 30) +0.045 to +0.050

MNI PIPELINE: Corporate Bond Roundup - Issuers Sidelined on Veterans Day

- Date $MM Issuer (Priced *, Launch #)

- 11/11 No new corporate supply Tuesday - issuers sidelined on Veterans Day holiday

- $19.95B Priced Monday

- 11/10 $11B *Verizon: $2B +7Y +90, $2.25B +10Y +100, $1.5B 20Y +110, $3.25B 30Y +120, $2B 40Y +130

- 11/10 $1.65B *Enterprise Products Op $300M 3Y Tap +43, $600M 5Y Tap+73, $750M 10Y tap +93

- 11/10 $1.6B *Caterpillar $1.05B 3Y +37, $550M 3Y SOFR+58

- 11/10 $1.5B *LyondellBasell $500M 5Y +145, $1B 10Y +185

- 11/10 $900M *Mosaic $500M +3Y +77, $400M 5Y +92

- 11/10 $750M *Flex $150M 7Y +105, $600M 10Y +130

- 11/10 $750M *Plains All American $300M 5Y +102, $450M 10Y +142

- 11/10 $700M *Carpenter Tech 8.25NC3.25 5.625%

- 11/10 $600M *AutoNation +3Y +90

- 11/10 $500M *Illumina WNG 5Y +105

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Easily Outperform On Soft Labour Data

Gilts easily outperformed peers Tuesday.

- UK labour market data broadly came in on the soft side, driving an early bull steepening rally. A December BOE cut is now around 80% priced from <70% prior, helping the UK short-end strengthen (2Y yields hit a post-Aug 2024 low).

- Treasuries led a global rally in early afternoon on weekly ADP private sector payrolls data that showed a notable contraction in the 4-week period to Oct 25.

- In other data, German ZEW underperformed in both expectations and current conditions.

- BOE MPC hawk Greene reiterated her previously aired areas of focus, having no impact on the short end & gilts.

- On the day, the German curve lightly bull flattened, while the UK's held its early bull steepening.

- Periphery/semi-core EGB spreads were little changed vs Bunds.

- Wednesday's calendar includes Italian industrial production and final German CPI. We also get commentary from ECB's Schnabel and de Guindos, as well as BOE's Pill.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.4bps at 2.001%, 5-Yr is down 0.9bps at 2.259%, 10-Yr is down 1bps at 2.658%, and 30-Yr is down 0.6bps at 3.254%.

- UK: The 2-Yr yield is down 8.3bps at 3.724%, 5-Yr is down 7.8bps at 3.857%, 10-Yr is down 7.4bps at 4.387%, and 30-Yr is down 6.7bps at 5.172%.

- Italian BTP spread up 0.1bps at 74.5bps / French OAT down 0.4bps at 76.4bps

MNI FOREX: USD Index Extends Recent Weakness Following Data, CHF Outperforms

- A softer-than-expected ADP jobs release from the US caught the market a little off guard on Tuesday, weighing on the greenback and allowing the USD index to plumb new pullback lows below 99.40.

- ADP noted that “not only is the pace of employment growth shifting lower, it’s doing so in a jagged path across occupations, industries, and geographies. Going forward, instead of being a stable constant, the break-even rate more likely will be constantly moving”.

- Most notable initially was the move for USDJPY, which extended its selloff from the overnight highs to around 80 pips. Downside momentum picked up on a break of the overnight lows, below 154.00 to 153.67 lows before stabilising. We have pointed out that USDJPY continues encounter some resistance above the 154.00 handle, potentially registering an eighth daily high between 154.14-154.49, bolstering the short-term significance of this resistance cluster. First important support to watch lies at 152.70, the 20-day EMA.

- CHF outperforms following late yesterday's optimism on a potential Swiss trade deal with the US. While such a deal would be unlikely to sway SNB rates this year or the next, it should see a moderate upwards revision of 2026 GDP forecasts for the country, which is providing a boost to the Franc. EURCHF sees downside pressure as a function of that at 0.9273, while USDCHF (-0.67%) has tracked back below 0.8000.

- EURUSD broke above Friday’s high to trade back above 1.1600. The 50-day EMA intersects at 1.1627, and a breach would alter the short-term bearish theme.

- It’s worth noting that GBPUSD fully reversed the UK labour market data inspired selloff, however, sterling weakness remains evident through the cross, with EURGBP maintaining its position back above 0.88 for now.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0900/1000 | * | Industrial Production | |

| 12/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 12/11/2025 | 1045/1145 | ECB Schnabel Speech at BNP Paribas | ||

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | *** | Money Supply | |

| 12/11/2025 | - | *** | New Loans | |

| 12/11/2025 | - | *** | Social Financing | |

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits | |

| 12/11/2025 | 1420/0920 | New York Fed's John Williams | ||

| 12/11/2025 | 1500/1000 | Philly Fed's Anna Paulson | ||

| 12/11/2025 | 1505/1005 | Kansas City Fed's Jeff Schmid | ||

| 12/11/2025 | 1520/1020 | Fed Governor Chris Waller | ||

| 12/11/2025 | 1730/1230 | Fed Governor Stephen Miran | ||

| 12/11/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 12/11/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 12/11/2025 | 2050/1550 | New York Fed's Roberto Perli | ||

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins | ||

| 13/11/2025 | 0030/1130 | *** | Labor Force Survey |