MNI ASIA OPEN: Canada Trolls Pres Trump on Tariffs

EXECUTIVE SUMMARY

- MNI CANADA: PM Carney-Can Pick Up On Trade Talks When US Is Ready

- MNI CANADA: Ontario's Ford Says US Ad Campaign That Upset Trump Will Soon Be Paused

- MNI EU-RUSSIA: Belgian Objections Punt Frozen Russian Asset Loan Plan To Dec EUCO

- MNI US DATA: U.Mich 1Y Inflation Expectations Hold Dip But 5-10Y Highest Since June

- MNI US DATA: Core CPI Trends: Shorter-Term Run Rates Somewhat Higher Than Y/Y

US

MNI FED: MNI Fed Preview - October 2025: QT, Or Not QT

MNI's preview of the October FOMC has been published - Download Full Report Here

- The Federal Reserve is overwhelmingly expected to cut the funds rate by 25bp for a 2nd consecutive meeting on October 29, bringing the target range to 3.75-4.00%.

- This will again be framed as a risk management cut, with the limited data available since the September meeting not disconfirming that the shift in the balance of risks had tilted toward labor market downside.

- Dissent to this decision should once again be limited to Gov Miran in favor of a 50bp cut.

- With limited new developments and official data to opine on, Chair Powell’s press conference will be eyed for affirmation that a December cut remains on track, as signalled by the most recent Dot Plot.

- He’s unlikely to give much away, but it would be surprise given the lack of data and relevant developments if he suggested that a further 2025 cut was in any greater doubt than it was 6 weeks earlier.

- Instead, we think focus in terms of action at this meeting will be on the balance sheet, with the Fed likely to announce an end to quantitative tightening amid diminishing reserve levels and nascent evidence of funding market pressures.

- We will also be watching for any news on the Fed’s communications framework, with an updated “Dot Plot” potentially unveiled at some point by year-end.

NEWS

MNI BRIEF: Interest Rate Cut Needed To Boost Domestic Demand

China needs to continue lowering interest rates and increase fiscal spending to rapidly address weak demand and secure nominal GDP growth above 5% in 2025, China Finance 40 Forum senior researcher Zhang Bin said Saturday at the Bund Summit in Shanghai. Zhang, who is also deputy director of the Institute of World Economics and Politics at the Chinese Academy of Social Sciences, noted that given current low price levels and weak corporate profits, real interest rates remain elevated. Sustained reductions in real borrowing costs would help rebalance savings and investment, he said.

MNI BRIEF: Policy To Be Supportive, Consumption Key To Growth

Consumption will be crucial in absorbing China’s excess capacity as external markets become less open, while policies are likely to remain supportive but not overly expansionary given rising central government leverage and ongoing efforts to repair the balance sheets of households, companies, financial institutions and local governments, People’s Bank of China monetary policy committee member Huang Yiping said Saturday at the Bund Summit in Shanghai.

MNI CANADA: Ontario's Ford Says US Ad Campaign That Upset Trump Will Soon Be Paused

Ontario Premier Ford says on x.com re the ads that spurred President Trump to end trade talks with Canada: "In speaking with Prime Minister Carney, Ontario will pause its U.S. advertising campaign effective Monday so that trade talks can resume." Limited reaction in USDCAD and rates to this apparent de-escalation.

- Full post: @fordnation "Our intention was always to initiate a conversation about the kind of economy that Americans want to build and the impact of tariffs on workers and businesses. We've achieved our goal, having reached U.S. audiences at the highest levels. I've directed my team to keep putting our message in front of Americans over the weekend so that we can air our commercial during the first two World Series games.

MNI CANADA: PM Carney-Can Pick Up On Trade Talks When US Is Ready

(MNI) London - Reuters reports first public comments from PM Mark Carney following US President Donald Trump's announcement that trade talks with Canada would be "terminated immediately". Carney says, "We can't control the trade policy of the US...We recognise US policy has changed...Canadian officials have been working on negotiations on trade, lots of progress [has been] made" Says Canada, "stands ready to pick up on that progress and build on that progress when the Americans are ready to have those discussions."

MNI US: Summary Of NEC Director Hassett's Comments To Reporters

Summary of National Economic Council Director Kevin Hassett’s recent comments to reporters at the White House. On the government shutdown: “We 100% want the government open. We agree with Speaker Johnson… Democrats in the Senate are no longer a moderating force…” Hassett gives no indication that the White House is considering breaking with the Congressional GOP position on negotiating with Democrats on healthcare, signalling that the impasse will continue.

MNI EU-RUSSIA: Belgian Objections Punt Frozen Russian Asset Loan Plan To Dec EUCO

Kyiv's hopes that the EU could agree on 23 Oct to a plan that would see frozen Russian assets held in the Union to fund 'reconstruction loans' for Ukraine have been dashed, at least in the short term. The key hold-out on the plans to utilise EUR140bln in frozen assets held at Euroclear has been Belgium, whose PM, Bart De Wever, argued that his gov't would be at legal risk if the funds were seized.

MNI US-RUSSIA: Putin Envoy-Want Dialogue w/US Despite 'Unfriendly Steps'

Reuters reporting comments from Kirill Dmitriev, CEO of the Russian Direct Investment Fund and President Vladimir Putin's special envoy on Foreign Investment and Economic Cooperation, who is in the US for talks amid a major escalation in tensions after the Trump administration imposed sanctions on oil giants Lukoil and Rosneft. Dmitriev confirms he is in the US for a trip planned some time ago.

US TSYS

MNI US TSYS: Tsys Reject Post-CPI Rally, Mildly Lower, Focus on Next Week's FOMC

- Treasuries look to finish mildly weaker Friday - well off knee-jerk highs after the Sep CPI inflation data came out lower than expected. Core rose a seasonally adjusted 0.23% M/M (median unrounded expectation of 0.32) and with the miss translating into the non-seasonally adjusted Y/Y rate at 3.02% (cons 3.1) after two months at 3.1%.

- White House's Rapid Response account on X.com suggests that the BLS may not release an October inflation report because it was unable to conduct the in-person surveys as normal during October, on account of the shutdown.

- Tsys extended lower after S&P flash PMI (link) noted strong business activity growth (second-fastest of the year) although prices charged rose at their softest rate since April. Tsys held modestly weaker levels after lower than expected UofM sentiment, current conditions and expectations, while 5-10Y inflation exp rises slightly.

- Tsy Dec'25 10Y contract currently at 113-14.5 (-1) vs. 113-09.5 low, 10Y yld 3.9969% -.0040; curves mildly steeper: 2s10s +0.667 at 51.270, 5s30s +1.634 at 98.433. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 113-06+, the 20-day EMA.

- The dollar index declined around 30 pips in the immediate aftermath, however, downside momentum quickly stalled. Overall, the DXY is unchanged on the session.

- Stocks gapped to new record highs following Friday morning's lower than expected CPI inflation data, sentiment buoyed as the report underscored expectations of two 25bp rate cuts by year end.

OVERNIGHT DATA

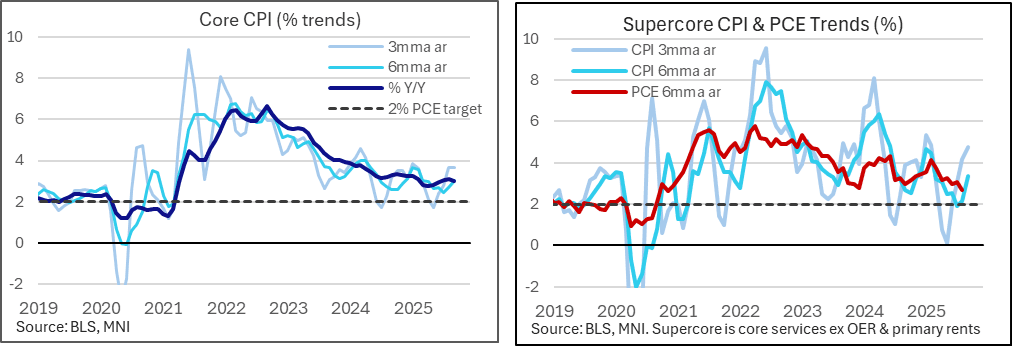

MNI US DATA: Core CPI Trends: Shorter-Term Run Rates Somewhat Higher Than Y/Y

- Core CPI was clearly softer than expected in September, rising a seasonally adjusted 0.23% M/M (median unrounded expectation of 0.32) and with the miss translating into the non-seasonally adjusted Y/Y rate at 3.02% (cons 3.1) after two months at 3.1%. The Y/Y has been within a 2.8-3.3% range since mid-2024.

- The three-month run rate held above this Y/Y at 3.6% annualized (unchanged) whilst the six-month met it as it lifted to 3.0% after 2.7% in August.

- Supercore CPI inflation meanwhile was closer to expectations in September at a solid 0.35% M/M (analyst range 0.30-0.42) which saw three- and six-month rates accelerate to 4.7% and 3.3% respectively. This category is however the most prone to deviations from its PCE counterpart - see the below chart.

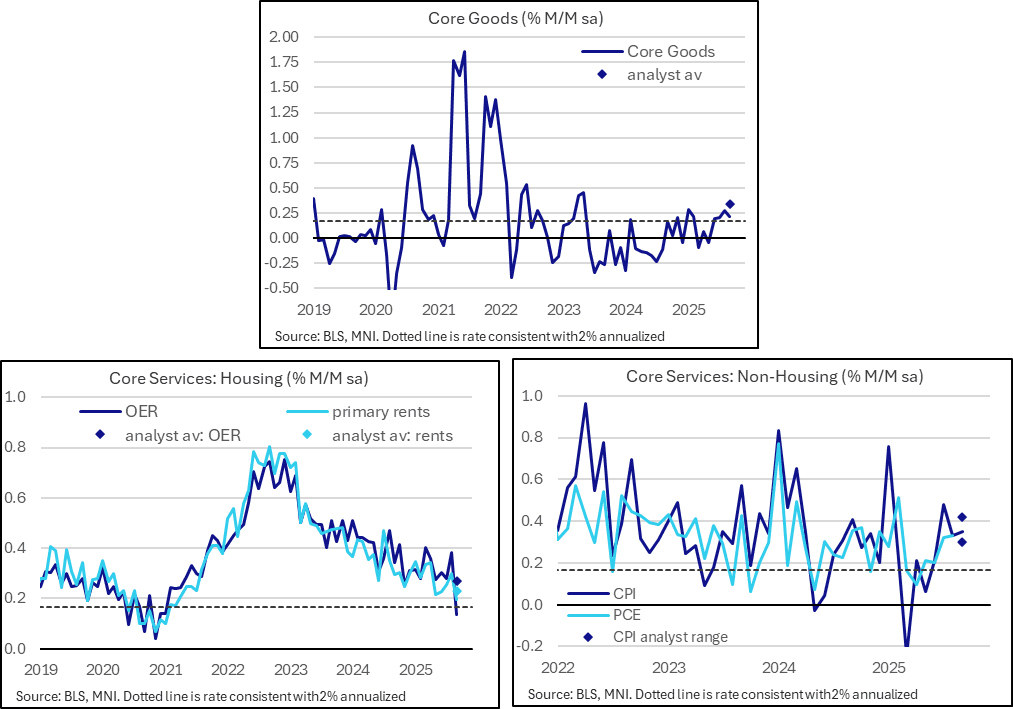

MNI US DATA: Core Goods And Housing CPI Miss, Supercore Within Estimates

- Core Goods: 0.22% M/M in Sept (analyst av 0.34%) after 0.28%

- Core goods ex used cars: 0.31% M/M after 0.17%

Housing inflation

- OER: 0.13 M/M vs analyst av 0.27 (range 0.21-0.31) after 0.38%

- Primary rents: 0.20 M/M vs analyst av 0.23% (range 0.14-0.26) after 0.30%

Core services ex-housing

- Core services excl OER & primary rents ('supercore'): 0.351% M/M after 0.33%. Latest 3mth av of 0.387%

- Limited analyst estimates for ex OER & rents had averaged 0.38% M/M, ranging from 0.30 to 0.42

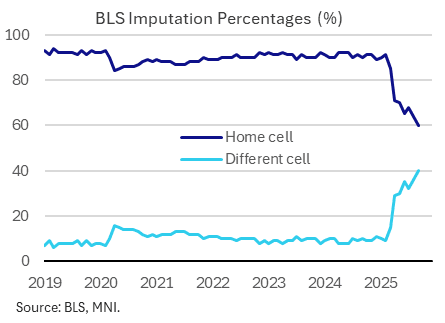

MNI US DATA: Further CPI Data Quality Concerns

- 40% of the commodities and services price survey source data for today’s CPI report was based on a “different cell” rather than its “home cell” in September, a new high after 36% in August.

- This September CPI report shouldn’t have been affected by the government shutdown, with its collection period coming earlier enough, and it instead extends what had already been a marked increase in different cell imputation this year reportedly owing in large part to budget and staff cuts.

- A historical average is closer to 10%, although it jumped to circa 30% from April where it then saw a range of 29-36% until August before the latest push higher to 40% in latest data.

- For context, it peaked at 15% in the pandemic when in-person surveys weren’t possible.

- As reported earlier, the White House's Rapid Response account on X.com suggests that the BLS may not release an October inflation report because it was unable to conduct the in-person surveys as normal during October, on account of the shutdown.

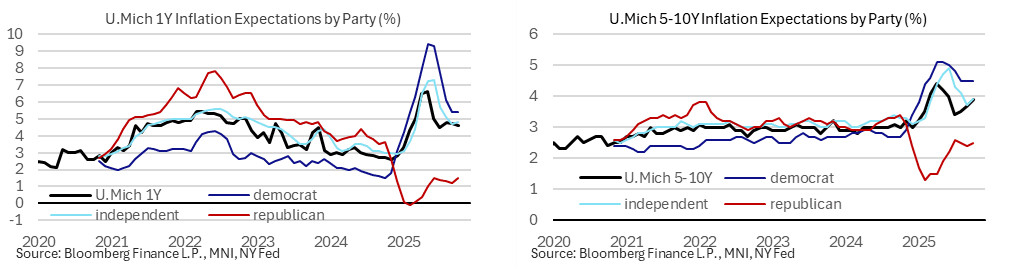

MNI US DATA: U.Mich 1Y Inflation Expectations Hold Dip But 5-10Y Highest Since June

- Consumer sentiment: 53.6 (cons 54.5, prelim 55.0) after 55.1 in September

- 1Y inflation expectations: 4.6% (cons & prelim 4.6) in Oct final after 4.7% in September – lowest since June

- 5-10Y inflation expectations: 3.9% (cons & prelim 3.7) in Oct final after 3.7% in September – highest since June

- From the press release: “Long-run inflation expectations increased from 3.7% last month to 3.9% this month but remains below this year’s high point seen in April. This month’s increase in long-run inflation expectations was driven primarily by independents and Republicans. Inflation uncertainty—as measured by the interquartile range of expectations—ticked up for both time horizons this month.”

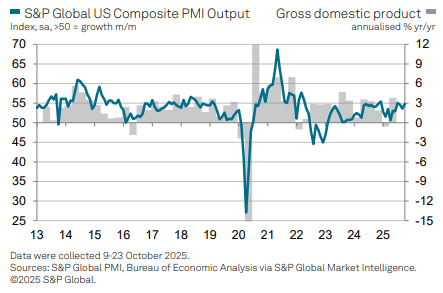

MNI US DATA: Flash PMIs Point To Solid Activity And Moderating Price Metrics

- Manufacturing PMI: 52.2 (Bloomberg cons 52.0) in Oct prelim after 52.0 in Sep – now a two-month high

- Services PMI: 55.2 (cons 53.5) after 54.2 – now a three-month high

- Composite PMI: 54.8 (cons 53.3) after 53.9 – now a three-month high

The PMI press release (link) notes strong business activity growth (second-fastest of the year) although prices charged rose at their softest rate since April:

MNI CANADA DATA: Trade Data, Key To Q3 GDP, Delayed On US Gov't Shutdown

The ongoing US government shutdown will impact Canadian Q3 GDP data and trade data for the foreseeable future. Specifically, StatCan notified Friday that it will not publish the September goods and services trade data on Nov 4 as scheduled, and will have to produce "special estimates" of Canadian exports to the US when it compiles Q3 GDP (due for Nov 28 release).

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 509.81 points (1.09%) at 47245.11

S&P E-Mini Future up 59.25 points (0.87%) at 6834.25

Nasdaq up 295.6 points (1.3%) at 23239.19

US 10-Yr yield is down 0.8 bps at 3.993%

US Dec 10-Yr futures are down 1/32 at 113-14.5

EURUSD up 0.0012 (0.1%) at 1.163

USDJPY up 0.28 (0.18%) at 152.85

#VALUE!

Gold is down $19.99 (-0.48%) at $4106.98

European bourses closing levels:

EuroStoxx 50 up 6.17 points (0.11%) at 5674.5

FTSE 100 up 67.05 points (0.7%) at 9645.62

German DAX up 32.1 points (0.13%) at 24239.89

French CAC 40 down 0.15 points (0%) at 8225.63

US TREASURY FUTURES CLOSE

3M10Y +1.921, 13.294 (L: 8.154 / H: 14.89)

2Y10Y +0.706, 51.309 (L: 46.875 / H: 52.749)

2Y30Y +1.773, 110.151 (L: 108.11 / H: 113.32)

5Y30Y +1.509, 98.308 (L: 93.181 / H: 99.875)

Current futures levels:

Dec 2-Yr futures down 0.125/32 at 104-12.375 (L: 104-10.875 / H: 104-15.25)

Dec 5-Yr futures up 0.25/32 at 109-23.75 (L: 109-20 / H: 109-30)

Dec 10-Yr futures down 1/32 at 113-14.5 (L: 113-09.5 / H: 113-24)

Dec 30-Yr futures down 6/32 at 118-21 (L: 118-11 / H: 119-07)

Dec Ultra futures down 7/32 at 123-1 (L: 122-20 / H: 123-24)

MNI US 10YR FUTURE TECHS: (Z5) MA Studies Highlight A Bullish Structure

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 114-02 High Oct 17

- PRICE: 113-14 @ 1201 ET Oct 24

- SUP 1: 113-06+ 20-day EMA

- SUP 2: 112-30 Low Oct 13

- SUP 3: 112-24+ 50-day EMA

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

A bullish structure in Treasuries remains intact and short-term weakness is considered corrective. The contract recently breached a key resistance at 113-29, the Sep 11 high, to confirm a resumption of the medium-term uptrend. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 113-06+, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.025 at 96.385

Mar 26 +0.010 at 96.615

Jun 26 steady00 at 96.825

Sep 26 -0.005 at 96.970

Red Pack (Dec 26-Sep 27) -0.01 to -0.005

Green Pack (Dec 27-Sep 28) -0.015 to -0.01

Blue Pack (Dec 28-Sep 29) -0.015 to -0.01

Gold Pack (Dec 29-Sep 30) -0.01 to -0.005

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.24% (+0.03), volume: $3.002T

- Broad General Collateral Rate (BGCR): 4.21% (+0.03), volume: $1.145T

- Tri-Party General Collateral Rate (TCR): 4.21% (+0.03), volume: $1.113T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $93B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $173B

FED Reverse Repo Operation

RRP usage retreats to $2.435B (lowest level since mid-March 2021) with 4 counterparties this afternoon from $6.941B Thursday. Compares to this year's high usage of $460.731B on June 30.

PIPELINE Corporate bond roundup:

- Date $MM Issuer (Priced *, Launch #)

- $1.5B Priced Thursday, $26.4B/wk

- 10/23 $1B *Versant Media Group 5.25NC2 7.239%

- 10/23 $500M *Pershing Square 7Y +175

MNI FOREX: USD Weakness Short-Lived Following Soft US CPI

- Following the US CPI data, US yields were pressured lower, naturally weighing on the US dollar. Headline CPI came in on the lower side of expectations in September (headline 0.31% M/M vs 0.40% median expected, 0.38% prior), built largely on the miss in core categories.

- The dollar index declined around 30 pips in the immediate aftermath, however, downside momentum quickly stalled. Overall, the DXY is unchanged on the session as we approach the weekend close.

- The positive impulse for major US equity benchmarks has continued to underpin the outperformance for Cross/JPY on Friday, with USDJPY looking to extend its winning streak to six sessions, currently hovering just below 153.00. Japanese politics have been the key driver all week, as the market continues to assess PM Takaichi’s new cabinet and an imminent stimulus package said to be in the works.

- Despite Eurozone flash PMIs and the US data, EURUSD has remained in a 47pip range Friday. For Germany, in addition to the stronger growth signals, an uptick in output charge inflationary pressures added to the hawkish theme of the flash PMI report.

- US dollar declines were most notable for gold, where XAU/USD sharply recovered around 2% from pre-data levels to trade at levels close to $4,120, still roughly $260 off the recent record highs.

- Over the weekend, it is worth noting that daylight saving time shifts will occur across Europe. On Sunday, there are midterm elections in Argentina. Monday’s data calendar is highlighted by German IFO, while RBA Governor Bullock will speak.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 27/10/2025 | 0900/1000 | ** | M3 | |

| 27/10/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 27/10/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 27/10/2025 | 0915/1015 | ECB Elderson Keynote on Banking Governance | ||

| 27/10/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 27/10/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/10/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/10/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 27/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/10/2025 | 1530/1130 | * | US Treasury Auction Result for 2 Year Note | |

| 27/10/2025 | 1700/1300 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/10/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/10/2025 | 0001/0001 | * | BRC Monthly Shop Price Index |