FED: MNI Fed Preview - October 2025: QT, Or Not QT

Oct-24 21:06

MNI's preview of the October FOMC has been published - Download Full Report Here

- The Federal Reserve is overwhelmingly expected to cut the funds rate by 25bp for a 2nd consecutive meeting on October 29, bringing the target range to 3.75-4.00%.

- This will again be framed as a risk management cut, with the limited data available since the September meeting not disconfirming that the shift in the balance of risks had tilted toward labor market downside.

- Dissent to this decision should once again be limited to Gov Miran in favor of a 50bp cut.

- With limited new developments and official data to opine on, Chair Powell’s press conference will be eyed for affirmation that a December cut remains on track, as signalled by the most recent Dot Plot.

- He’s unlikely to give much away, but it would be surprise given the lack of data and relevant developments if he suggested that a further 2025 cut was in any greater doubt than it was 6 weeks earlier.

- Instead, we think focus in terms of action at this meeting will be on the balance sheet, with the Fed likely to announce an end to quantitative tightening amid diminishing reserve levels and nascent evidence of funding market pressures.

- We will also be watching for any news on the Fed’s communications framework, with an updated “Dot Plot” potentially unveiled at some point by year-end.

MNI’s separate preview of sell-side analyst summaries to follow on Monday Oct 27

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Coming Up In Asia Pac Markets On Thursday

Sep-24 21:06

| 0050BST | 0750HKT | 0950AEST | Japan Aug PPI Services |

| 0050BST | 0750HKT | 0950AEST | BoJ Minutes Of July Meeting |

| 0100BST | 0800HKT | 1000AEST | Australia 2035 Inflation-Linked Bond Sale |

| 0230BST | 0930HKT | 1130AEST | Australia Aug Job Vacancies |

| 0335BST | 1035HKT | 1235AEST | New Zealand 2030, 2033 Bond Sales |

| 0435BST | 1135HKT | 1335AEST | Japan 40yr Bond Sale |

| 0630BST | 1330HKT | 1530AEST | Japan Aug Nationwide Dept Store Sales |

Source: Bloomberg Finance L.P./MNI

FED: SF's Daly: Do Not Want To See Further Labor Market Softening

Sep-24 20:51

SF Fed President Daly's comments in Q&A suggest that she's not overly concerned about the labor market, but sees enough signs of potential weakness - and not enough signs of tariff-related inflation persistence - that she agrees with the general principle of cutting rates as "insurance".

- Asked whether she would consider the labor market "weak", Daly says: "I wouldn't really characterize the labor market as weak. The unemployment rate is low,... The people are finding jobs. Wage growth is still expanding at productivity plus inflation. So you have a sense that people are moving and doing things. But what is true is that it's not as speedy as it once was. So if you think three years ago, it was what we called frothy, then it got to healthy, then it got to solid. Now I'd say it's sustainable, but I do not want to see further softening. So one of the things that you see in the [September] rate cut is some insurance - you see the labor market has softened at a pretty good clip. it's come down rapidly from its highs, but the level of where it's sitting right now isn't weak. But you want to prevent that weakness, because we know, historically, once it tips into weakness, it's extremely hard to get it back out."

- Daly: "I don't see stagflation as around the corner. What I do see is that inflation has been printing above our target for quite a while, and that people have been enduring that sense that prices are rising. They're rising at a faster clip. When I get up in the morning, I still have to think about price increases, and we have work to do there on the labor side... I'd see that's an economy that still needs monetary policy, you know, bridling, but not as much as we had. But it's not something that I see as faltering and recession risk... recession risk is very low right now... Stagflation is a very different thing."

- Daly doesn't sound concerned about persistent tariff impacts on inflation: "We haven't seen tariffs [impact] in any sector other than the directly tariffed sectors like goods, and only the tariff parts of that. And then in services, you haven't seen it gone up. And in housing, where they have many, many inputs that are tariffed, you haven't seen the cost of housing rise rapidly. In fact, shelter inflation has been coming down, not going up. So that's, I think, evidence so far that's consistent with tariffs being a one time thing... we're seeing that if you look at the announced tariffs ... they have not come into consumer prices because ... firms take them along the supply chain, and everybody shares a little bit of that, or spreads it out over a longer period."

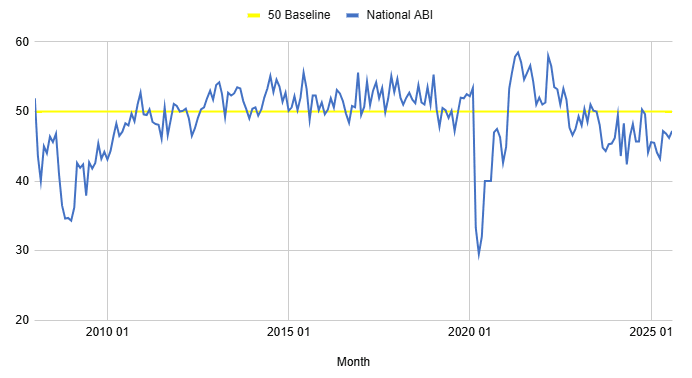

US DATA: Architectural Billings Suggest Weakness Ahead For Construction

Sep-24 20:30

The American Institute of Architects (AIA)'s Architecture Billings Index (ABI) remained below the 50 mark in August.

- At 47.2, it improved from 46.2 in July. But the sub-50 reading meant that the value of new design contracts dropped for a record 18th consecutive month (the series has been published for 15 years).

- As a leading indicator of construction activity, this is a negative sign for both nonresidential and residential (multifamily) investment over the coming year.

- Already, construction is under duress - as of the latest data for August from the Census Bureau, private sector construction activity contracted (in value terms) for the 14th consecutive month (-0.2% after -0.5%). Overall, since peaking in December 2023, private nonresidential construction has fallen by 6.9%.