FOREX: USD Weakness Short-Lived Following Soft US CPI

Oct-24 17:52

- Following the US CPI data, US yields were pressured lower, naturally weighing on the US dollar. Headline CPI came in on the lower side of expectations in September (headline 0.31% M/M vs 0.40% median expected, 0.38% prior), built largely on the miss in core categories.

- The dollar index declined around 30 pips in the immediate aftermath, however, downside momentum quickly stalled. Overall, the DXY is unchanged on the session as we approach the weekend close.

- The positive impulse for major US equity benchmarks has continued to underpin the outperformance for Cross/JPY on Friday, with USDJPY looking to extend its winning streak to six sessions, currently hovering just below 153.00. Japanese politics have been the key driver all week, as the market continues to assess PM Takaichi’s new cabinet and an imminent stimulus package said to be in the works.

- Despite Eurozone flash PMIs and the US data, EURUSD has remained in a 47pip range Friday. For Germany, in addition to the stronger growth signals, an uptick in output charge inflationary pressures added to the hawkish theme of the flash PMI report.

- US dollar declines were most notable for gold, where XAU/USD sharply recovered around 2% from pre-data levels to trade at levels close to $4,120, still roughly $260 off the recent record highs.

- Over the weekend, it is worth noting that daylight saving time shifts will occur across Europe. On Sunday, there are midterm elections in Argentina. Monday’s data calendar is highlighted by German IFO, while RBA Governor Bullock will speak.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Nov'25 10Y Skew Play

Sep-24 17:45

- +15,000 TYX5 111/112 put spds 1 over 114 calls ref 112-22.5

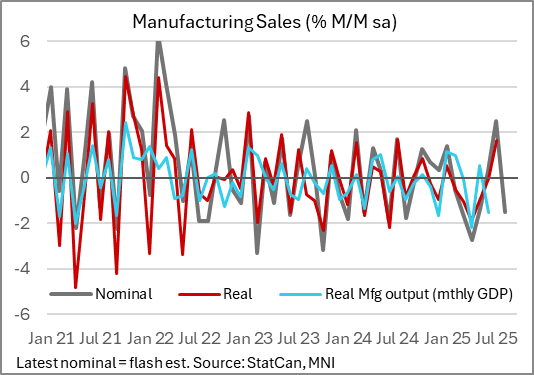

CANADA DATA: Pullback In Aug Manufacturing Sales In Line With Monthly Volatility

Sep-24 17:36

StatCan's advance estimate of manufacturing sales for August is for a 1.5% M/M decrease, which if confirmed would mark the first decrease in 3 months and partially reversing the 2.5% rise in July (all in value and not volume terms).

- As usual with the advance estimate there were no further details available, though StatCan reports the largest decreases were in the transportation equipment and food subsectors.

- Even with the M/M decrease, the comparison with the sharp drawdown in March /April/May means that manufacturing sales were due to post a 6-month best -1.5% on a 3M/3M annualized basis.

- As with other indicators, though, this one suggests the nascent pickup in activity and sentiment in various sectors in the summer - after the worst of the US-Canada trade conflict concerns - has subsequently petered out, with activity remaining volatile.

- We get July GDP data on Friday, with expectations and the advance estimate showing +0.1% M/M after -0.1% in June. Per StatCan's advance GDP release, there were no notable mentions of July manufacturing output :"Increases in real estate and rental and leasing, mining and quarrying (except oil and gas) and wholesale trade were partially offset by a decrease in retail trade" in the month.

- July manufacturing sales were confirmed at 2.5% last week, with wholesale sales ex-petroleum growth reported at 1.2% - so three of the four major "sales" categories point to a pickup in July activity (retail sales fell 0.8% however), in line with the StatCan advance anecdote).

- For August, retail sales are estimated to have bounced (1.0% M/M).

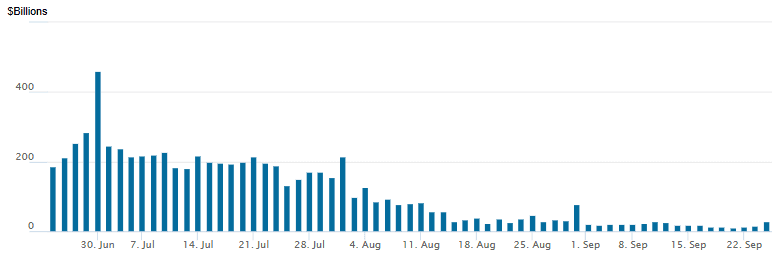

US: FED Reverse Repo Operation

Sep-24 17:30

RRP usage bounces to $29.172B with 22 counterparties this afternoon from $14.402B Tuesday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.