MNI ASIA MARKETS ANALYSIS: Tsy Yields Decline Ahead Emply Data

HIGHLIGHTS

- Treasuries rally on soft JOLTS jobs data in the lead up to Thursday's ADP, Friday's NFP employment release - key data with the Fed entering policy blackout late Friday through September 18.

- Initial greenback strength reversed and subsequently extended lower following a softer-than-expected US JOLTS jobs report, stoking the softening labour market narrative as we approach Friday’s release of non-farm payrolls.

- The Fed's latest Beige Book pointed to a slightly improved assessment of current economic activity in August versus the prior edition in July, with selling price pressures remaining modestly/moderately to the upside.

US TSYS

MNI US TSYS: Trimming Gains Ahead More Employ Data

- Treasuries look to finish near late session highs, trimming gains ahead of upcoming data: Thursday's ADP, Jobless Claims, ISM Services, followed by the August Employment report on Friday.

- Treasuries gapped higher after this morning's lower than expected JOLTS jobs data: Job openings were lower than expected at 7181k (sa, cons 7380k) in July after downward revised 7357k (initial 7437k) in June. Combined with the already known sizeable rise in unemployment from last month’s payrolls report and the ratio of openings to unemployed fell to 0.99 from 1.05 (initial 1.06).

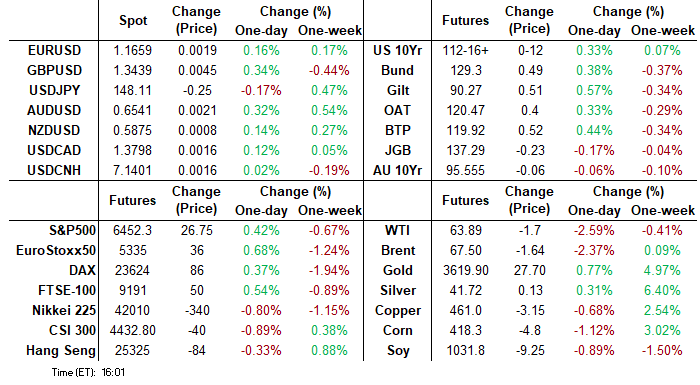

- Currently, the Dec'25 10Y trades +12.5 at 112-17 (yld 4.2168 -.0446) vs. 112-21 high - briefly through initial technical resistance: 112-20+ Aug 28 / 29 A breach of this hurdle confirms a resumption of the current bull cycle and signals scope for an extension towards the 113-00 handle.

- Curves bull flatten: 2s10s -1.804 at 60.209 5s30s -2.961 at 120.651.

- The USD index is roughly 0.3% lower on the session as we approach the APAC crossover, with GBP and AUD marginally outperforming while the likes of CAD and CHF remain closer to unchanged on the day.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (+0.05), volume: $2.947T

- Broad General Collateral Rate (BGCR): 4.36% (+0.03), volume: $1.142T

- Tri-Party General Collateral Rate (TCR): 4.36% (+0.03), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $120B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $220B

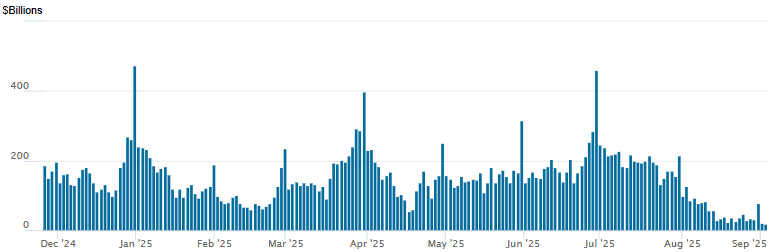

FED Reverse Repo Operation

RRP usage continues to retreat to lowest levels since early April 2021 today: $17.923B with 17 counterparties this afternoon, from $21.066B yesterday. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options remain mixed late Wednesday, both leaning towards puts in the second half. Underlying futures scaling off late session highs. Projected rate cuts have gained vs. morning (*) levels: Sep'25 at -23.8bp (-23bp), Oct'25 at -37.7bp (-35.9bp), Dec'25 at -58.5bp (-55.4bp), Jan'26 at -70.2bp (-66.9bp).

SOFR Options:

+12,500 SFRV5 96.00/96.12/96.25/96.37 call condors, 4.75

+5,000 SFRZ5 96.25/96.50 1x2 call spds, 1.75 vs. 96.24/0.05%

over 5,000 0QH6 96.50/96.75 put spds vs. 3QH6 96.25/96.50 put spds, 0.75 net steepener

+4,000 SFRZ5 96.06/96.12/96.18/96.25 put condors, 1.75 ref 96.21

2,000 SFRV5 96.06/96.18/96.25/96.37 call condors ref 96.21

-3,500 SFRU5 95.81/95.87/95.93 put flys, 1.75 ref 95.905

2,000 SFRU5 95.87/95.93 2x1 put spds

+22,000 SFRX5 95.93/96.06/96.18 put flys, 2.5-2.75 ref 96.215

+10,000 SFRU5 96.00/96.12/96.25 call flys, 0.75

+22,500 SFRU6 97.25/97.50 call spds vs. 96.00 put, 1.0 ref 96.885

Treasury Options:

+23,647 wk2 TY 112 puts, 13 vs. 112-20.5 (exp 9/12)

2,500 TYV5 110.25/110.5/111.25 broken put flys, 2 ref 112-17

Block/screen, 20,000 USV5 108/USX5 106 put spds, 7 net/steepener vs. 113-10

+5,000 UXYZ5 109.5/112.5 put spds, 39

+4,000 FVV5 110 calls, 22

over +22,200 TUV5 104.62 calls, 4.5-5.0

over +16,800 TUV5 104.5 calls, 6.5

over 19,800 TUV5 104.75 calls, 3.5 ref 104-06.62

9,000 Wed wkly TY 112 puts ref 112-02

6,000 wk1 TY 112.5 calls, 11 ref 112-04

4,000 wk1 TY 112/112.5 1x2 call spds, 3

MNI BONDS: EGBs-GILTS CASH CLOSE: Pressure On Long End Abates

Yields reversed an early rise to finish lower Wednesday, with strong bull flattening evident across EGBs and Gilts.

- Gilt futures pierced Tuesday's lows in early trade, with ongoing fiscal concerns continuing to weigh on the space, but eventualy bounced; meanwhile 10Y Bund yields weakened but held the 2.80% level.

- Having found an early footing, bonds rallied through much of the remainder of the session.

- Weak US job openings data added a final up-leg to global core FI in mid-afternoon, with yields closing near their session lows. Long-end Gilts also benefited from DMO cancelling a 30Y auction in the FQ3 quarter.

- In BOE Treasury Select Committee testimony, some highlights included Lombardelli sounding more hawkish that MNI's Markets Team had assumed, while BoE's Bailey noted that the bank's decision on QT in the next few weeks "is an open decision".

- European data wasn't a market-mover, with composite PMIs in the Eurozone and UK respectively revised slightly lower/higher in the final readings.

- The German and UK curves bull flattened, with Gilts outperforming; periphery/semi-core EGB spreads tightened, with BTPs outperforming.

- Thursday's schedule includes Eurozone retail sales and an appearance by ECB's Cipollone, while Swiss and Swedish inflation will garner some attention.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.8bps at 1.966%, 5-Yr is down 3.3bps at 2.28%, 10-Yr is down 4.6bps at 2.74%, and 30-Yr is down 5bps at 3.356%.

- UK: The 2-Yr yield is down 2.2bps at 3.96%, 5-Yr is down 4.1bps at 4.13%, 10-Yr is down 5.2bps at 4.748%, and 30-Yr is down 9bps at 5.603%.

- Italian BTP spread down 1.7bps at 87.3bps / French OAT down 0.2bps at 79.9bps

MNI OPTIONS: All Call Spread Buying In Rates

Wednesday's Europe rates/bond options flow included:

- ERU5 97.9375/98.00cs, bought for 2 in 20k

- SFIZ5 96.20/96.25cs, bought for 1.75 in 2k

- SFIM6 96.70/96.85cs, bought for 2.75 in 6k

MNI FOREX: USD Reverts Lower Following Soft JOLTS Jobs Report

- It was a tale of two halves for G10 currency markets on Wednesday, as initial greenback strength reversed and subsequently extended lower following a softer-than-expected US JOLTS jobs report, stoking the softening labour market narrative as we approach Friday’s release of non-farm payrolls.

- The USD index is roughly 0.3% lower on the session as we approach the APAC crossover, with GBP and AUD marginally outperforming while the likes of CAD and CHF remain closer to unchanged on the day.

- Initial sterling weakness saw GBPUSD print a near one month low of 1.3333, however, greater stability for risk and the associated reversal lower for UK Gilt yields helped underpin a solid GBP recovery. Cable rose around 120 pips to 1.3450 amid these dynamics erasing a solid portion of the steep declines from Tuesday’s session.

- For AUD, there was a more resilient tone across the entire session following Australian Q2 GDP coming in stronger than both the RBA and consensus expected. Additional hawkish comments from RBA’s Bullock helped underpin the Aussie rally, which has seen AUDUSD close within close proximity of 0.6569 resistance. Clearance of this level would expose key resistance and the bull trigger at 0.6625, the Jul 24 high.

- Additionally, AUDNZD strength continues to stand out, reaching fresh cycle highs today above 1.1140. A breach of the key 1.1180 mark would place the cross at the highest level since late 2022. Above here, 1.1250 marks a significant 76.4% retracement point of the 2022 selloff.

- USDJPY nicely respected Fibonacci resistance at 149.12, printing a high of 149.14 during early European trade. Following that, waning dollar momentum and the subsequent price action following the US data helped USDJPY eventually back below the 148 handle. Heightened political uncertainty in Japan allows USDJPY to hold onto its 100 pip advance this week.

- Swiss CPI kick starts tomorrow’s calendar before US ADP, jobless claims and ISM Services PMI are released.

MNI FX OPTIONS: Larger FX Option Pipeline

- EUR/USD: Sep05 $1.1550(E1.4bln), $1.1600(E2.1bln), $1.1740-50(E1.5bln), $1.1775-80(E1.1bln), $1.1800(E1.3bln); Sep08 $1.1600(E1.2bln)

- USD/JPY: Sep05 Y146.00($2.2bln), Y146.95-00($1.2bln), Y147.35-50($1.1bln)

- GBP/USD: Sep09 $1.3595-20(Gbp981mln)

- AUD/USD: Sep05 $0.6400(A$1.1bln), $0.6500-10(A$1.3bln), $0.6600(A$1.0bln)

- USD/CAD: Sep05 C$1.3850-60($1.0bln)

MNI US STOCKS: Late Equities Roundup: Energy & Industrials Shares Weighing

- Stocks remain mixed late Wednesday, a weaker DJIA dragging the tech-heavy Nasdaq index off earlier highs. Currently, the DJIA trades down 219.89 points (-0.49%) at 45077.47, S&P E-Minis up 6.75 points (0.11%) at 6432.75, Nasdaq up 119.3 points (0.6%) at 21399.8.

- Energy and Industrial sector shares continue to lead decliners in late trade, oil and gas shares reversing the prior session gains as crude prices reverse support (WTI -1.60 at 63.99): Diamondback Energy -4.96%, APA Corp -4.66%, EOG Resources -4.17%, ConocoPhillips -3.93% and Halliburton -3.61%.

- Capital goods shares weighed on the Industrials sector: Axon Enterprise -3.61%, PACCAR -2.39%, Boeing -2.35% and Carrier Global -2.20%.

- On the positive side, media and entertainment services shares buoyed the Communication Services sector: Alphabet +8.31%, Paramount Skydance +4.63%, Warner Bros Discovery +2.02% and Match Group +1.33%.

- Consumer Discretionary sector shares followed a close second: Norwegian Cruise Line +2.29%, Tesla +2.22%, PulteGroup +1.75%, CarMax and DoorDash both +1.69%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Monitoring Support At The 50-Day EMA

- RES 4: 6600.00 Round number resistance

- RES 3: 6585.83 2.0% 10-dma envelope

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6523.00 High Aug 28 and the bull trigger

- PRICE: 6432.75 @ 1425 ET Sep 3

- SUP 1: 6371.75 Low Sep 2

- SUP 2: 6332.30 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback is - for now - considered corrective. Price has traded through the 20-day EMA. The key support to watch lies at the 50-day EMA, at 6336.02. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

MNI COMMODITIES: Gold Hits Another All-Time High, Silver Rallies, Crude Pulls Back

- Spot gold has rallied by a further 1.2% to a fresh all-time high at $3,578/oz today, with the yellow metal now up by ~8% from the August 20 low.

- Spot is on track for its longest streak of daily higher highs since 2022, which was only previously surpassed in 2017.

- The recent rally has been spurred by fresh concerns around Fed independence amid the ongoing Governor Cook saga and mounting fears around fiscal pressures.

- Gold remains in a clear bull cycle, with this week’s gains confirming a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows.

- The next objective is the $3,600.00 handle, followed by $3,623.1, a Fibonacci projection.

- Meanwhile, silver has also rallied by 1.2% to $41.4/oz today, taking total gains since Aug 20 to around 12%.

- Trend signals in silver remain bullish, with the precious metal piercing resistance at $41.064, the 1.764 projection of the Apr 7 - 25 - May 15 swing, today. Above here, sights are on round number resistance at the $42.0 handle next.

- Elsewhere, crude has come under pressure on Wednesday after OPEC+ said it was considering further voluntary cut rollbacks at its upcoming weekend meeting.

- WTI Oct 25 is down by 2.6% at $63.9/bbl.

- A bear cycle in WTI futures remains intact, with initial support seen at $61.29, the Aug 13 low and the bear trigger. Clearance of this level would pave the way for a move towards $57.71, the May 30 low.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0630/0830 | *** | CPI | |

| 04/09/2025 | 0700/0900 | ** | Unemployment | |

| 04/09/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/09/2025 | 0830/0930 | Decision Maker Panel data | ||

| 04/09/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/09/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 04/09/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 04/09/2025 | 0930/1130 | ECB Cipollone Speaks at Digital Euro Hearing, European Parliament | ||

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/09/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/09/2025 | 1400/1000 | Fed nominee Stephen Miran | ||

| 04/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 04/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/09/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 04/09/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 04/09/2025 | 1605/1205 | New York Fed's John Williams | ||

| 04/09/2025 | 2300/1900 | Chicago Fed's Austan Goolsbee | ||

| 05/09/2025 | 2330/0830 | ** | average wages (p) | |

| 05/09/2025 | 2330/0830 | ** | Household spending |